Car Detailer Business Insurance

Getting business insurance for your car detailing service is essential.

Business insurance can protect a business from financial loss, property damage, and injury to individuals.

For example, an employee may accidentally damage a customer’s vehicle while working on it. Naturally, the damage must be repaired. But there is insurance that will cover the cost of repairs.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Car Detailer Business

General liability insurance is — generally speaking — one of the most important insurance policies for car detailing businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

While general liability insurance can cover a broad range of risks, it may not provide coverage for all the potential risks faced by your business. In such cases, you may need to consider obtaining specialized policies that offer coverage for specific types of risks, such as:

- Commercial property coverage: Property insurance can provide coverage for the company’s physical assets, such as the building and equipment, in case of damage or loss due to fire, theft, vandalism, or natural disasters. This type of insurance can help car detailing companies recover from unexpected events that may damage their property and equipment.

- Commercial auto insurance: This type of insurance is designed to protect a car detailing company’s vehicles from damages and accidents while on the road. It can cover the costs of repairs, medical expenses, and legal fees resulting from an accident involving a company vehicle.

- Worker’s compensation insurance: This policy provides coverage for employee injuries or illnesses that occur on the job. For car detailing companies, this type of insurance is essential as employees may be exposed to various hazardous chemicals and machinery while detailing vehicles.

When searching for an insurance company, it’s important to keep in mind that there are two main types to choose from, traditional brick-and-mortar insurers such as Nationwide or Allstate, and online insurers such as Ergo Next or Tivly.

The advantages and disadvantages of each will depend on your specific circumstances. However, if you’re a small business owner looking for affordable and high-quality insurance, it’s generally recommended to opt for an online-based insurer.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

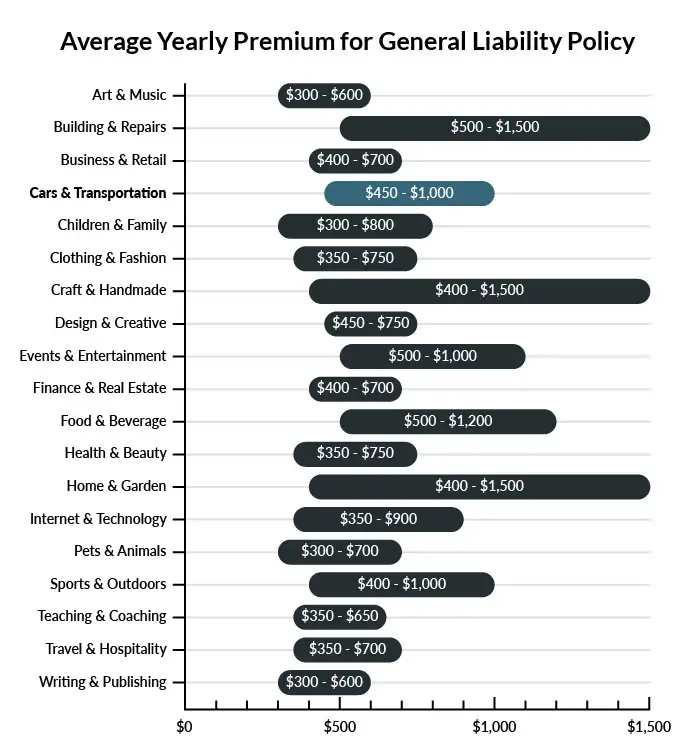

The average car detailer business in America spends between $450-$1,000 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a car detailer business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for a Car Detailer Business

Example 1: In your specialized business, your workers rely heavily on large equipment to assist in the detailing process. If a customer wanders into the garage to check on their car as it sits on the lift, they could be burned, scraped, or slip and fall on tools on the floor. In this line of work, it’s nearly impossible to prevent every possible accident from ever taking place. Luckily, general liability coverage can step in to help cover damages if you’re sued by an injured customer.

Example 2: If you’re working in a busy garage and one car rolls back into another, it could cause thousands of dollars in damages to both vehicles. While minor scrapes and dings can easily be paid for out-of-pocket, you don’t want to be stuck paying for serious damages. Large-scale property damage to a third party’s property should be covered by your comprehensive general liability policy.

Example 3: While it’s important to employ a team that takes workplace safety seriously, in the car detailing business, a wide variety of cleaning solutions and oils are used to make each car look it’s best. If a car detailing product is spilled or not cleaned properly, there is a risk for employees to slip and fall. With general liability insurance, you can rest easy knowing that most accidents, damages, and bodily injury situations are covered in case of a lawsuit.

Other Types of Coverage Car Detailer Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Garage Keepers Liability

Depending on the services you offer, it may be necessary to store customer vehicles on-site for several hours or even overnight. If a customer’s car is vandalized or stolen while on your property and you don’t have proper insurance, you could be held responsible for damages and left to repair or replace the vehicle by paying out-of-pocket.

Workers’ Compensation Coverage

Most business types must carry workers’ compensation insurance if they have any part-time or full-time employees. If an employee becomes sick or injured on the job, this type of insurance coverage works to cover their lost wages and related medical bills. Working with vehicles is a serious and potentially dangerous business, which is why it’s so important to make sure that your team is adequately covered in the event of an accident.

Commercial Auto Insurance

If your car detailer shop offers loaner vehicles to your customers or you use your own service vehicles, you are most likely required to invest in commercial auto coverage. Any vehicles that are used solely for business purposes should be covered under a commercial auto insurance policy to help protect your employees, customers, and your bottom line in the event of an accident.

Commercial Umbrella Liability

Whenever a business involves working on and around vehicles, there are a number of different risks to protect against. In fact, it is common for the expenses associated with accidents in these high-risk workplaces to exceed the limits of a primary insurance policy. With the help of commercial umbrella liability insurance, you can supplement your primary coverage for additional protection.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your car detailer business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Car Detailer Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Generally speaking, yes. Some types of insurance are required by state laws. In addition, an enterprise will be exposed to risks, such as property damage, financial loss, and personal injury, even before it starts conducting business. Consequently, it’s good practice to have business insurance from the very start.

Not necessarily. Certain exceptions may be written directly into your car detailer business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.