Clothing Boutique Business Insurance

Getting insurance for your clothing boutique is essential.

Clothing boutiques need to be protected against things like claims of intellectual property infringement, product liability, and breaches of contract.

For example, one of your clothing boutique’s designs is too similar to that of a patented design, or a customer claims that your latest sales campaign was false advertising.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Clothing Boutique Business

General liability insurance is — generally speaking — one of the most important insurance policies for clothing boutiques.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Your clothing boutique may find it beneficial to purchase some of the following policies in addition to general liability to protect against some of the more specific risks it faces:

- Crime insurance

- Property insurance

- Workers’ compensation insurance

- Business interruption insurance

- Commercial umbrella insurance

As a business owner, it is important that you are aware of the differences between the two distinct groups that insurance providers are commonly divided into:

- Traditional brick-and-mortar insurers — Refers to providers such as Hiscox and The Hartford, which often have a long-standing history and operate from a physical storefront.

- Online insurers — Refers to providers such as Tivly and Ergo Next, which have been founded more recently and operate almost completely online. They are the favored option by many businesses because their digital nature allows them to conveniently and affordably offer their customers highly tailored assistance.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

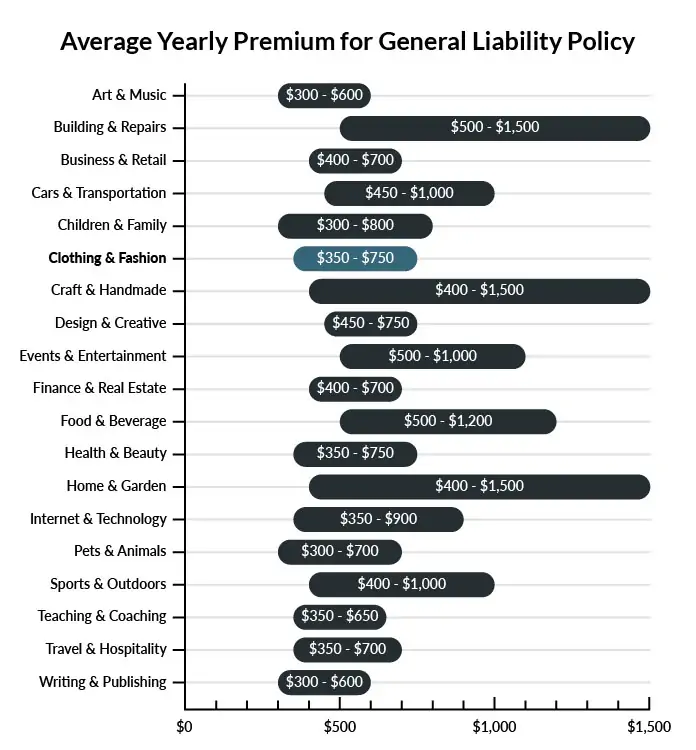

The average clothing boutiques in America spends between $350-$750 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a clothing boutique business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for a Clothing Boutique Business

Example 1: One of your customers leaves a pair of slacks with you to be altered. During the alteration process, the clothing is damaged beyond repair. Should the customer opt to sue you, your General Liability policy would kick in and pay for costs associated with this claim.

Example 2: A customer is interested in trying on a sweater that is displayed on the top shelf. A boutique employee asks the guest to wait for assistance and walks away to grab a small ladder. Instead of waiting, the customer reaches for the sweater, causing a nearby display to fall on their head. Your policy will recover costs related to the ensuing lawsuit.

Example 3: Heavy rain occurs during a busy Saturday shift, causing customers to track in water and mud. To reduce potential exposure, you place a welcome mat by the front door for guests to wipe their feet. As a customer is rushing to get out of the rain, she slips and falls, breaking her wrist trying to catch her fall. Even though you took all necessary precautions to avoid such an incident, the disgruntled customer sues your business. Your policy will cover charges associated with the lawsuit.

Other Types of Coverage Clothing Boutique Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Crime Insurance

This coverage offers another layer of protection for your inventory and cash register contents. If an employee steals out of the cash drawer, or a customer shoplifts several pieces of jewelry, Crime Insurance will help reduce the effects of these losses.

Property Insurance

If you own your location instead of renting, you need property insurance to protect the building. If your business is based out of your home, your homeowners’ insurance will not cover the home when it is being used for commercial purposes. Property insurance also covers items owned by your business.

This coverage is generally offered in a Business Owners’ Policy (BOP)

Workers’ Compensation Insurance

If your clothing boutiques has any employees (full-time or part-time), you are legally required to carry workers’ compensation insurance. This type of coverage will help compensate your employees in the case that they get injured on the job.

Business Interruption Insurance

In the event of a fire, flood, or other catastrophes, there is a good chance your business operations will be halted for some time. Business interruption coverage is designed to help you recoup a portion of the revenue your business would lose due to the inability to operate.

This type of insurance is typically included in a business owner’s policy.

Commercial Umbrella Insurance

Umbrella coverage allows you to extend above and beyond the standard limits of your other business insurance policies. If you are faced with a large lawsuit or other claim situation, there’s a possibility that the coverage limits of your standard policies will be insufficient. In this case, your umbrella policy will allow you to surpass these limits.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your clothing boutique business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Clothing Boutique Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes, safeguarding your clothing boutique with insurance from the start against the numerous risks associated with the industry is pivotal to its long-term success.

On top of providing protection to your business from the many risks it is likely to face, it may help it remain legally compliant in situations where you are obligated to carry specific insurance policies (e.g., workers’ compensation and commercial auto).

Not necessarily. Certain exceptions may be written directly into your clothing boutique business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.