How to Start a Corporation

Starting a corporation is easy with our 5 step guide. You can start a corporation by filing formation documents with your state and setting up a board of directors.

We’ll show you how to start a corporation yourself below.

Or, you can hire a trusted professional service to help:

Start a Corporation in 5 Easy Steps

A corporation is a registered business treated as a separate legal entity from its owners, also known as shareholders, and guided by a board of directors.

Not sure if a corporation is right for you? Visit our LLC vs Corporation guide to find out which structure is best for your small business.

We provide detailed state-specific instructions and important links in our How to Start a Corporation state guides:

- Alabama

- Alaska

- Arizona

- Arkansas

- California

- Colorado

- Connecticut

- Delaware

- Florida

- Georgia

- Hawaii

- Idaho

- Illinois

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

- Nebraska

- Nevada

- New Hampshire

- New Jersey

- New Mexico

- New York

- North Carolina

- North Dakota

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Vermont

- Virginia

- Washington

- Washington D.C.

- West Virginia

- Wisconsin

- Wyoming

You can start your own corporation in 5 easy steps:

- Step 1: Name Your Corporation

- Step 2: Choose a Registered Agent

- Step 3: Hold an Organizational Meeting

- Step 4: File the Formation Documents

- Step 5: Get an EIN

Step 1: Name Your Corporation

Choosing a business name is the first step in starting a corporation. You must choose a unique name that complies with your state’s corporate name requirements.

1. General Corporate Name Guidelines:

- Your name must contain the word “corporation,” “company,” “incorporated,” “limited” or an abbreviation of one of these terms.

- Your name must be distinguishable from any existing business in your state. This often includes a state’s reserved names.

- Your name cannot use the words “bank,” “trust,” “trustee,” “credit union,” or related words without approval.

- Your name cannot include words that could confuse your corporation with a government agency (FBI, Treasury, State Department, etc.).

2. Is my corporation name available?

Your corporation’s name should be unique and distinguishable from other business names.

For name search instruction in your state, choose your state from the drop-down in our Business Name Search guide.

3. Is the URL available?

Before you register your corporation, you should see if a good URL is available for your desired business name. Even if you aren’t planning on creating a business website now, we advise buying a web domain right away to prevent other businesses from securing it.

We recommend using GoDaddy to search for your domain name.

After choosing a domain name for your corporation, consider setting up a business phone system to improve your customer service and build credibility. We recommend Phone.com because of its many useful features. Start calling with Phone.com.

Need Help Naming Your Business?

Use our Corporation Name Generator to brainstorm your business’s perfect name. For more help, visit our free How to Name a Business guide. Then, create a logo with our free Logo Maker.

FAQ: Naming a Corporation

Naming your business involves several variables. From naming guidelines to brainstorming your brand, we have it covered.

To learn more about naming a business, visit our How to Name a Business guide and choose your state from the drop-down menu.

You will need to set up a DBA to operate under a name other than your legal name. Some states also require certain business types to file a DBA.

To learn more about DBA guidelines in your state, visit our How to File a DBA guide and select your state from the drop-down menu.

Step 2: Choose a Registered Agent

You must appoint a registered agent when you register your corporation with the state. Some states refer to registered agents as statutory agents, resident agents, or agents for service of process.

What is a Registered Agent? A registered agent is an individual or entity that has been appointed by an LLC or corporation to receive service of process, government correspondence, and compliance documents on behalf of a business. To learn more, read our What is a Registered Agent guide.

Who Can Be a Registered Agent? Your registered agent can be an individual, business entity, or professional registered agent service. Any member of the corporation or individual can serve as your registered agent as long as the person:

- is 18 years or older

- has a physical address in the state where business activity is conducted

- is available (in person) during normal business hours

Designating someone else to serve as a registered agent for your LLC or corporation has its benefits. To learn more about hiring a registered agent service for your corporation, read our Should I Use a Registered Agent Service guide.

Recommended: Northwest includes registered agent service with their incorporation package ($29 for the 1st year + State Fees).

