Cleaning Business Insurance

Getting insurance for your cleaning business is essential.

Cleaning businesses need to be protected against things like lawsuits surrounding employment disputes, contractual breaches, and claims of property damage.

For example, an employee accidentally damages the flooring of a customer’s house, or a commercial client claims that your employees didn’t perform the services listed in their contract.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Cleaning Business

General liability insurance is — generally speaking — one of the most important insurance policies for cleaning businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

In addition to general liability, other insurance policies that are commonly purchased by cleaning businesses include:

- Professional liability insurance

- Commercial auto insurance

- Commercial property insurance

- Workers’ compensation insurance

When purchasing coverage for your cleaning business, you will typically encounter key types of providers, each with their own unique approach to selling:

- Traditional brick-and-mortar insurers — These providers operate out of a storefront and make use of insurance agents to sell insurance to their customers. Well-known examples of this type of provider include Nationwide and Hiscox.

- Online insurers — These providers operate entirely online by taking advantage of AI to sell extremely customized and good-value insurance thanks to their lower operating costs.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

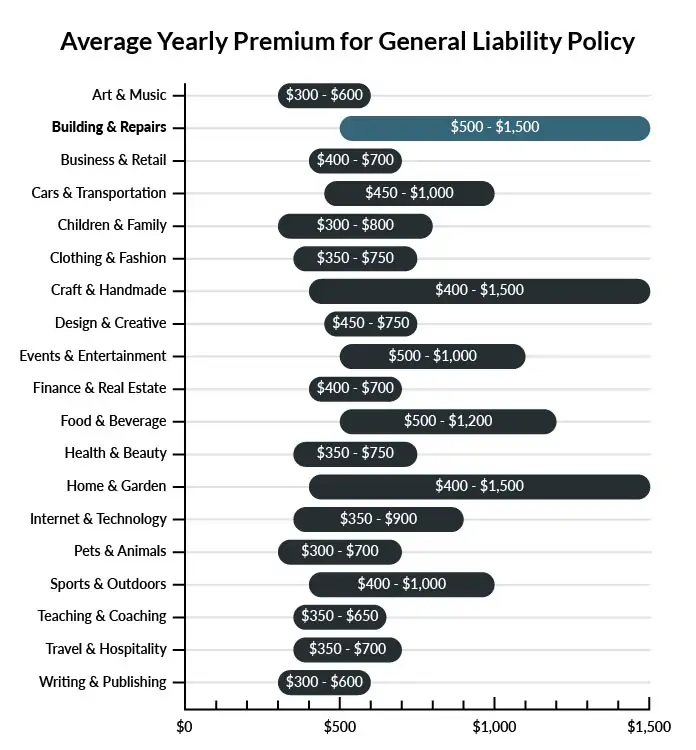

On average, cleaning companies in America spend between $500 – $1,500 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a cleaning business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for a Cleaning Business

Example 1: One of your employees is cleaning a local recording studio when he spills a cleaning agent all over a deck of some expensive electronics. The client demands that you pay for replacements. Your general liability insurance will cover this expense.

Example 2: An employee is loading the van with cleaning supplies when she accidentally knocks a client over. The client breaks her wrist and asks that you pay for her medical treatment. Your general liability insurance policy will likely cover the cost of her medical bills.

Example 3: A competing cleaning company sends you a letter telling you that they are suing you for libel. While you are not certain how you could have libeled them, you know you need an attorney. Your general liability insurance will pay for your legal expenses.

Other Types of Coverage Cleaning Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Professional Liability Insurance

Professional liability insurance will cover negligence claims due to alleged mistakes or failure to perform. It will protect your cleaning business in the event that a client sues you claiming your services or a mistake you made caused them injury. It will pay for your legal fees and the cost of a settlement if one is necessary.

Commercial Auto Insurance

When you have a vehicle that you use primarily for business, you need commercial auto insurance. This will protect your vehicle, the driver, and others on the road. If you are involved in an accident, it will pay for repair and replacement costs as well as for medical treatment for the injured.

Commercial Property Insurance

You have probably invested a significant amount of money in your cleaning equipment and supplies. If you were to lose it in an unexpected event, like a fire, it would be expensive to replace. Commercial property insurance would help cover replacement costs as long as the loss was caused by a covered event.

Workers’ Compensation Insurance

If you have employees, you need workers’ compensation insurance to protect them, and your business, in case they are injured on the job. Most states require workers’ comp insurance for employers. This policy will pay for an employee’s medical bills if they are hurt performing word duties. It will also help cover the cost of lost wages if they are unable to work while recovering from their injury.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your cleaning business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Cleaning Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

It is vital for your cleaning business to make sure it is protected from the many risks of this industry with sufficient business insurance from the offset.

In some cases, this is not a mere recommendation, as your business can be legally obligated to carry specific policies (e.g., commercial auto insurance) if it meets certain criteria.

Not necessarily. Certain exceptions may be written directly into your cleaning business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.