Axe-Throwing Business Insurance

Getting insurance for your axe-throwing business is essential.

Axe-throwing businesses need to be protected against things like claims of personal injury, property damage, or breach of contract.

For example, a client may accidentally injure an employee while throwing an axe, or a poorly-thrown axe could cause damage to the surrounding premises.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for an Axe-Throwing Business

General liability insurance is — generally speaking — one of the most important insurance policies for axe-throwing businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Nonetheless, it can be beneficial for axe-throwing businesses to employ several supplementary policies for more extensive protection. Some useful policies include:

- Commercial property insurance

- Professional liability insurance

- Commercial auto insurance

- Workers’ compensation insurance

There are generally two categories of insurance providers available for you to choose between when looking for business coverage:

- Traditional brick-and-mortar insurers: Includes established providers (such as The Hartford and Hiscox) that utilize insurance agents and a physical store to provide insurance. However, this necessitates higher overheads, which are often passed on to their customers.

- Online insurers: Contrastingly, these insurers offer quotes completely online without an insurance agent’s assistance. By taking advantage of AI technology, these providers can offer highly customized quotes at affordable rates due to their lower overheads.

Let's Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

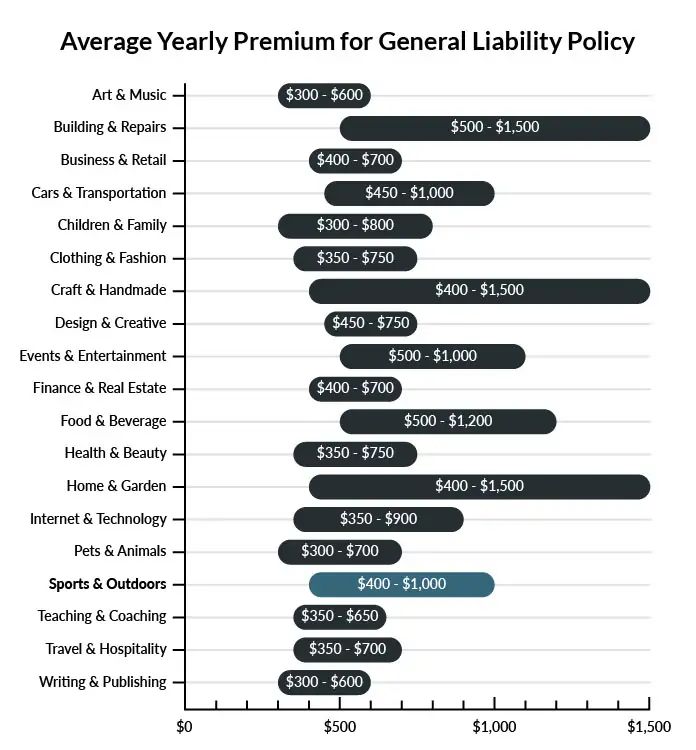

The average axe-throwing business in America spends between $400-$1,100 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for an axe-throwing business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for an Axe-Throwing Business

Example 1: A client has been drinking and hurls one of your provided axes at his friend during a bachelor party. If found liable for resulting damages, your business would be covered by general liability insurance for court-ordered payments or settlements reached.

Example 2: A client is trying to collect all of the axes toward the end of a session to be helpful. He loses his balance and falls, hurting himself and losing a fair amount of blood before an ambulance arrives. If liable, your business would likely be covered by general liability policy for resulting damage payments owed.

Example 3: A client tries to follow instructions but fails and throws an axe improperly, resulting in a serious shoulder injury that must be surgically repaired. If found liable, your business would probably have coverage through a general liability policy. This would help to cover damages owed or any settlement reached with the plaintiff.

Other Types of Coverage Axe-Throwing Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Your axe-throwing business will need plenty of material assets, including axes, range equipment, targets, safety gear, vehicles, and real estate on which to set up a place of business. If your property is compromised by incidents like fire or violent weather, you will be looking at a sizeable financial setback. Commercial property insurance is designed for businesses that need protection for their material resources, including tools, equipment, machinery, and owned real estate.

Professional Liability Insurance

This is a policy for businesses that offer careful advice in a professional capacity to clients. If your guides at the axe-throwing facility are found to have been negligent or unprofessional in a way that leads to injury or other damages, you could suffer a lawsuit from dissatisfied clientele. Professional liability insurance provides coverage for businesses that might be held responsible for perceived errors or various negative outcomes related to the services provided and/or promised.

Commercial Auto Insurance

If you would like to take your axe-throwing business to the next level, you can become a mobile service that relocates per the needs of its clientele. If your business is making that leap, or including commercial vehicles for any reason, this policy is a must-have. Commercial auto insurance keeps you and your employed drivers covered for accidents on public roads.

Traffic collisions can happen anytime and anywhere, and it’s legally required for vehicles to be insured in either a personal or professional capacity.

Workers' Compensation Insurance

Unless you are a one-man axe-throwing company, you’ll need a policy to help cover your employees. Part-time and full-time employees require your business to take out a workers’ compensation policy. Keep your employees and their families covered in the event of workplace accidents.

This policy will include disability and similar benefits for employees injured while in the process of fulfilling their professional duties.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your axe-throwing business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Axe-Throwing Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Next Insurance. Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

"Business insurance" is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes, it is highly recommended. Due to the high-risk nature of an axe-throwing business, they will be exposed to a variety of different claims from the get-go. This means that acquiring appropriate business insurance before starting is vital.

In fact, some forms of insurance may even be an operational requirement for your business to be in compliance with the law (e.g., workers’ compensation and commercial auto).

Not necessarily. Certain exceptions may be written directly into your axe-throwing business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.