FAQ: Choosing a Registered Agent

Using a professional registered agent service is an affordable way to manage government filings for your corporation. For most businesses, the advantages of using a professional service significantly outweigh the annual costs.

For more information on how to set up a registered agent in your state, visit our What is a Registered Agent guide and choose your state from the drop-down menu.

If you don’t have a registered agent, there are negative consequences in most states. Your business could be penalized with lawsuits and fines, lose good standing with the state, and could eventually be dissolved.

Step 3: Hold an Organizational Meeting

Before you officially file the formation documents in Step 4, you will need to hold an organizational meeting to complete the following tasks:

- Fill-out and execute the articles of incorporation (see Step 4 below)

- Create and approve bylaws

- Select your initial director(s)

- Determine your share structure

- Execute an Incorporator’s Statement

Create and Approve Corporate Bylaws

Bylaws are the rules that determine how your organization will be governed and run. You can think about the bylaws as a constitution for your corporation. It makes the rules and priorities clear for everyone involved.

A corporation’s bylaws will supplement any rules set forth by the federal government or the state.

In your bylaws, be sure to include:

- How the corporation will be governed, including the role of directors and officers

- How meetings are held, voting procedures, electing officers or directors

- How records will be kept and managed

- How disputes will be handled

- How bylaws will be added/amended in the future

- The date of the annual shareholders’ meeting

- How to negotiate contracts

- Fiduciary duties to the corporation (i.e. acting in the best interests of the corporation)

- What constitutes a quorum for voting purposes

What is a Quorum? A quorum is the minimum number of members of an assembly that must be present at a meeting to make the meeting valid, or any of the votes held therein.

Ready to get started? These bylaws templates can be customized to suit the needs of your incorporated business.

Appoint Initial Directors

You must appoint the state’s required number of directors until the first shareholders’ meeting.

A corporate director is in charge of the adoption, amendment, and repeal of operational bylaws as well as the election, supervision, and removal of officers.

After forming the corporation, the incorporator(s) — or initial director(s), if named on the formation documents — should call an organizational meeting. During this initial meeting, either the incorporator(s) will elect the board of directors or the initial director(s) will appoint the officers.

Choose a Share Structure and Strategy

A share of stock is the unit of ownership of a corporation. Each share of stock represents a percentage of ownership of the company. For example, if a corporation issues one share of stock the shareholder (stock owner) would then own 100% of the corporation.

Shares can be structured into classes. Each class, termed a share class, holds different rights and privileges. You can have multiple classes and each class can hold any number of shares.

Authorized Shares: the number of shares the corporation is allowed to issue.

Issued Shares: the total number of shares actually issued to shareholders.

Share Class: a group of shares that has a unique set of rights and privileges.

Some states only allow corporations to list one class of shares on their provided formation document. In these cases, you must either complete an additional provision or draft your own formation documents. Check with your state for further instructions.

NOTE: We recommend starting with a high number of authorized shares. Many attorneys suggest 10 million. By starting with a high number, you have the flexibility to issue shares as needed without paying legal fees to increase your initial authorized shares amount.

Create and Execute an Incorporator’s Statement

The incorporator(s) should sign an Incorporator’s Statement with complete names and addresses of each initial director and store it in the corporate records book.

This document names the initial director(s) that will serve until the board of directors is elected during the first shareholder’s meeting. It should be stored with the rest of your corporate records.

FAQ: Initial Directors & Share Structure

A corporate director is in charge of the adoption, amendment, and repeal of operational bylaws as well as the election, supervision, and removal of officers.

A share class is a group of shares that has a unique set of rights and privileges compared to other shares of the same corporation.

Step 4: File the Formation Documents

You will need to file formation documents with your state.

For state-specific formation information, choose your state from this drop-down.

Once the documents are approved, you will have officially formed a corporation. Most states provide the formation documents online, while others require you to draft your own formation documents.

