Bakery Business Insurance

Getting insurance for your bakery is essential.

Bakeries may be exposed to financial loss as a result of damage to their property or claims for compensation from customers and other parties who suffer injury as a result of the business.

For example, a manufacturer’s representative visiting the bakery is burnt owing to an employee’s negligence, and the representative sues. These losses can be guarded against if the appropriate insurance is in place.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Bakery Business

General liability insurance is — generally speaking — one of the most important insurance policies for bakeries.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

While general liability insurance will protect your bakery from a wide range of risks, there are insurance policies especially designed for specific dangers. Such specialized policies include:

- Commercial property coverage: Policies of this kind will offer protection if a fire results because of overheating equipment and causes damage. Coverage will also extend to property that is damaged by vandals or stock that is stolen by burglars, as well as other types of property damage.

- Commercial auto insurance: Coverage may be for the risk of damage that is caused by collision or may be more extensive with comprehensive coverage, which, in addition to collision-covered events, will protect against other risks.

- Business income coverage: This policy will compensate a business for loss of income resulting from an adverse event, such as a fire, that interrupts operations, as well as cover regular operating expenses, like rent, that must continue to be paid.

Companies providing insurance products are generally of two kinds:

- Traditional brick and mortar insurers: These are long-established providers that operate as the hub of a network of agents and brokers. Included in this bracket are insurers like Travelers Group and USAA Group.

- Online insurers: Providers, such as Ergo Next and Zipari, are insurtechs that are able to offer lower premiums. This is because they have lower operational costs. Importantly, there is no network of branches to maintain.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

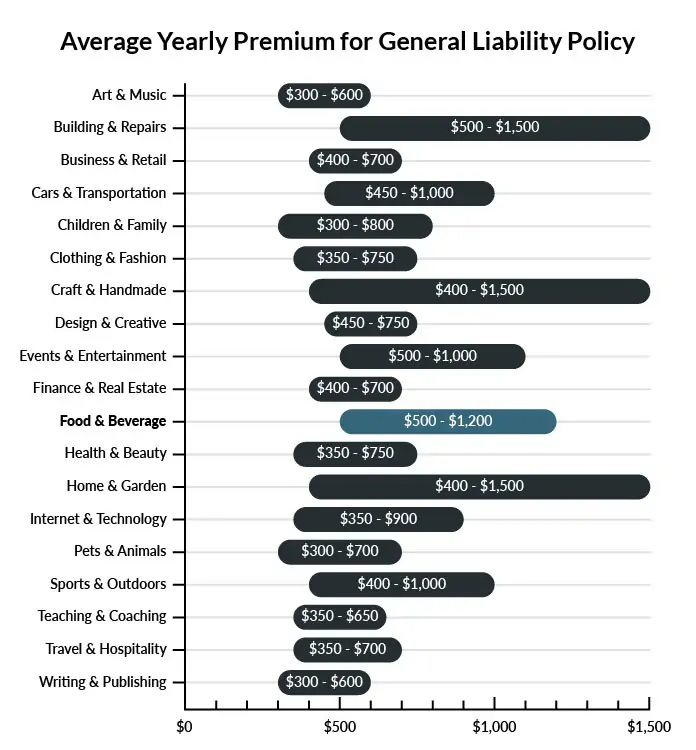

The average bakery in America spends between $500 – $1,200 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a bakery business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for a Bakery Business

Example 1: A visitor to your bakery is taking a tour when she stumbles and catches herself on a hot oven. The burns she sustains require medical care. She demands that your business pays for that medical care. You can likely get financial assistance from your general liability insurance policy to pay for her treatment.

Example 2: One of your bakers writes a blog about her experiences. In one of her recent blogs, she talks about why your bakery is better than a competitor’s bakery. The competitor sees the blog and decides to sue your business for libel. Your general liability insurance will pay for your legal defense against accusations of libel, including the cost of a settlement if one is required.

Example 3: A customer is leaving your store. She swings the door open to leave, steps into the doorway, and then stops to check her phone. The door swings back and hits her, knocking her to the ground and causing her to break her wrist. She sues your company for damages. Your general liability insurance will pay for your legal defense.

Other Types of Coverage Bakery Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

All of your ovens, other equipment, and supplies for baking took a considerable investment to acquire. If you were to lose most or all of your property in an unexpected event like a fire, it would be expensive to pay for replacements. With a commercial property insurance policy, you can get financial help to pay for repairing or replacing the property that is lost in a covered event.

Product Liability Insurance

You bake your goods with care, but there is always the possibility that someone will claim that something you sold caused them injury or illness. If you have product liability insurance, your policy will pay for your legal expenses if a customer sues you for damages caused by one of your products.

Commercial Auto Insurance

If you have a vehicle that you use primarily for business, you need a commercial auto policy to protect your vehicle, those that drive the vehicle, and your business. Your state likely requires you to have a commercial auto policy. With such a policy, you have coverage if your vehicle is involved in an accident, both for property damage and for medical care to treat injuries.

Workers’ Compensation Insurance

Your state most likely requires you to carry workers’ compensation insurance if you have employees. Your policy will pay for medical treatment for employees injured performing work-related duties. It will also help to pay their lost wages while they recover from their injuries.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your bakery business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Bakery Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Taking up insurance prior to starting business operations is crucial. Failing to have coverage from the onset may not only expose your business to peril, it could also lead to legal infringements.

Certain forms of insurance, such as commercial auto insurance and workers’ compensation, are required by law. Additionally, your business may need insurance so as to be protected against specific risks such as property damage and bodily injury to customers.

Not necessarily. Certain exceptions may be written directly into your bakery business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.