Delivery Service Insurance

Getting insurance for your delivery service is essential.

It is vitally necessary that delivery services be protected from the many perils that come with doing business. That’s why they need insurance. Insurance can shield your business from damage to property, as well as cover the business for liability arising from bodily injury or pecuniary loss.

For example, a customer alleges a large number of his packages have been misplaced and sues. Thankfully, there is insurance to cover such an eventuality: the policy will pay both for legal fees and to compensate the customer.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Delivery Service

General liability insurance is — generally speaking — one of the most important insurance policies for delivery services.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

While general liability insurance can cover a broad range of risks, it may not provide coverage for all the potential risks faced by your business. If such is the case, you may need to consider obtaining specialized policies that offer coverage for specific types of risks, such as:

- Commercial property coverage: A policy of this type could cover damage to any property you own, such as office equipment and furniture, as well as the business premises.

- Commercial auto insurance: Coverage may include the risk of damage through collision or comprehensive coverage that protects against both collision and non-collision risks, such as vandals damaging your vehicle.

- Business income coverage: This is coverage that reimburses you for loss of income that results from an interruption of business. If, for example, your business has to shut up shop for a while because some adverse event, such as a fire, has occurred the insurer will cover the loss of income sustained.

When it’s time to take out business insurance, you will generally be able to choose between the following two types of insurers, who vary in their approach to underwriting:

- Traditional brick and mortar insurers: Traditional insurers use a lot of manual processes when it comes to underwriting policies. This, combined with relying on agents and brick and mortar locations, can drive up premium prices.

- Online insurers: Insurtechs, like Policy Genius and Ergo Next, use artificial intelligence and machine learning algorithms to underwrite policies more efficiently and accurately. This can lead to better matched policies and lower premiums.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

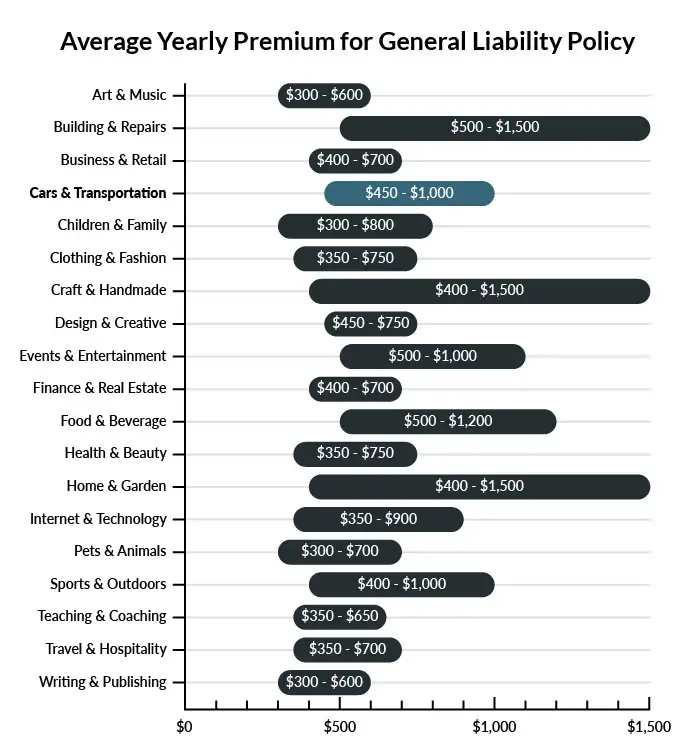

The average delivery business in America spends between $450-$1,500 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a delivery service to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for a Delivery Service

Example 1: A potential client pays a visit to your office to talk to you about a potential contract for deliveries. He goes to use the restroom but fails to notice a change in the level of the floor and trips and falls. He sustains a broken wrist. Your general liability insurance policy would likely cover the cost of treating his injuries.

Example 2: One of your delivery drivers is in a rush to meet a deadline. He is moving so quickly through your warehouse that he fails to see a visitor and runs into her, knocking her backward to the ground. She requires an ambulance and sues your business for her injuries. The general liability insurance policy you carry will pay for the costs of your legal defense, including the cost of a settlement if you wind up settling the case out of court.

Example 3: A forklift driver in your warehouse is hurrying to move a pallet of goods slated for delivery when he loses control of the forklift and drops the pallet to the ground. The entire order of expensive computer hardware is smashed. Your general liability insurance policy will likely pay for the cost of replacing your customer’s property.

Other Types of Coverage Delivery Services Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Workers’ Compensation Insurance

As an employer, your state likely mandates that you carry workers’ compensation insurance. Your policy will pay for the medical care required to treat work-related injuries sustained by your employees. It will also pay for some of the wages they lose out on when they are unable to work due to work-related injuries.

Commercial Auto Insurance

Your delivery vehicles should be covered by a commercial auto insurance policy. Much like a personal auto insurance policy, the commercial insurance policy you carry will pay for the repair or replacement of a work vehicle involved in an accident caused by you or your employees. The policy will also pay for medical treatment for injuries sustained in the accident and for any damages you or your employees are liable for due to the accident.

Commercial Umbrella Insurance

In the event that your company is required to pay extensive damages—like if you lose a big lawsuit—the limits of your general liability insurance policy may be exceeded. A commercial umbrella insurance policy is designed to pick up where your general liability insurance leaves off so you don’t have to pay the costs out of pocket.

Data Breach Insurance

Data breach insurance, also called cyber attack insurance, is designed to protect your business if you are the victim of a cyberattack. For instance, if your customer information is compromised by a cybercriminal and one or more of your customers takes legal action against your business due to the security breach, your data breach insurance would pay for your legal costs—including the cost of paying settlements, if necessary.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your delivery service:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Delivery Service Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes, and there are good reasons why you need business insurance. Your fledgling business will be exposed to risk even before its doors are open to the public. Installing fittings and fixtures, ordering office furniture and equipment, purchasing or leasing vehicles: these are all activities that involve some degree of risk.

In addition, state laws mandate the purchase of commercial auto insurance to cover company vehicles, and workers’ compensation insurance to cover employees.

Not necessarily. Certain exceptions may be written directly into your delivery service insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.