The formation documents will cover the basics of your corporation, including:

- Corporate name and principal address

- Corporate service of process agent name and street address

- The number of authorized shares the corporation is allowed to issue

Some states only allow corporations to list one class of shares on their provided formation document. In these cases, you must either complete an additional provision or draft your own formation documents.

FAQ: Corporate Formation

An S corporation is a tax designation that can be used by corporations and LLCs alike. S corporations are taxed as pass-through entities. This means that S corps do not pay federal taxes on their business income. Instead, the profits of the business “pass-through” to the owners of the S corp, who are also known as shareholders.

Read our What is an S Corporation article to learn more.

A C Corporation is the default structure of an incorporated company. It’s a separate legal entity from its owners with a basic operational structure consisting of shareholders, officers, directors, and employees.

Read our What is a C Corp article to learn more.

New corporations should list a high number of authorized shares on their formation documents. Most legal and business professionals recommend 10 million shares be authorized when a corporation is formed.

Authorized shares are the number of shares that a corporation is allowed to issue. This number is initially set by the incorporator on the corporation’s formation documents and can be increased later by going through a legal process. Issued shares are the shares that have actually been distributed to shareholders.

Step 5: Get an EIN

What is an EIN? An Employer Identification Number (EIN), or Federal Tax Identification Number (FTIN), is used by the federal government to identify a business entity. It is essentially a social security number for the company.

Why do I need an EIN? An EIN is required for the following:

- To open a business bank account for the company

- For Federal and State tax purposes

- To hire employees for the company

How do I get an EIN? An EIN is obtained from the IRS (free of charge) by the business owner after forming the company. This can be done online or by mail.

Get an EIN

Option 1: Request an EIN from the IRS

– OR –

Option 2: Apply for an EIN by Mail or Fax

Mail to:

Internal Revenue Service

Attn: EIN Operation

Cincinnati, OH 45999

Fax: (855) 641-6935

Fee: Free

How to Run Your Corporation

It is very important to adhere to the formalities of running a corporation. In order to protect your personal assets, and not allow creditors or municipalities to pierce your corporate veil, you must:

- Maintain up-to-date bylaws

- Set up a corporate records book

- Hold required annual meetings

- Give notice of meetings when applicable

- Keep accurate meeting minutes

Maintain Your Corporation’s Bylaws

You must maintain up-to-date bylaws to protect your corporate veil.

If you want to amend a section or article of your corporation’s bylaws, you must call a special meeting with the board of directors. During this meeting, a copy of your proposed changes should be distributed to the board members. Depending on your bylaw structure, either a majority vote or minimum vote will be required to pass the amendment.

After the first meeting, notices must be sent to the corporation’s shareholders. A second meeting will need to be held with all voting parties to either approve or disapprove your proposed amendments.

Set Up a Corporate Records Book

Think of this as the hard-copy record book where all critical corporate documents are kept, like your California Articles of Incorporation, bylaws, meeting minutes, stock certificate ledger, stock transfer documents, etc.

You should keep the corporate records book at your principal location. Corporate records book kits can be purchased online, or you can use a large generic binder to store your records.

Hold Periodic Board Meetings and Record Minutes

You must hold regular corporate meetings to maintain your business’s management structure.

Annual Shareholders’ Meeting

Corporations in most states must hold an annual shareholders’ meeting. The first annual shareholders’ meeting should occur soon after formation. During this meeting, the shareholders elect the board of directors. Your corporate bylaws should note the date of your annual shareholders’ meeting.

Special Meetings

Corporations might also need to conduct “special” board of director’s meetings. These meetings are called to discuss important business matters that will affect the corporation. Your state may have unique meeting notice requirements for special meetings.

Notice of Meetings

If your corporation has more than one shareholder, you will need to provide formal notice of meetings to owners (shareholders), employees, and officers before the meeting occurs. The notice must provide the following information:

- Whether the meeting is a regular or special meeting

- Where the meeting will be held

- When the meeting will occur

When a meeting must be held at the last minute, without formal notice of the meeting, a waiver of notice must be signed by all eligible people stating that they are giving up the right to receive formal notice as laid out in the bylaws and formation documents.

