Escape Room Business Insurance

Getting insurance for your escape room is essential.

Escape rooms need financial protection from personal injury claims, property claims, and other types of risks.

For example, a customer could injure themselves while in a room, or panic while trying to get out of a room and sue for emotional distress.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for an Escape Room Business

General liability insurance is — generally speaking — one of the most important insurance policies for escape rooms.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

In addition to general liability policies, other types of policies should be considered for your escape room:

- Workers’ compensation insurance

- Product liability insurance

- Commercial property insurance

- Commercial umbrella insurance

You can purchase business insurance for your escape room from a traditional provider or an online provider. You’ve probably heard of a lot of traditional providers, such as Nationwide and The Hartford. These are large, well-established companies that have considerable experience. However, they also charge more because they use agents to sell insurance and maintain physical offices.

Online providers, by contrast, are more agile and cheaper because they sell insurance on their websites. They don’t use agents, either, which means they can charge less for the same high-quality coverage.

Let's Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

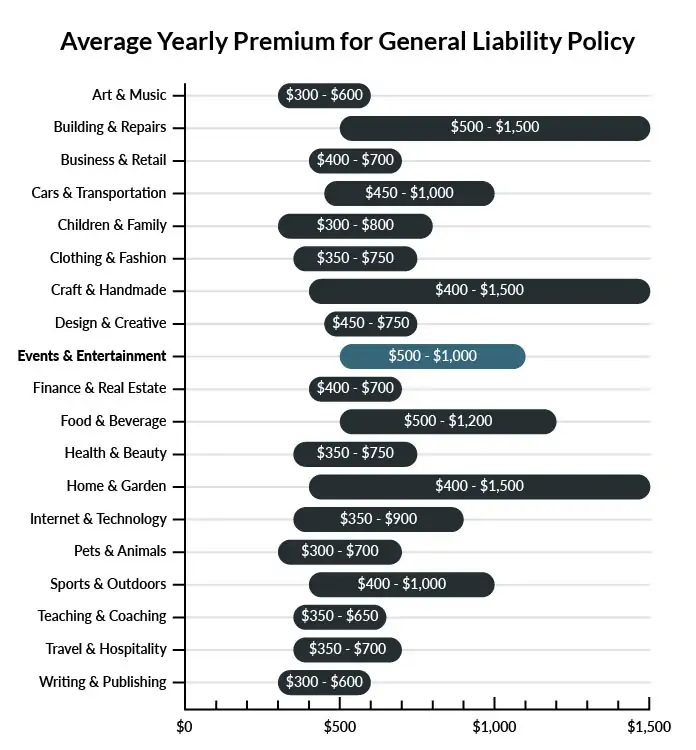

The average escape room business in America spends between $500 - $1,100 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for an escape room business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for an Escape Room Business

Example 1: In your escape room, a customer is exposed to a container full of non-venomous snakes. The customer becomes erratic and eventually decides to sue your business. His attorney writes that you are at fault for failing to provide foreknowledge that snakes, “reasonably predictable sources of psychologically valid phobias,” were present in the escape room. General liability insurance could probably cover your business’s losses in the event of a court order or settlement for the plaintiff’s resulting psychiatric sessions.

Example 2: A new employee forgets to administer bodily harm waivers to a pair of customers. The theme of their escape room is pitch-black darkness, and one of the customers walks into a wall, breaking his nose. The customer’s nasal surgery will be expensive, and while a waiver cannot always protect your business, you are far more vulnerable without one. The customer decides to sue your business. General liability insurance would likely provide coverage for damages owed or settlements reached regarding the accident.

Example 3: Your business is being sued for failing to release a customer from her escape room in a timely manner. She claims that she shouted to be released from the room many times and that your staff did not respond, forcing her through the 40-minute duration of the escape experience. Neither you nor your employees heard anything through the door, but there is no footage of the incident to corroborate your testimony. If the court found your business liable, you could expect general liability insurance to help cover damages owed.

Other Types of Coverage Escape Room Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Escape room businesses require real estate and a substantial collection of physical assets including tools, props, costumes, and more. A policy of this kind is essential for the protection of equipment used in your carefully organized escape room scenarios, as well as any business-owned real estate. Fires, in particular, can be devastating to an escape room business, but violent storms and similar weather disasters may also lead to the damage or destruction of your expensive business assets. Commercial property insurance can protect a business against these and similar threats.

Business Interruption Insurance

While somewhat similar to commercial property insurance, business interruption policies offer equally important coverage for escape room companies. Covering disasters like those mentioned above, this insurance will assist in recovering estimated losses and cover temporary relocations during downtime that occurs due to weather or other disasters. This policy can ease the process of recovery after a business’ assets have been compromised.

Workers’ Compensation Insurance

You might begin an escape room business alone, but if your business is successful, you will probably want to grow and include more escape rooms or even new locations. Workers’ compensation insurance is necessary for companies that employ part-time or full-time workers. Most work-related accidents that cause injuries to employees will be covered in this policy.

Umbrella Insurance

This is a special kind of policy that functions atop existing policies. Essentially, it covers an even broader range of possible claims than individual policy limits will allow. As you operate your escape room business, you may be surprised to see how different customers behave in your rooms. Any unexpected claims that arise from these unpredictable encounters could be covered by the extended safety net of umbrella insurance.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your escape room business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Escape Room Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Next Insurance. Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

"Business insurance" is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

We do recommend purchasing adequate business insurance for your escape room before taking on your first customers to protect your company from financial risk. Your state also may require some types of business insurance, such as workers’ compensation, if you have employees. Always check local laws and regulations so that you don’t get in legal trouble for being underinsured.

Not necessarily. Certain exceptions may be written directly into your escape room business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.