California Sales Tax Guide

California’s Sales Tax Rate: 7.25%

Maximum Local & County Rate: 2.00%

This guide simplifies compliance with California’s sales tax code by breaking down the process into four easy steps:

Use a Professional Service

TaxCloud automates sales tax calculation, filing, and compliance for just $19 per month.

Which Goods and Services Are Taxable?

Determining whether or not the products or services your company sells are taxable in California is the first step in sales tax compliance.

Traditional Goods or Services

Purchases of physical property, like furniture, home appliances, and motor vehicles, are subject to sales tax in California.

Groceries and prescription medications are tax-exempt.

California charges a reduced rate on the purchase of gasoline (2.25% plus applicable district taxes) or farm and manufacturing equipment (3.3125% plus applicable district taxes).

Some services in California are subject to sales tax. For a detailed list of taxable services visit the California Society of CPA’s website.

The California State Board of Equalization has also published a comprehensive guide to sales tax exemptions and exclusions.

Digital Goods or Services

A digital good or service is anything electronically delivered, such as an album downloaded from iTunes or a film purchased from Amazon.

California State does not require businesses to collect sales tax on the sale of digital goods or services.

However, California has one exception to this policy. Businesses must collect sales tax on pre-written computer software that is sold online.

How to Register for California Sales Tax

If you have determined that you need to charge sales tax on some or all of the goods and services your business sells, your next step is to register for a seller’s permit. This allows your business to collect sales tax on behalf of your local and state governments.

In order to register, you will need the following information:

- Your social security number (corporate officers excluded)

- Your date of birth

- Your state ID number, driver license number, or other ID (e.g., passport, military ID)

- Names and location of banks where you have an account

- Names and addresses of suppliers

- Name and address of bookkeeper or accountant

- Name and address of personal references

- Expected average monthly sales and the amount of those sales which are taxable

- Your email address

- If you have purchased an existing business, you must also provide the previous permit information

Register for a Seller’s Permit

Register for a Seller’s Permit online through the California Department of Tax and Fee Administration

Get StartedSave Money with a Resale Certificate

With a resale certificate, also known as a reseller’s permit, your business does not have to pay sales tax when purchasing goods for resale.

Download Resale Certificate

Download the Resale Certificate through the California Department of Tax and Fee Administration

Download FormInstruction: Present the certificate to the seller at the time of purchase.

Collecting Sales Tax

After getting your seller’s permit and launching your business, you will need to determine how much sales tax you need to charge different customers. To avoid fines and the risk of costly audits, it’s important for business owners to collect the correct rate of sales tax.

When calculating sales tax, you’ll need to consider the following kinds of sales:

- Store Sales

- Shipping In-State

- Out-of-State Sales

Recommended: Use our Sales Tax Calculator to look up the sales tax rate for any Zip Code in the US.

Store Sales

For traditional business owners selling goods or services on site, calculating sales tax is easy: all sales are taxed at the rate based on the location of the store.

Here’s an example of what this scenario looks like:

Mary owns and manages a bookstore in San Diego, California. Since books are taxable in the state of California, Mary charges her customers a flat-rate sales tax of 7.75% on all sales. This includes California’s sales tax rate of 7.250%, and Mary’s local district tax rate of 0.500%.

In-State Sales

When shipping to customers in the state of California, your tax rate will depend upon the county and city tax districts that your business and customer share in common. This concept is illustrated by the three scenarios below:

Shipping to a Customer in your City

When shipping to customers in the same city and county as your business, you’ll be responsible for collecting state, county and city sales tax.

Shipping to a Customer in your County

When shipping to customers in a different city, but within the same county as your business, you’ll be responsible for collecting state and county sales tax. You will not be responsible for collecting city sales tax on behalf of your customers.