Meeting Minutes

Meeting minutes are not legally required in some states, but they are necessary. Well-recorded minutes are indispensable during disputes and court actions.

For single-shareholder corporations (common for small business owners), minutes general only need to record the following:

- The date of the meeting

- A note that it was a joint meeting of the shareholders and board of directors

- When the next election of the board of directors will meet if that date is part of your corporate bylaws

Several companies offer corporate minutes templates. To learn more, read our review of the Best Corporate Meeting Minutes Templates.

Research Corporate Licenses and Permits

Do I need business licenses and permits?

To operate your corporation, you must comply with federal, state, and local government regulations. For example, restaurants likely need health permits, building permits, signage permits, etc.

The details of business licenses and permits vary from state to state. Make sure you read carefully. Don’t be surprised if there are short classes required as well.

Fees for business licenses and permits will vary depending on what sort of license you are seeking to obtain.

Obtain the correct business licenses and permits for your corporation, or have a professional licensing service do it for you:

- Federal: Use the U.S. Small Business Administration (SBA) guide to federal business licenses and permits.

- State: Visit our How to Start a Corporation state guides for links to your state’s licensing requirements.

- Local: Contact your local county clerk and ask about local business licenses and permits.

Protect Your Business & Personal Assets

To maintain personal asset protection, it is essential to have dedicated business banking and business credit accounts.

When your personal and professional accounts are mixed, personal assets like your home or vehicle are at risk in the event your corporation is sued. This is also known as piercing the corporate veil.

You can protect your corporation by following these two steps:

1. Get a Business Bank Account

Opening a business bank account protects your personal assets and legitimizes your corporation. Separating your professional account from your personal account also simplifies your business’s tax filing and accounting processes.

To open a bank account for your corporation, you will need an Employer Identification Number (EIN) and your corporation’s formation documents.

For a look at our favorite business checking accounts, visit our Best Banks for Small Business review.

2. Open a Business Credit Card

Much like a business bank account, a dedicated business credit card will help your California corporation separate your personal and professional expenses.

In addition to this, a business credit card will also help build your business’s credit history, which can be used to raise capital for your corporation. A higher business credit score will also help your business obtain loans and higher credit limits later on.

Small business credit cards also offer benefits that personal credit cards do not, such as business-specific cash back rewards and travel perks. Learn about the best small business credit cards here.

Recommended: Visit BILL to apply for their easy-approval business credit card and build your business credit quickly.

3. Hiring a business accountant:

- Prevents your business from overpaying on taxes while helping you avoid penalties, fines, and other costly tax errors

- Makes bookkeeping and payroll easier, leaving you with more time to focus on your growing business

- Helps effectively manage your business funding and discover areas of unforeseen loss or extra profit

For more business accounting tools, read our guide to the best business accounting software.

Recommended: Find out how much you could be saving today by trying our recommended accounting software.

Get Insurance

Business insurance helps you manage risks and focus on growing your corporation. The most common types of business insurance are general liability insurance, professional liability insurance, and workers’ compensation.

- General Liability Insurance protects your business from lawsuits. Most small businesses get general liability insurance.

- Professional Liability Insurance covers claims of malpractice and other business errors for professional service providers (consultants, accountants, etc.)

- Workers’ Compensation Insurance provides coverage for employees’ job-related illnesses, injuries, or deaths. Get a free quote with ADP.

Protect your Business with Insurance

Get a quote with Ergo Next and find an insurance product tailored to your needs. It only takes a few minutes.

Properly Execute Legal Documents

Signing a legal document improperly can leave you open to personal liability. You must sign as a representative of the business and not as yourself. When signing legal documents on behalf of your corporation, follow this formula to avoid problems:

- The formal name of your business

- Your signature

- Your name

- Your position in the business as its authorized representative

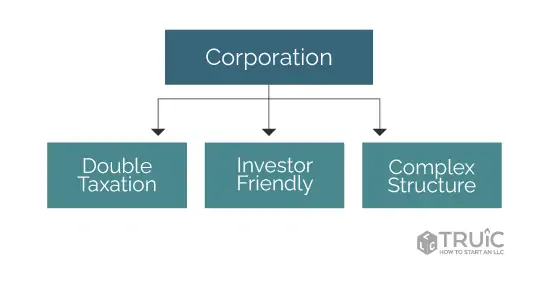

Is Starting a Corporation Right for Your Small Business?

