Sole Proprietorship

A sole proprietorship is a business owned by an individual that isn’t formally organized. A sole proprietor files taxes under their own name and is personally liable for any debts or legal actions taken against the business.

Topics:

Sole Proprietorship Meaning | Sole Proprietorship Definition

A sole proprietorship is a business owned by an individual that isn’t formally organized. A sole proprietor files taxes under their own name and is personally liable for any debts or actions taken against the business.

Sole proprietorships are popular with many business owners because of how simple they are to form and maintain, although they have disadvantages as well.

Should I Form a Sole Proprietorship?

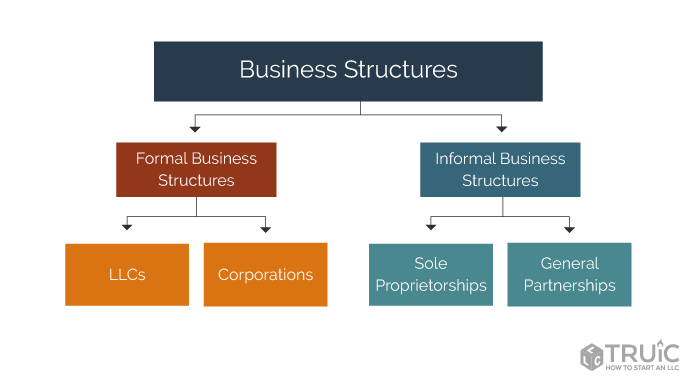

Sole proprietorships have several advantages over formal business structures like corporations and limited liability companies (LLCs), including:

- Less paperwork: Corporations and LLCs require you to file several forms and other paperwork, both during the startup process and during the normal course of business, but sole proprietorships can usually be formed without any paperwork at all.

- Lower startup and maintenance costs: Along with less paperwork comes less filing fees and other related expenses.

- Less regulation: Sole proprietorships generally have less reporting requirements and regulations.

However, sole proprietorships also come with several disadvantages, including:

- No personal liability protection: Owners of sole proprietorships are liable for any debts or legal judgments the business incurs.

- No tax benefits: Sole proprietors must pay income tax on all profits as well as self-employment tax.

- Limited growth potential: Because of the lack of liability protection, sole proprietorships are ill-suited for growing businesses.

- Less credibility: Unless they register a “doing business as” (DBA) name, sole proprietorships must operate under the legal name of the owner, which could make the business seem less professional to customers and potential investors.

A sole proprietorship could be a good option if your business has the following characteristics:

- Your business is low-profit and low-risk: Because there is no personal liability protection with a partnership, there should be a low chance of financial loss.

- You have a small customer base: If your customer base goes beyond friends and family, there is increased risk.

- You started your business as a hobby: Partnerships are often a good option as you transition an activity from just a hobby to a small business.

If your business does not check each of these boxes, you may want to consider the advantages of forming an LLC. Starting one is easy with our How to Form an LLC guide.

How to Form a Sole Proprietorship

One of the biggest advantages of a sole proprietorship is that they are very easy to form. In fact, they typically don’t require any paperwork to start in most states — you can simply start doing business under your own name. However, it may be a good idea to register a DBA for the business. This will allow you to operate under a different name than your personal legal name.

Sole Proprietorship Taxes

Because a sole proprietorship is an informal business structure and not a separate legal entity, it is indistinguishable from its owner for tax purposes.

Sole proprietorships are considered pass-through entities, which means all of the business’s profits or losses pass through directly to the owner’s individual income tax filing rather than being subject to some sort of corporate tax. The tax rate on the business’s profits will depend on the owner’s personal tax bracket.

In addition to personal income tax, sole proprietors must pay a 15.3% self-employment tax. This covers both the employer and employee share of Social Security and Medicare tax.

How to Start a Business

Once you have learned about the advantages and disadvantages of a sole proprietorship and decided if it is the right business structure for you, you will need to actually form and set up the business. Whether you choose to form a sole proprietorship or some other structure, there are more things to take care of before you are ready to sell your products or services.

You can read these in more detail in our state-by-state How to Start a Business guides, but here is a quick rundown of some basic steps after forming your business:

- Register for taxes

- Create business banking and credit accounts

- Set up accounting

- Obtain permits and licenses

- Get insured

- Establish a web presence

Sole Proprietorship FAQ

What are the advantages and disadvantages of a sole proprietorship?

Sole proprietorships are easy and inexpensive to start and maintain, but they don’t offer any personal liability protection or tax advantages.

How is a sole proprietorship formed?

In most states, there are no filings or fees required to form a sole proprietorship — you only need to start doing business under your own name.

How are sole proprietorships taxed?

Sole proprietorships are subject to pass-through taxation, which means the profits or losses of the business pass through to the owner’s individual tax return without being taxed at the company level. Sole proprietors must also pay self-employment tax.

Do sole proprietors need to file quarterly taxes?

Yes. The Internal Revenue Service (IRS) requires sole proprietors to pay estimated quarterly income tax if they expect to owe $1,000 or more for the year.

How do I pay myself as a sole proprietor?

You can pay yourself as a sole proprietor by withdrawing money from your business bank account. This is commonly called a “draw.”

Can a sole proprietor put themself on payroll?

Sole proprietors do not receive salaries as part of the company’s payroll.

Can you have employees with a sole proprietorship?

Yes, but having employees as a sole proprietorship is uncommon.

Is a single-member LLC the same as a sole proprietorship?

No. A single-member LLC is a formal business structure with one owner. Single-member LLCs are taxed in the same way as sole proprietorships.