Comic Book Store Insurance

Getting insurance for your comic book store is essential.

Comic book stores need to be protected against things like claims arising from personal injury on the premises, copyright infringement, and disputes surrounding employment.

For example, your store sells unlicensed merchandise to its customers, or a customer claims that you misrepresented the legitimacy of a collectible comic book.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Comic Book Store

General liability insurance is — generally speaking — one of the most important insurance policies for comic book stores.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

While general liability is essential to all comic book stores, it is unable to provide fully comprehensive protection by itself. Therefore, many stores decide to purchase some of the following policies in addition to it:

- Commercial property insurance

- Crime insurance

- Workers’ compensation insurance

- Business interruption insurance

When you are looking at where to purchase insurance for your business, there are generally two main routes available to you:

- Traditional brick-and-mortar insurers: This reputable and well-established group of insurers (which includes the likes of Nationwide and The Hartford) use an approach that focuses on their brick-and-mortar locations and insurance agents.

- Online insurers: By contrast, this group of insurers (which includes the likes of Ergo Next and Tivly) have gained recognition for their primarily digitally-focussed approach that utilizes AI instead of insurance agents. Their inherently lower overheads also enable them to offer high-quality coverage for a much lower price.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

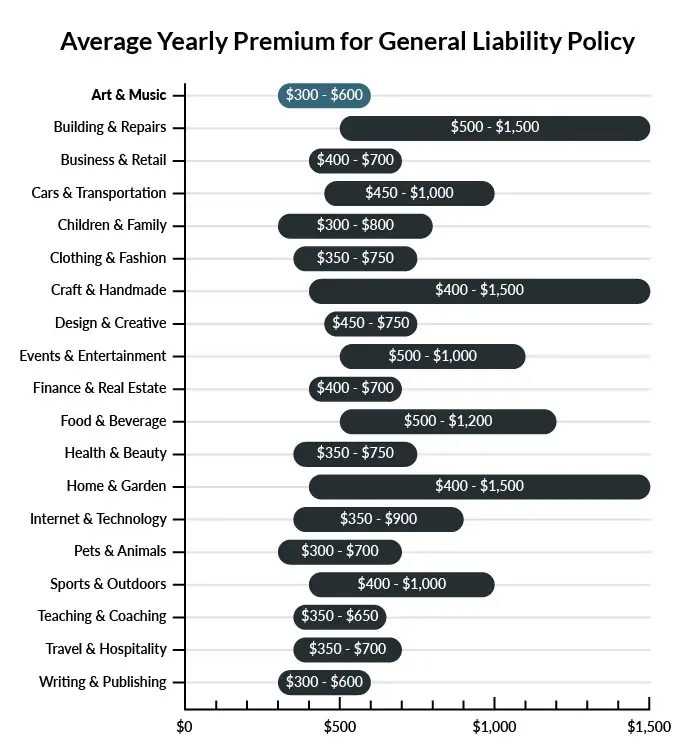

The average comic book shop in America spends between $300-$600 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a comic book store to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for a Comic Book Store

Example 1: An employee is covering the evening shift alone. He decides to extract a vintage golden-age Superman comic, worth several thousand dollars, from its protective casing and plastic cover. As he is reading it, a car alarm goes off and startles him, causing him to spill his coffee on the delicate collectible. The value of the comic drops, and it can only be sold for less than half its previous price. General liability insurance could probably compensate your business with an estimate of the comic’s previous worth.

Example 2: During a Magic: The Gathering tournament, your comic book shop hosts nearly two dozen players who occupy a large section of your store. One of the players, who has been drinking alcohol, becomes physically aggressive with his opponent. He strikes his opponent in the face, dislocating his jaw and knocking out a tooth. The injured customer sues your business. General liability insurance could probably help cover court-ordered payments to the injured party or any settlement reached.

Example 3: A car thief hotwires someone else’s vehicle in your parking lot, driving the stolen car erratically across the pavement and into the window of your store. Your front door and window display of board games are smashed, adding up to more than a thousand dollars of damages. These damages would likely be covered in part by general liability insurance.

Other Types of Coverage Comic Book Stores Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Comic book shops contain expensive inventory, from rare comics to high-quality modern board games. Commercial property insurance can help your business avoid losing costly merchandise or even shutting down, due to events like fire and violent weather. This policy also applies to owned real estate, making it especially crucial for comic book businesses that own their storefronts. All it takes is one disaster to put a store out of business, and commercial property insurance can be the difference between ruined entrepreneurship and a thriving company.

Crime Insurance

Employee theft of high-value goods, like expensive vintage comic books worth thousands of dollars, can amount to serious losses for your business. While you may trust your employees, the complex reasons behind significant theft are not always predictable. If you entrust your storefront to an employee, it would be wise to purchase a policy like this one, which will cover losses due to employee dishonesty, property theft, forgeries, and more.

Workers’ Compensation Insurance

You may decide to staff your business with part-time or full-time employees, which will legally require workers’ compensation insurance. With this policy, your valuable workers are covered in the event that they suffer serious accidental injuries in the workplace. Providing disability and death benefits for your employees and their families, this insurance is an essential inclusion for any business owner who elects to hire help.

Business Interruption Insurance

Interruptions to business are often unexpected, leading to a disorganized scramble as company personnel strives to reestablish the business’s footing. This is a long, expensive process during which every passing day represents stagnant profits at best and a tremendous expense at worst.

Business interruption insurance serves to cover estimated losses during a temporary business closure resulting from a fire, tornadoes, or other similar disasters. The policy can sometimes cover temporary relocations during the rebuilding efforts, keeping companies afloat during challenging transitions.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your comic book store:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Comic Book Store Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

If you want to ensure the longevity of your comic book store, it is crucial that you obtain the necessary business insurance beforehand. This should shield your store from any financial loss it could be exposed to as a consequence of the inherent risks of this industry.

In many cases, certain insurance policies (such as workers’ compensation or commercial auto) may be mandatory for your store to operate in line with your state’s regulations.

Not necessarily. Certain exceptions may be written directly into your comic book store insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.