A limited liability company (LLC) is usually the best business structure for most small businesses because it offers liability protection like a corporation but unlike a corporation, it has a simple tax structure and simple maintenance requirements.

Our Form an LLC guide offer simple step-by-step instructions for forming an LLC.

When to Form a Corporation

Most small businesses start as limited liability companies (LLCs) but there are some instances when starting as a corporation makes sense.

Your small business would benefit from a corporate structure if:

- you need to carry significant profit over from tax year to tax year

- you need to attract venture capitalist and investors

- there is benefit in managing a complex business structure

Profit Carryover from Year to Year

If a small business is unable to spend a significant amount of its profit during a tax year on expenses to grow the business, it could make sense to structure the business as a corporation rather than an LLC. This is because of the difference in the way the two business entities are taxed.

A corporation is taxed at about 15% for all profits that carry over to the next tax year. In this same scenario, an LLC member’s tax burden would be greater because they pay FICA taxes and federal and state income taxes, which are higher than the 15% corporate rate.

That said, a business owner who anticipates needing to carry profit into the next tax year should look closely at the financial benefits of forming a corporation.

Venture Capital and Investors

If you need to attract investors, starting a corporation could be the best choice for your small business.

An investor in a corporation pays taxes on dividends only when they receive them whereas an investor in an LLC would have to pay taxes regardless of whether they received a distribution or not. The LLC investor might never see a return on their investment but might have to pay taxes every year regardless. This is why investors prefer C corps.

Managing a Complex Business Structure

If the benefits of managing a complex business structure outweigh the costs, starting a corporation could make sense for your small business.

Corporations are more complex organizations compared to LLCs, with increased administrative overhead, more paperwork, and complex compliance requirements. Managing a corporation may require help from an attorney or accountant which can increase overall business costs.

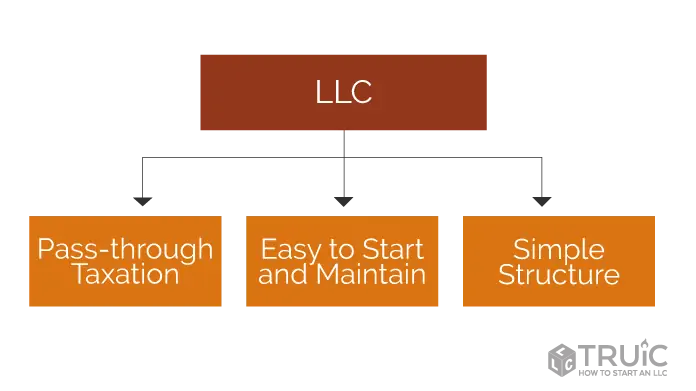

When to Form an LLC

Most small businesses start as limited liability companies (LLCs). An LLC is most likely the best structure for your business if:

- you need liability protection

- you plan to invest most of your profit back into the business each year

- you would benefit most from an easy to maintain business structure

Reinvesting LLC Profit and Pass-Through Taxation

If you expect to reinvest most of the profit back into your small business, an LLC is the right choice.

Small businesses usually carry very little profit from one tax year to the next. This is because small businesses usually spend most of their income on expenses like marketing, software, and office equipment to help the business grow. But, why does this matter?

Pass-Through Taxation

Pass-through taxation means the net income (profit minus expenses) of the business passes through to the LLC member(s) individual tax returns. This means the business itself will not be taxed and you will only be taxed on the business’s net income on your individual tax return.

Corporate income is taxed twice and one of those times occurs prior to expenses being deducted. This is not a good scenario for a small business that is reinvesting its profits to promote growth.

To learn more, read our LLC vs Corporation guide.

