Convenience Store Insurance

Getting insurance for your convenience store is essential.

Convenience stores need to be protected against things like claims arising from slips and falls, product liability, and assault or robbery.

For example, a customer suffers food poisoning after consuming one of your products, or they slip and fall while entering your store.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Convenience Store

General liability insurance is — generally speaking — one of the most important insurance policies for convenience stores.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

It is very common for convenience stores to adopt several insurance policies alongside general liability to ensure they are properly protected. Some of these policies could include:

- Commercial property insurance

- Workers’ compensation insurance

- Product liability insurance

- Business interruption insurance

- Crime insurance

There are typically two general routes available to your business when it comes to the type of insurance provider you can purchase your coverage from. These options are:

- Traditional brick-and-mortar insurers — This group includes providers like Nationwide, The Hartford, and Hiscox.

- Online insurers — This group includes providers like Tivly and Ergo Next.

We suggest businesses opt for online insurers in favor of traditional ones because they offer the perfect balance of high-quality insurance for an affordable price.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

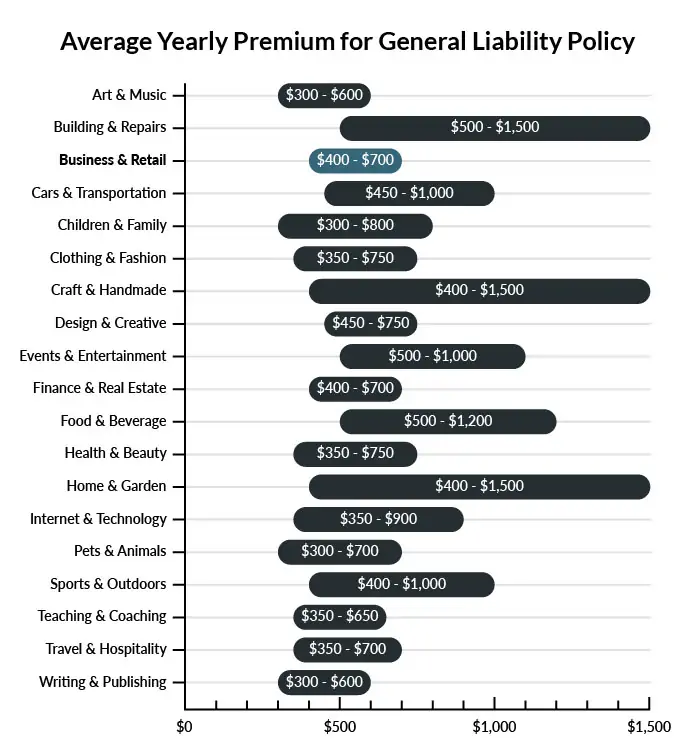

The average convenience store in America spends between $400-$700 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a convenience store to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your.

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for a Convenience Store

Example 1: A customer walks in shortly after the store’s floor has been mopped, and they slip and fall hard on the floor. General liability insurance would probably cover legal costs and injuries resulting from the fall.

Example 2: When making deliveries, a supplier knocks over a full supply shelf and injures their leg General liability insurance would probably cover the vendor’s injuries.

Example 3: An advertised special is canceled, and a customer files a false advertising lawsuit because they couldn’t get the deal. General liability insurance would likely help pay associated legal costs.

Other Types of Coverage Convenience Stores Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Convenience stores should have commercial property insurance for the physical property they own. This may include a parking lot, a building, coolers, equipment, and inventory.

Commercial property insurance can be purchased through business owners policies (BOPs).

Workers’ Compensation Insurance

Assuming your convenience store has employees, the store needs workers’ compensation insurance. This insurance covers work-related illnesses and injuries, and it’s generally required by state law if your business employs workers.

Product Liability Insurance

Businesses can sometimes be held responsible for damage or injuries that the products they sell cause. Product liability insurance protects against risks that come with selling products.

When selecting product liability insurance, make sure it covers the full range of products that your convenience store sells. Coverage for packaged foods and beverages, prepared foods and beverages, alcohol, tobacco, and non-food items should all be included if your store carries those products.

Product liability insurance can be purchased by itself or through a package policy.

Business Interruption Insurance

Recovering from a disaster can take time, and bills often still need to be paid. Business interruption insurance may provide supplemental revenue during a post-disaster recovery period so that your convenience store can continue to pay its due bills.

Business interruption insurance can be purchased through BOPs.

Crime Insurance

Commercial property insurance usually protects against burglaries, but it often excludes theft by employees. Crime insurance provides coverage for employee theft and similar perils.

Crime insurance can be purchased by itself or through a package policy.

Liquor Liability Insurance

If your convenience store sells alcohol, it might need liquor liability insurance. This coverage shields businesses from liability suits associated with alcohol-related incidents that their customers are involved in. Whether your store is required to carry it depends on what type of alcohol is sold and the laws in your state.

Liquor liability insurance can be purchased by itself or through a package policy.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your convenience store:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Convenience Store Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

For your convenience store, acquiring business insurance is one of the most important tasks to be completed before it opens. Neglecting the protection of this coverage can negatively affect the long-term growth of your business as it will be vulnerable to all risks it may face.

Additionally, certain forms of insurance may be essential for your business to continue to operate legally — especially if your store has employees or designated vehicles.

Not necessarily. Certain exceptions may be written directly into your convenience store insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.