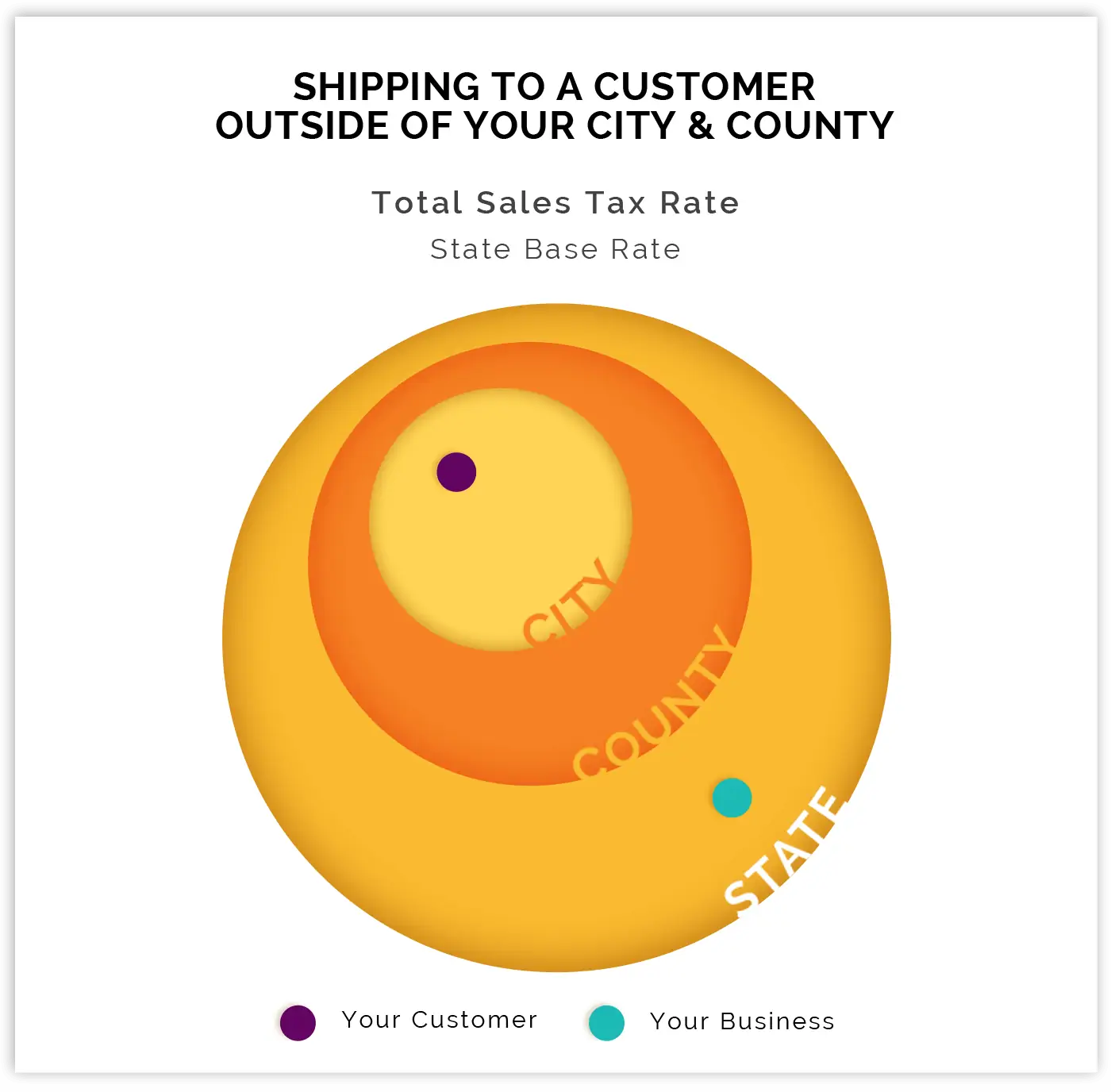

Shipping to a Customer Outside your City and County

When shipping to customers outside of your business’s city and county, you will only need to collect sales tax at California’s base tax rate. You will not be responsible for collecting county or city sales tax on behalf of your customers.

Out-of-State Sales

California businesses only need to pay sales tax on out-of-state sales if they have nexus in other states. Nexus means that the business has a physical presence in another state.

Common types of nexus include:

- A physical location, such as an office, store, or warehouse

- An employee who works remotely or who is a traveling sales representative

- A marketing affiliate

- Drop-shipping from a third party seller.

- A temporary physical location, including festival and fair booths.

File Your Sales Tax Return

Now that you’ve registered for your California seller’s permit and know how to charge the right amount of sales tax to all of your customers, you are all set to file your sales tax return. Just be sure to keep up with all filing deadlines to avoid penalties and fines.

Let TaxCloud Collect and File Tax For You

Schedule a call with TaxCloud today to learn more about how their team calculates, collects, and files sales taxes for your business.

How to File

California requires businesses to file sales tax returns and submit sales tax payments online.

File the California Tax Return

File with the California Department of Tax and Fee Administration

File OnlineHow Often Should You File?

How often you need to file depends upon the total amount of sales tax your business collects.

- Annual filing: If your business collects less than $100.00 in sales tax per month then your business should file returns on an annual basis.

- Quarterly filing: If your business collects between $100.00 and $1200.00 in sales tax per month then your business should file returns on a quarterly basis.

- Monthly filing: If your business collects more than $1200.00 in sales tax per month then your business should file returns on a monthly basis.

Note: California requires you to file a sales tax return even if you have no sales tax to report.

Filing Deadlines

All California sales tax return deadlines fall on the last day of the month, unless it is a weekend or federal holiday, in which case the deadline is moved back to the next business day.

2018 California Sales Tax Filing Deadlines

Annual filing: January 31

Quarterly filing:

- Q1 (Jan. – Mar.): April 30

- Q2 (April – June): July 31

- Q3 (July – Sept.): October 31

- Q4 (Oct. – Dec.): January 31

Monthly filing: The last day of the following month, or the next business day, e.g. April 30 for the month of March, or May 31 for the month of April.

Penalties for Late Filing

California charges a 10.00% of the total amount of sales tax owned fine for late filing.

California Helpful Resources

Board of Equalization Publication 44 – District Taxes

Publication 44 is the comprehensive guide to understanding District Sales Taxes in the State of California. It explains the basics, as well as special circumstances that may occur and how to handle them.

Board of Equalization Publication 73 – Your California Seller’s Permit

Your California Seller’s Permit is a complete explanation for everything related to obtaining and dissolving a seller’s permit, and collecting and filing sales tax in the State of California.

Board of Equalization Publication 100 – Shipping and Delivery Charges

This publication is a short concise overview is a list of suggestions and tips for business owners who must ship their products across California. It also features a handy reference chart for certain shipping scenarios that will be helpful in answering questions about applying the proper sales tax to items.

Board of Equalization Publication 105 – District Taxes and Delivered Sales

Publication 105 is a slightly longer publication than Publication 100, and is designed to help summarize the tax laws as they apply to District Taxes.

General Tax Enquiry – California Board of Equalization:

1 (800) 400-7115