Insurance for a Christmas Lights Installation Business

Getting insurance for your Christmas light installation business is essential.

Christmas light installation businesses need protection against operational risks that cause loss or expose them to liability. Such risks include damage to property and financial loss, as well as third-party liability for claims of negligence.

For example, a contractor may install electrical fittings improperly as a result of which a fire occurs that causes damage to the store next door. In a situation such as that the owner is likely to take legal action. It’s best to be prepared for such eventualities by having insurance.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Christmas Lights Installation Business

General liability insurance is — generally speaking — one of the most important insurance policies for Christmas light installation businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Regardless, your Christmas lights installation business may also need protection from other risks. Three common risks that many businesses are exposed to and the policies that cover them are:

- Commercial property coverage: Provides reimbursement for the cost of replacing damaged or stolen property, which could be anything from electrical fixtures and fittings to tools and equipment.

- Commercial auto insurance: An auto insurance policy may offer just basic protection that indemnifies an owner for collision-related damage to vehicles or individuals. There are also comprehensive policies that protect against off-the-road risks.

- Business income coverage: This is coverage that reimburses you for loss of income that results from an interruption of business. If, for example, your business has to shut up shop for a while because some adverse event, such as a fire, has occurred the insurer will cover the loss of income sustained.

In today’s insurance marketplace you’ll find the following two types of insurers:

- Traditional brick and mortar insurers: This category includes the conventional firms, like State Farm and GEICO, that have dominated the market for decades.

- Online insurers: These providers, e.g. Ergo Next, have mostly entered the industry in the 21st century. They may be new to the market but they come equipped with the most advanced risk management techniques.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

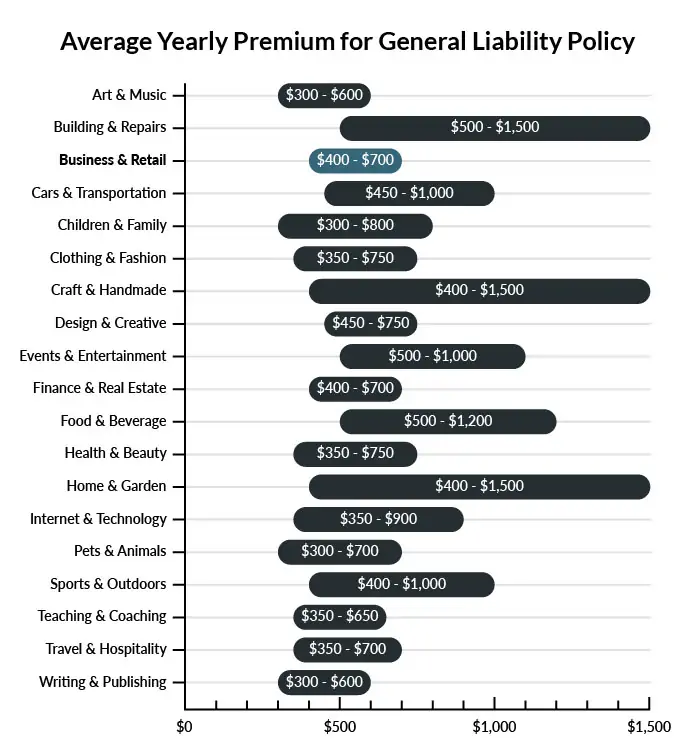

On average, Christmas lights installation businesses in America spend between $400 – $700 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a Christmas lights installation business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Christmas Lights Installation Business

Example 1: While setting up the Christmas lights in a client’s home, the technician activates the wrong wire and causes an electrical fire. General liability insurance will likely cover any property damage that may result from the accident.

Example 2: A technician accidentally leaves a bucket of tools in the middle of an outdoor walkway during the unveiling of a client’s light installation. This obstruction causes the client to trip, fall, and break their wrist. General liability insurance would likely cover the injuries and follow-up appointments.

Example 3: A local competitor believes that your logo too closely resembles their own. They sue you for copyright infringement as well as lost income. General liability will likely help cover the cost of either fighting the claim in court or settling outside of it.

Other Types of Coverage Christmas Lights Installation Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Professional Liability Insurance

Professional liability insurance is there in case you or your employees make a mistake or skip a step while on the job. No matter how skilled your technicians are, light installations will always be a hazardous line of work. This coverage is an extension of general liability insurance and provides specific coverage should your employees’ work cause major damage or physical injury to your clients.

Commercial Auto Insurance

Employees using their vehicles to get back and forth to clients’ homes will need commercial auto insurance to protect themselves, the vehicle, and other people on the road. Commercial auto insurance is likely to cover an at-fault accident, repairing any vehicles or property that may have been damaged. It will also cover the cost of treating bodily injuries.

Home-Based Insurance

Because Christmas lights are a seasonal business, many owners will operate their business from their homes. Should a work-related accident or injury occur on the premises, homeowner’s or renter’s insurance might not cover the damages.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your Christmas lights installation business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Christmas Lights Installation Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Generally speaking, yes. Acquiring business insurance prior to starting your business is crucial. Failing to have coverage from the onset may not only expose your business to unforeseen hazards, but it could also lead to legal infringements.

Certain forms of insurance, such as commercial auto insurance and workers’ compensation, are mandatory by law. Additionally, your business may necessitate insurance to safeguard against specific risks such as property damage and personal injury to customers.

Not necessarily. Certain exceptions may be written directly into your Christmas lights installation business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.