Board Game Cafe Business Insurance

Getting insurance for your board game cafe is essential.

To ensure they are protected against potential losses or legal liabilities, board game cafes must shelter themselves from operational risks. These risks may encompass various scenarios, such as property damage, financial losses, or claims of negligence from third parties.

For example, in an attempt to placate a disorderly customer, your employee may have to block her physically from injuring another customer. The customer files suit. It’s important to have insurance in a situation like that to protect your business against any allegations of trespass to a person.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Board Game Cafe Business

General liability insurance is — generally speaking — one of the most important insurance policies for board game cafes.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

While general liability insurance provides coverage for a variety of risks, it may not be quite adequate for all the risks that your business may face. Some risks may require coverage from specialized policies, such as those that offer:

- Commercial property coverage: Policies of this sort will offer protection if a faulty faucet leaks water into the store room. Coverage is usually much wider than for flooding, however. And will extend to property that is damaged by vandals or stock that is stolen by burglars, as well as property damage due to fire.

- Commercial auto insurance: Some auto insurance policies may offer just basic protection that indemnifies drivers for collision-related damage to vehicles or injury to individuals. However, a comprehensive policy protects against off-the-road risks.

- Business income coverage: This is coverage that reimburses you for loss of income that results from an interruption of business. If, for example, your business has to shut up shop for a while because some adverse event, such as a fire, has occurred, the insurer will cover the loss of income sustained.

In the 21st century, you’ll find there are two basic kinds of providers operating in the industry:

- Traditional brick and mortar insurers: This category includes firms, like Travelers and Chubb, that rely on actuaries and historic data to assess risks.

- Online insurers: These providers, like MetroMile and Next, operate through the internet and process huge quantities of data to price risk. This allows online insurers to provide better coverage at much lower premiums.

Let's Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

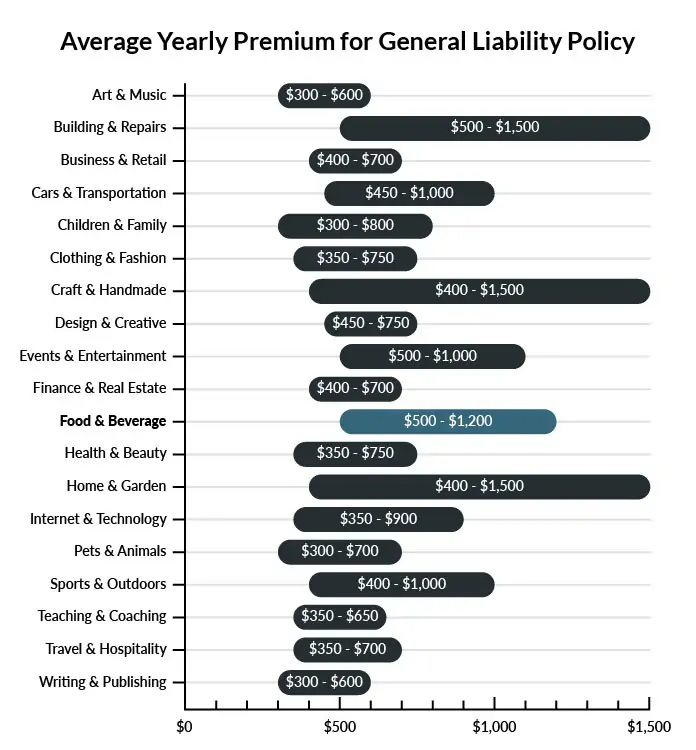

The average board game cafe in America spends between $500-$1,200 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a board game cafe business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for a Board Game Cafe Business

Example 1: A waiter spills scalding hot coffee on one of the patrons who is playing a game at his table. The spill causes serious burns, and the patron is rushed to the hospital. If liable for damages, general liability insurance would probably help your company pay whatever a court found it to owe or any settlement reached between you and the injured patron.

Example 2: A customer is playing a game and eating the salad he ordered, but he has a serious allergic reaction to one of the ingredients. After receiving medical care, he decides to sue your cafe. If liable for the incident, general liability insurance would probably help to pay for the damages incurred or any settlement agreed upon by you and the injured party.

Example 3: A custodian fails to leave a wet floor sign, and a customer slips, landing on his tailbone. Part of the bone has fractured, and he sues your cafe. If held liable by the court, you could probably rely on general liability insurance to help cover some of the damages owed.

Other Types of Coverage Board Game Cafe Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

This is a big one for board game cafes. Not only do they run a little restaurant/bar, but they also operate a board game store on the same premises! Disasters like fire or violent weather can lead to a loss of equipment, supplies, kitchen machinery, and pricey inventory. The board games alone tend to run an average of $40-$50, and some games go for as much as $100. That’s a lot of crucial inventory loss. A serious board game cafe needs a commercial property insurance policy to keep its material assets covered in the event of the aforementioned disasters or similar catastrophes. This policy will cover commercial material goods as well as owned commercial real estate impacted by the incident.

Crime Insurance

Due to a resurgence over the past decade, the board game industry is alive and stronger than ever. Part of its resurgence into pop culture and its economic viability has to do with the new nature of board game content, which is often extensive, complex, and designed to meet customers’ expectations for innovative gaming experiences.

This means that board game cafes are keeping some very expensive inventory, much of it neatly packaged for quick removal. Should employee dishonesty cost your business thousands in lost inventory or cash, crime insurance provides your business coverage. It can also cover computer fraud losses and the theft of client property.

Liquor Liability Insurance

Many board game cafes provide alcohol as part of their versatile business models. Board games are social events, and where there is recreational socializing, there is often alcohol. Gaming and drinking can play well together, but if your business opts to provide alcohol to its patrons, a liquor license is not only important, it’s required by law.

Events that are normally covered by general liability insurance may be covered by this policy instead—as long as alcohol is reasonably determined to be a significant causal factor in the damage. Intoxicated patrons may be acting of their own accord, but your business could be found liable for their destructive behavior anyhow. Keep your board game cafe covered for intoxication incidents out of its control with liquor liability insurance.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your board game cafe business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Board Game Cafe Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Next Insurance. Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

"Business insurance" is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes, and there are good reasons why you need business insurance. Your fledgling business will be exposed to risk even before its doors are open to the public. Adjustments to the premises, hiring and managing workers, creating operational procedures: these are all activities that involve risk despite their innocuous guise.

In addition, state laws mandate the purchase of commercial auto insurance to cover company vehicles, and workers’ compensation insurance to cover employees.

Not necessarily. Certain exceptions may be written directly into your board game cafe business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.