Meals-to-Go Business Insurance

Getting insurance for your meals-to-go business is essential.

Meals-to-go businesses need to be protected against things like claims of false advertising, breaches of contract, and product liability.

For example, a customer becomes ill after eating one of your meals, or one of your chefs claims that you didn’t pay them in accordance with their contract.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Meals-to-Go Business

General liability insurance is — generally speaking — one of the most important insurance policies for meals-to-go businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

There are numerous policies available to your meals-to-go business that can extend the protection of general liability, such as:

- Commercial auto insurance: In each state, vehicles used mainly for business purposes (e.g., food delivery) on public roads are legally required to carry this policy.

- Product liability insurance: Protects your business from the financial consequences of lawsuits related to the meals it sells.

- Commercial property insurance: If any of your business’s expensive kitchen equipment is destroyed in an event like a fire or natural disaster, this policy will assist with the financial cost of replacing it.

When browsing the different options available to you when buying insurance, it is important to keep in mind the following two provider types:

- Traditional brick-and-mortar insurers — Characterized by tangible storefronts and their employment of insurance agents to offer quotes to customers.

- Online insurers — Characterized by little to no physical presence and an almost entirely online operation.

Overall, online insurers are greatly favored by small businesses as their price range is accessible, and their policies maintain the quality and accuracy of their more expensive alternatives.

Let's Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

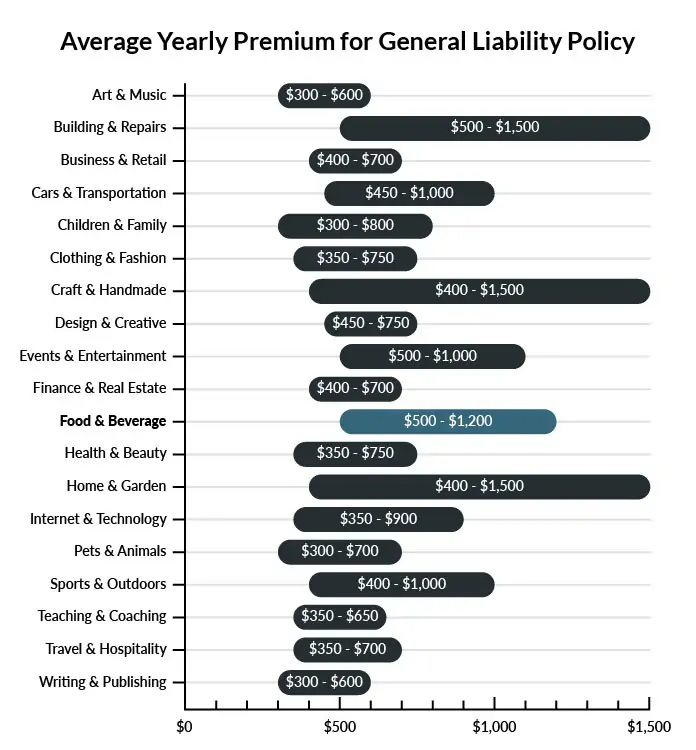

The average Meals-to-Go Business in America spends between $500 - $1,200 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a meals-to-go business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Meals-to-Go Business

Example 1: While delivering ingredients, a supplier trips over boxes left on the floor and is hurt in the fall. General liability insurance would probably cover their injuries.

Example 2: An employee trips while delivering a large order of finished pasta to a customer’s million-dollar home. The pasta spills out of the containers, and red sauce goes flying. The customer later sues because their expensive curtains, tablecloth, and carpet were all stained in the incident and are permanently ruined. General liability insurance would probably cover the damage.

Example 3: When conversing with a customer, an employee complains about the food at a local restaurant. The complaint is made in front of several people, and the restaurant owner eventually hears of the disparaging remarks. They file a slander lawsuit. General liability insurance would likely cover any legal costs and settlement.

Other Types of Coverage Meals-to-Go Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Auto Insurance

All states require businesses that use vehicles on public roads to carry minimum levels of auto coverage. What type of commercial auto insurance your business needs depends on what vehicles the business delivers meals with. Company-owned cars and vans usually must be insured with a traditional commercial auto policy. If deliveries are made via employees’ personal vehicles, a hired and non-owned auto policy might suffice. The latter provides certain protections only when a personal vehicle is used for work (not including commutes).

Commercial auto insurance is often bundled with other coverages in a package policy.

Product Liability Insurance

Product liability insurance offers protection against lawsuits related to products that a business makes or sells. Customers might file a suit if a product causes damage or harm. Food sold to customers meets the insurance definition of a product, which is why this insurance might be appropriate for your meals to go business. A policy may help your business if improperly prepared foods spread E. coli, if an unpitted olive causes someone to choke, or in other situations.

Product liability insurance is available through many package policies.

Home-Based Business Insurance

If you run a home-based meals to go business, you’ll likely want home-based business insurance. A policy will normally fill in some of the coverage gaps left by a homeowner’s insurance policy, which isn’t really intended to insure a business venture.

Home-based business insurance is available through a BOP, and some insurers offer it as an endorsement that can be added to their homeowner’s policies.

Commercial Property Insurance

If you operate from a company-owned kitchen, a property insurance policy will better meet your business’s insurance needs. This type of policy is commonly used to protect commercial properties and the equipment in them. Professional kitchen equipment is often expensive, so make sure you have enough property coverage to replace all of your stoves, ovens, refrigerators, freezers, fire sprinklers, and other equipment.

Property insurance is widely available through a BOP.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your meals-to-go business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Meals-to-Go Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Next Insurance. Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

"Business insurance" is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes, particularly due to the sheer amount of risks a meals-to-go business can expect to face. It is essential to acquire business insurance prior to launching as your business will encounter potentially financially damaging risks from its first day.

Additionally, neglecting insurance entirely can open your business up to legal liability in instances where certain policies are not optional (e.g., commercial auto insurance).

Not necessarily. Certain exceptions may be written directly into your meals to go business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability – that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.