Accounting Firm Business Insurance

Getting insurance for your accounting firm is essential.

Accounting firms need to be protected against claims involving things like professional negligence, breach of contract, or fraudulent misrepresentation.

For example, you may make an error in their financial reporting that causes damage to a client, or an employee may be found to have overstated their qualifications.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for an Accounting Firm

General liability insurance is — generally speaking — one of the most important insurance policies for accounting firms.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

While general liability insurance will protect your accounting firm from a large array of risks, it will also likely need additional coverage in conjunction with this to be fully protected. Many accounting firms tend to opt for the following coverage:

- Property insurance

- Professional liability insurance

- Home-based business insurance

- Commercial umbrella insurance

There are two main options when looking to acquire insurance for your business:

- Brick-and-mortar providers: This is the more traditionally popular option that offers trust and longevity.

- Online providers: This is a contemporary option that offers more personalized insurance at a lower cost without sacrificing quality.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

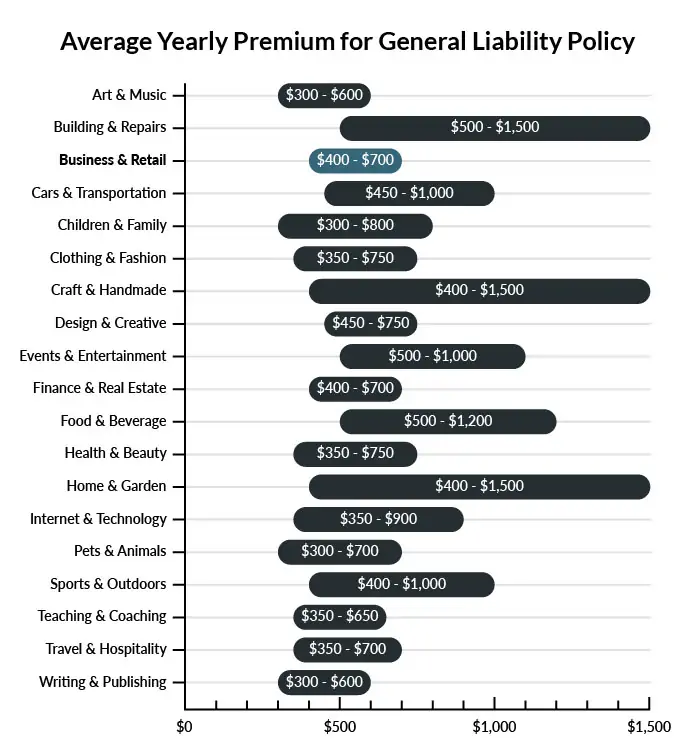

On average, accountants in America spend between $400 – $700 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for an accounting firm to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for an Accounting Firm

Example 1: A client is visiting the office to go over their tax reports and asks for a hot tea while having the meeting. Your employee accidentally spills the hot liquid on the client when delivering it, resulting in severe burns. General liability insurance will likely cover the resulting medical bills.

Example 2: One of your accountants misses an important deduction for a client, resulting in them overpaying thousands of dollars on their taxes. General liability insurance will likely help you settle any resulting claims or reputation loss.

Example 3: A client sues your business because they believe your marketing to be misleading. General liability insurance will likely help you cover the cost of defending yourself or settling out of court.

Other Types of Coverage Accounting Firms Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Professional Liability Insurance

Professional liability covers professional mistakes or negligence that may occur while on the job, Accountants give a lot of advice to their clients, and this coverage goes further than general liability insurance to help businesses when a particularly egregious error may have occurred.

Property Insurance

An accounting business typically relies on the space and the equipment they have to function. Just one storm, incident of theft, or fire can threaten its livelihood. Property insurance is likely to cover the grounds, physical building, and the business equipment in the event of damage or destruction.

Home-Based Business Insurance

For accountants working from their home, this insurance will cover any damage or destruction that occurs to the areas used for business. So if the accountant is deducting the cost of their mortgage for tax purposes, they’ll likely need home-based insurance to cover common events such as fire, theft, or flooding.

Commercial Umbrella Insurance

Commercial umbrella insurance is designed to cover expenses in the case of a particularly costly legal claim. For example, if a client feels as though you cost them millions of dollars because your financial forecasting proved too conservative. The case drags on for a year, incurring many thousands of dollars in legal costs. Commercial umbrella insurance will cover a business when the limits of its general liability or professional liability insurance policies are reached.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your accounting firm:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Accounting Firm Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

It is very important you secure the right accounting firm business insurance before launching operations in order to mitigate the inherent risks associated with the accounting industry.

It is also worth being aware that you may be legally mandated to own certain types of insurance (e.g., workers’ compensation or commercial auto) in order to be compliant with local regulations.

Not necessarily. Certain exceptions may be written directly into your accounting firm insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability – that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.