LLCs are Easy to Start and Maintain

Limited liability companies (LLC) are a simple business structure: they require less paperwork, less administrative overhead, and are much easier to start and maintain than a corporation.

LLCs are also adaptable and can elect to become corporations at a later date. This makes LLCs a great starting point for your business to grow.

Corporation FAQ

There are a number of good reasons to form a corporation. Some of the advantages include:

- Limited liability protection

- Unlimited capital generation

- Corporate tax benefits

- A more formal management structure

- Appeal to investors

To fully realize the benefits of incorporating, you will want to consider your company’s capital needs, profits, and management and ownership structure to make sure forming a corporation is the best business structure for you.

To learn more about what business structure is best for you, read our How to Choose a Business Structure guide.

The best type of corporation for your business depends on many factors. Here are some different types of corporations:

- C Corporations (C Corps) are owned by stockholders, have a board of directors, and hold annual meetings.

- S Corporation (S Corp) is a type of tax classification. Unlike a C Corp, an S Corp can pass-through income to its shareholders for tax purposes. S Corps are limited to 100 shareholders.

- Professional corporations are generally for corporations that require certain licensed individuals (e.g., doctors, attorneys, etc.).

- Nonprofit corporations use profits to advance the company’s mission rather than distributing them to shareholders.

You should carefully consider your business’s structure, goals, and financial situation before selecting your corporate structure.

A limited liability company (LLC), unlike a sole proprietorship or a general partnership, offers personal asset protection in the event that your business is subject to legal action. Additionally, unlike corporations, LLCs are also simple to form, simple to maintain, and are able to avoid “double taxation.”

That being said, corporations have an easier time raising capital than an LLC and they enjoy several tax benefits that LLCs do not, such as a lack of self-employment tax.

Deciding which is better—a corporation or an LLC—depends on your business’s specific situation. Your company’s size, structure, goals, and more will determine if it is better to form a corporation or form an LLC.

To learn more about which business structure is best for you, read our guide to choosing a business structure.

While several states have laws designed to make them more attractive for corporations, the best state to incorporate in is generally the one where you are located and do the majority of your business.

Certain corporate tax benefits or other laws may look appealing, but you may end up complicating things and paying taxes and meeting compliance regulations in multiple states.

Yes, non-citizens can start a corporation in the United States. You will need a physical mailing address in the US as well as a US bank account.

For more information about opening a company in the USA, read our guide.

There are many things to consider when choosing a business name, including your brand, name availability, and the naming laws in the state you are incorporating in. You can read more details about how to name your business in our step-by-step guide.

The cost of incorporating (filing formation documents such as articles of incorporation, a certificate of formation, etc.) is between about $45 and $300, depending on your state. There may also be attorney’s fees and a registered agent fee, among others.

To learn more about the cost of setting up a corporation in your state, visit one of our state-specific corporation guides.

A registered agent accepts tax and legal documents on behalf of your business. Most states require your corporation to have a registered agent. The agent can be a professional service, yourself, or a colleague given they meet the state’s criteria.

For more information, check out our What is a Registered Agent page.

Every state requires corporations to file a formation document such as a Certificate of Formation, a Certificate of Incorporation, or the Articles of Incorporation. Some states may require additional documents, such as a state tax registration form. Check our state-specific formation guides for more details.

Professional corporations that require licensed individuals may need certain permits and licenses to operate their businesses.

Many states require corporations to file an annual report or other annual corporation paperwork, but requirements can vary. It is best to check out one of our state-by-state guides.

Owners of C Corps pay taxes on profits paid (salaries, bonuses, and dividends), then everything else is filed under the corporate tax rate. Because of this, corporations are said to be “double taxed.” They are taxed first when the company makes a profit and then taxed again when dividends are paid to shareholders.

S Corps are taxed differently, with profits passing through to the owners’ individual tax returns. For more information, check out our What is an S Corporation page.

The U.S. federal corporate tax rate is 21%. Corporations might also have to pay additional state or local corporate taxes depending on where they decide to do business.