Debt Collection Agency Business Insurance

Getting insurance for your debt collection agency is essential.

Obtaining insurance is crucial to ensure the safety of your debt collection agency as it is exposed to the various risks that are common to that kind of business. With insurance, these businesses can be protected against property damage and also receive liability coverage for bodily injury or financial loss.

For example, a debtor complains that one of your assistants acted in a way that caused them to fear they would use violence. If that situation develops into a lawsuit, having insurance to pay legal fees and/ or compensation would be important.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Debt Collection Agency

General liability insurance is — generally speaking — one of the most important insurance policies for debt collection agencies.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

However, your debt collection company may face other hazards that are not covered by a general liability policy. Here are three types of insurance to guard against those adverse occurrences:

- Commercial property coverage: This type of insurance will compensate your business for expenses incurred in repairing damage to the premises that house the debt collection agency. Damage covered typically includes that caused by fire, vandalism, burglary and theft.

- Commercial auto insurance: An auto insurance policy may offer just basic protection that indemnifies for collision-related damage to vehicles or individuals. But it’s possible to get a comprehensive policy, which will protect against off-the-road risks.

- Business income coverage: This policy will indemnify a business for loss of income resulting from an adverse event that interrupts operations, such as damage to the premises caused by a falling tree. The policy will also cover regular operating expenses, like salaries, that must continue to be paid.

Despite the plethora of firms in the industry, there are basically just two types of insurers:

- Traditional brick and mortar insurers: Traditional insurers tend to be risk-averse and less likely to embrace change. Their conservative approach means they prefer to stick to tried and tested methods that have worked in the past. This can lead to higher premiums.

- Online insurers: Insurtechs are often more innovative than traditional insurers. They are more likely to experiment with new technologies and business models, which can lead to new products and services that benefit customers. Reduced overhead and innovative technologies promote lower premiums and better policy coverages.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

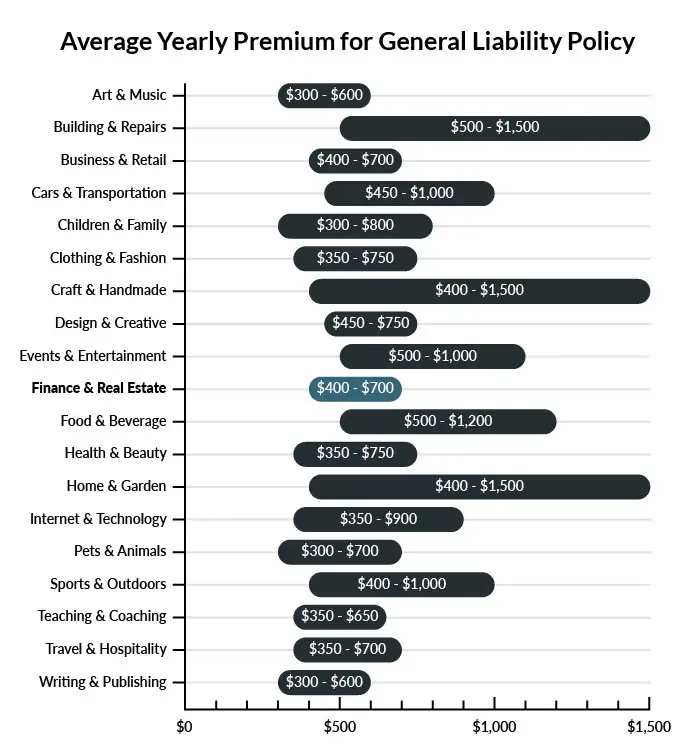

On average, debt collection agencies in America spend between $400 – $700 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a debt collection agency to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for a Debt Collection Agency

Example 1: A debtor accuses you of harassment based on your debt collection practices. General liability insurance would cover your legal costs to fight or settle the harassment charge.

Example 2: While visiting your agency, a potential client trips on a purse left in the hallway by one of your employees. General liability insurance would cover the potential client’s medical bills.

Example 3: Your agency accidentally identifies the wrong person as a debtor, and they sue your company for slander against their character. General liability insurance would cover your legal defense costs.

Other Types of Coverage Debt Collection Agencies Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

If you own the building in which you operate, commercial property insurance helps protect your business-related property from a variety of events, such as theft, vandalism, and extreme weather. It covers the cost of repairing the physical structure as well as repairing or replacing any equipment you store there.

Workers’ Compensation Insurance

Most states require businesses to carry workers’ compensation insurance for their part-time and full-time employees. This coverage protects your employees if they become injured at work or fall ill after a work-related accident. It not only covers an employee’s medical bills and lost wages if they need time to recover but also any disability or death benefits stemming from a work-related accident.

Professional Liability Insurance

If your business offers debt consulting services as well as collection services, this insurance covers any faulty or negligent advice you may provide. If a client accuses your company of revenue loss based on your consulting services, for example, professional liability insurance would pay your legal fees if that client decides to sue.

Data Breach Insurance

Because your business collects and stores information about your clients and individual debtors, there’s always a chance you could suffer a cyber attack. Data breach insurance covers damages if a hacker steals information about your agency, clients, and target debtors.

Commercial Umbrella Insurance

While your general liability insurance policy covers most claims, some accidents or lawsuits may be so catastrophic that they threaten to exhaust the limits of your primary coverage. Commercial umbrella insurance protects you from paying out-of-pocket for any legal fees and awarded damages that exceed your primary policy.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your debt collection agency:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Debt Collection Agency Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

It is crucial to purchase business insurance prior to opening your shop. Failing to obtain coverage from the very beginning can pose a significant threat to your business, not just from unforeseen dangers, but also from potential legal violations.

Certain types of insurance, such as workers’ compensation and commercial auto insurance, are mandatory by law. In addition, your business may need insurance coverage to guard against specific risks, such as property damage and customer injuries.

Not necessarily. Certain exceptions may be written directly into your debt collection agency insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.