Art Supply Store Insurance

Getting insurance for your art supply store is essential.

Art supply stores need to be protected against things like product liability claims, negligence, breach of warranty, and false advertising claims.

For example, an employee may fail to ensure that hazardous materials are labeled properly, or customers may claim that your store knowingly sold defective products.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for an Art Supply Store

General liability insurance is — generally speaking — one of the most important insurance policies for art supply stores.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

On top of general liability, art supply stores tend to take advantage of several other policies to ensure maximum coverage. Some of these policies include:

- Commercial property insurance

- Workers’ compensation insurance

- Professional liability coverage

- Commercial umbrella liability insurance

Businesses looking for insurance will notice that there are generally two types of providers for them to buy from:

- Traditional brick-and-mortar insurers: Historically favored for their reliability and long-standing history, these providers typically utilize an insurance agent to be able to offer their clients very customized quotes from their stores.

- Online insurers: By taking advantage of low overheads and AI, these online-based providers offer similarly customizable quotes to their traditional counterparts — often at a cheaper price.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

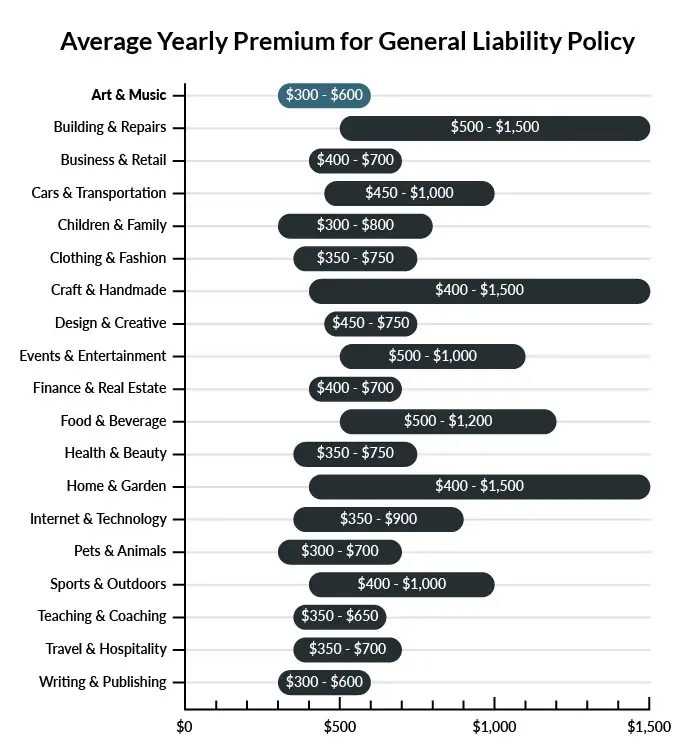

On average, art supply stores in America spend between $300 – $600 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for an art supply store to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for an Art Supply Store

Example 1: One of your staff members accidentally bumps into a customer, causing them to fall into a stack of merchandise. General liability Insurance will likely cover the cost of the customer’s injuries.

Example 2: You sell a defective set of paints to a customer and the merchandise ruins a valuable commercial project they were working on. General liability Insurance will likely cover their claims against you if the customer can prove a loss of income.

Example 3: A customer signs up for sculpture class at your store and purchases a full set of expensive supplies to help them complete the course. During the class, their tools are ruined and the customer blames faulty sculpture techniques taught in the class. General liability insurance will cover the cost of the tools or pay to fight the claim.

Other Types of Coverage Art Supply Stores Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Commercial property insurance covers not just the building you’re located in, but also the merchandise stored within it. If a covered event such as inclement weather or vandalism damages either the structure or its contents, you can use commercial property insurance to recoup your losses. Inventory can be damaged easily in an art supply store, and depending on the cost of the products, it can be expensive to replace without proper insurance coverage.

Workers’ Compensation Insurance

If you have employees working in your art supply store, workers’ compensation insurance will cover them in case they’re injured on the job. While an art supply store may not be as dangerous as many other businesses, your workers may be handling dangerous chemicals or tools throughout the day or stocking high shelves with heavy boxes.

Professional Liability Coverage

Professional liability insurance covers you in case you or your employees make a mistake on the job. For example, an employee mistakenly advises a customer that a certain product will not aggravate their skin condition, but it does. Professional liability insurance will help you fight the claim or settle the costs of the customer’s medical bills.

Commercial Umbrella Liability Insurance

This form of insurance offers extra protection in case of a particularly expensive liability claim. For example, if you decide to fight a lawsuit and the suit drags on for months, you’ll need additional coverage to cover attorney and court fees.

Commercial liability insurance can also help you restore your reputation in the face of public scrutiny. This form of insurance is highly recommended if you sell supplies to professional artists.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your art supply store:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Art Supply Store Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes, it is likely you will need insurance before starting your art supply store. Depending on your circumstances, you may even be required by law to hold certain policies, such as commercial auto.

Regardless, even where it is not a legal requirement, getting adequate business insurance for your art supply store is pivotal as it ensures your store is protected from many potential risks from the get-go.

Not necessarily. Certain exceptions may be written directly into your art supply store insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.