Hot Tub Garden Business Insurance

Getting insurance for your hot tub garden is essential.

Hot tub gardens need to be protected against things like claims of premises liability, personal injury, and contractual breaches.

For example, a customer seriously injures themselves after trying to climb out of a hot tub, or you accidentally fail to pay your employees by the agreed-upon date.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Hot Tub Garden

General liability insurance is — generally speaking — one of the most important insurance policies for hot tub gardens.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

There are a number of policies that can be used to supplement the protection of general liability, such as:

- Commercial property insurance: An invaluable policy for hot tub gardens, this covers the cost of any repairs or replacement of the expensive equipment required to run this business.

- Workers’ compensation insurance: Provides protection for injuries or illnesses suffered by employees while at work. Required by law in many states for businesses with at least a few employees.

- Business interruption insurance: Steady income is important to the survival of small businesses. This policy ensures that any interruption in your hot tub garden’s operation will not be fatal by covering any loss of income during such a period.

Despite initially seeming difficult, the decision of which insurance provider to select becomes much easier when you start with which category better meets your business’s needs. The two main options are:

- Traditional brick-and-mortar insurers — Refers to firms such as Hiscox and Nationwide, which have physical premises and storefronts as well as insurance agents to assist their customers.

- Online insurers — Refers to firms such as Ergo Next and Tivly, which do not own any physical storefronts, and are instead based entirely online.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

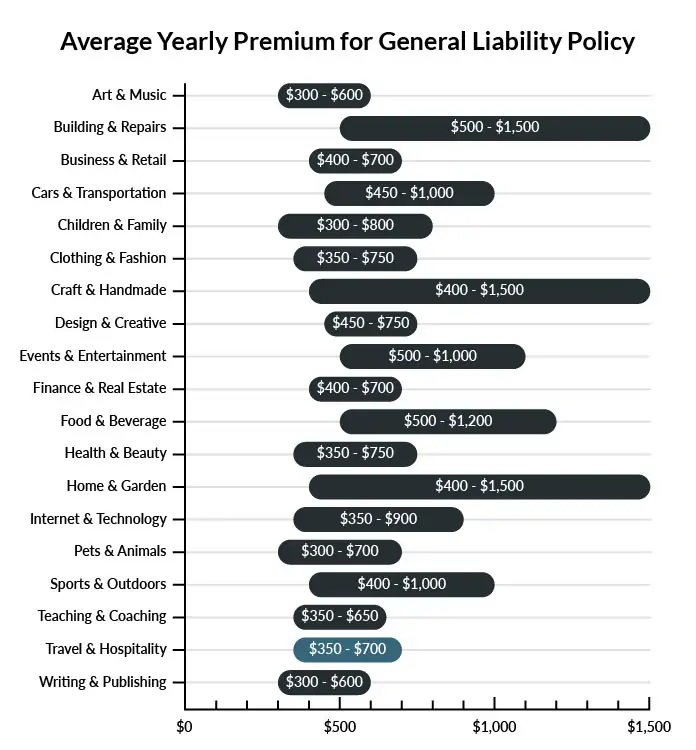

On average, hot tub gardens in America spend between $350 – $700 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a hot tub garden to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Hot Tub Garden

Example 1: Your employee uses too many chemicals when caring for the hot tubs, causing severe chemical burns on several people. As a result, there are several lawsuits against the business for damages. General liability will cover your cost for legal representation and damages awarded by the courts.

Example 2: A client slips when getting out of the hot tub. The resulting concussion has left her out of work for several weeks, and she has accrued a mountain of medical bills. She is seeking reparations from your business. Your general liability insurance should cover her medical bills as well as any potential lawsuit expenses on your part.

Example 3: The business that built your new website used a photo covered under copyright law. They are suing you and the site designer for copyright infringement. Your general liability policy will pay for your legal expenses and the damages the courts have ordered you to pay.

Other Types of Coverage Hot Tub Gardens Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Owning a business in this industry requires investment in expensive equipment. To protect your investment, owners should purchase a commercial property insurance policy. In the event of a loss, this policy would pay to repair or replace the building and its business contents.

If your space is a rental, you will still want to purchase a commercial property policy. Coverage will be limited to business property kept onsite. Some leases now require renters to cover certain parts of the building, such as air conditioning units. Review the terms of your lease with your insurance agent to identify any other beneficial endorsements.

Workers Compensation Insurance

State law requires that businesses carry workers compensation insurance for anyone that is on the payroll. It provides protection for employees with on-the-job injuries, paying both their medical bills and lost wages. Additionally, if an accident results in a lawsuit, the policy affords legal representation to the business owner.

Workers compensation is generally purchased as a standalone policy.

Business Interruption insurance

Most small business owners rely on steady revenue to pay their ongoing professional and personal expenses. If the company shuts down for an extended period after a loss, business interruption insurance can help keep the company afloat during repairs.

This coverage is often offered as part of a business owners’ policy (BOP) package.

Commercial Umbrella Liability Insurance

Organizations facing higher liability risks should purchase a commercial umbrella liability policy. If a lawsuit exhausts the limits of the underlying general liability policy, the umbrella policy will take over. This added layer of coverage protects your assets, helping to ensure your personal finances are not in danger.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your hot tub garden:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Hot Tub Garden Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

As a customer focussed business, business insurance will be essential for your hot tub garden to operate safely — especially insurance obtained before the garden opens.

It is also important to remember that, due to the amount of staff required to run a hot tub garden, your business may be obligated by law to acquire workers’ compensation insurance (among other policies).

Not necessarily. Certain exceptions may be written directly into your hot tub garden insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.