School Supply Store Insurance

Getting business insurance for your school supply store is essential.

This is because school supply stores need to be protected against a variety of different risks, such as product liability claims, personal injuries, and employment law disputes.

Business insurance will also be pivotal when it comes to protecting your store’s equipment and inventory from potential damage or theft.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a School Supply Store

General liability insurance is — generally speaking — one of the most important insurance policies for school supply stores.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Having said that, it is important to note that your school supply store will likely benefit from purchasing additional coverage policies.

This is because a general liability policy will not be able to holistically cover it from all foreseeable risks, such as those that relate to:

- Bodily injuries as a result of a purchased product: This is covered via a product liability insurance policy instead.

- Employment law disputes: This is covered via a workers’ compensation insurance policy.

- Damage to or theft of store equipment: This is covered via a commercial property insurance policy.

You will also need to spend some time in order to find the right insurer for your small business.

Even though there are several great options available as of 2024, we recommend going with an online insurer (e.g., Tivly, Next, etc) instead of a brick-and-mortar alternative.

This is because online insurers use AI in order to offer personalized coverage — instead of a live insurance agent — and so can have significantly lower operating costs, allowing them to be more affordable.

Let's Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

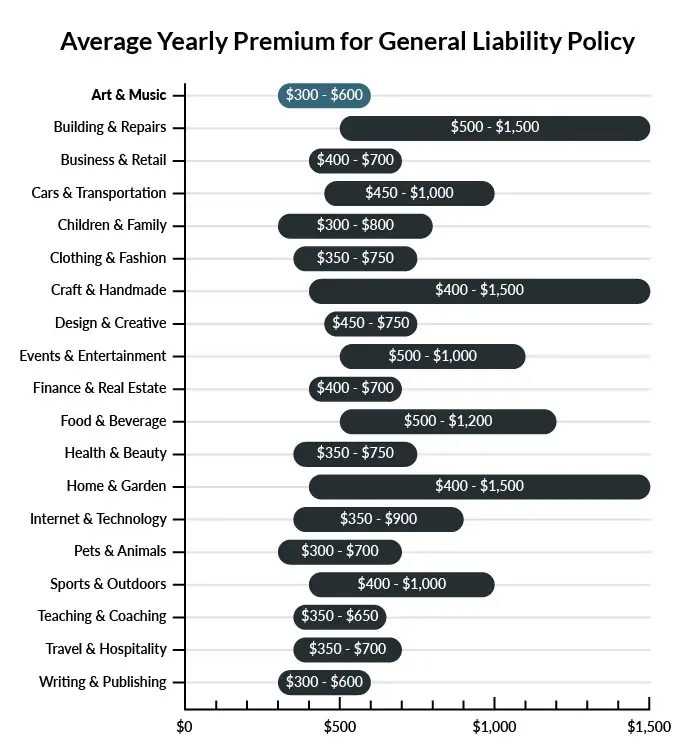

The average school supply store in America spends between $350-$600 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a school supply store to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our low-cost business insurance review.

Common Situations That General Liability Insurance May Cover for a School Supply Store

Example 1: An employee mops up a spill on the floor of your store but neglects to place a sign to indicate a slippery surface. A customer slips and falls, breaking her tailbone. She sues your business for medical payments and ongoing discomfort. If found liable, your business would probably be covered for payments or settlements through general liability insurance.

Example 2: A toddler is placed in the child seat of his mother’s shopping cart, but there is no seatbelt in this particular cart. The child squirms out and tips over the edge of the cart while his mother is not looking. He falls nearly four feet, landing on his head and sustaining a skull fracture. If held liable by a court, general liability insurance could probably help to cover any resulting settlement or payments for medical damages.

Example 3: A teacher from the local elementary school likes to drop by your storefront and chat as he picks up supplies for his next classroom project. Lately, he has developed a serious cough, becoming very ill and unable to work. An employee complains of comparable symptoms, and it is discovered that there is asbestos in the ceiling. If found liable, general liability insurance could probably assist in covering a settlement reached with the teacher or any medical payments mandated by the court.

Other Types of Coverage School Supply Stores Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Product Liability Insurance

School supply stores must exercise caution in the products they sell. Children represent vulnerable, developing minds, so if a product contains harmful materials or features dangerously sharp edges, a parent may elect to sue your business for a sizeable sum. Sometimes kids can break open a seemingly safe, child-friendly object, locating dangerous wiring or other hazards. If any of your products are considered as having injured a customer or their child, product liability insurance helps to cover any damages your company owes.

Commercial Property Insurance

Most businesses can benefit from a policy like this, and school supply stores are no exception. Events like fire and violent weather can leave your school supply storefronts at a major loss if the inventory is damaged. This policy can help to protect your business from disasters by covering losses of inventory, equipment, and owned commercial real estate.

Workers' Compensation Insurance

Any business that has part-time or full-time employees is legally required to provide some kind of compensation policy. This insurance covers your workers in the event of workplace accidents resulting in serious injury. Employees and their families can rest easier with this insurance in place, as it covers disability and/or death benefits for all workplace incidents. Keep your business running and your employees comfortable with a workers’ compensation policy.

Business Interruption Insurance

Following a disaster, your business may be forced to close for a period of time in order to make repairs and/or find a temporary location to operate out of. Business interruptions of this nature are often rife with recovery expenditures that can leave companies in a bad spot even after they manage to set themselves up again.

Business interruption insurance is designed to address exactly this issue. Addressing disasters like fire and tornadoes, an interruption policy will cover estimated profit losses and sometimes even temporary relocation costs, allowing a business to continue through its own period of recovery.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your school supply store:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

School Supply Store Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Next Insurance. Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

"Business insurance" is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Generally speaking, yes. Getting the right business insurance policies before you begin operating can play a pivotal role in your business’s long-term success.

This is because you will need to be insured before any liability arises, and this could theoretically happen as soon as you begin interacting with clients and/or purchasing store equipment.

Not necessarily. Certain exceptions may be written directly into your school supply store insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.