Laundry and Dry Cleaning Business Insurance

Getting insurance for your laundry and dry cleaning business is essential.

Laundry and dry cleaning businesses need to be protected against things like property damage, negligence, and contractual breaches.

For example, an employee may accidentally damage a customer’s clothing during the cleaning process, or a fire could break out at your store and cause property damage.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Laundry and Dry Cleaning Business

General liability insurance is — generally speaking — one of the most important insurance policies for laundry and dry cleaning businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

By itself, general liability will normally be insufficient for laundry and dry cleaning businesses. For this reason, many decide to purchase a couple of additional policies, including:

- Commercial property insurance

- Professional liability insurance

- Business interruption insurance

The first step involved in purchasing coverage for your laundry and dry cleaning business is identifying which type of insurer best suits your situation:

- Traditional brick-and-mortar insurers — This option, which includes some of the most reputable firms in the US (e.g., Hiscox, The Hartford, and Nationwide), is known for providing reliable and accurate insurance, albeit at a higher price.

- Online insurers — Alternatively, this option, which includes more contemporary firms like Tivly and Ergo Next, is known for its modern, online-based approach to providing insurance. Using powerful AI allows them to offer high-quality insurance at a competitive price thanks to their comparatively low overheads.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

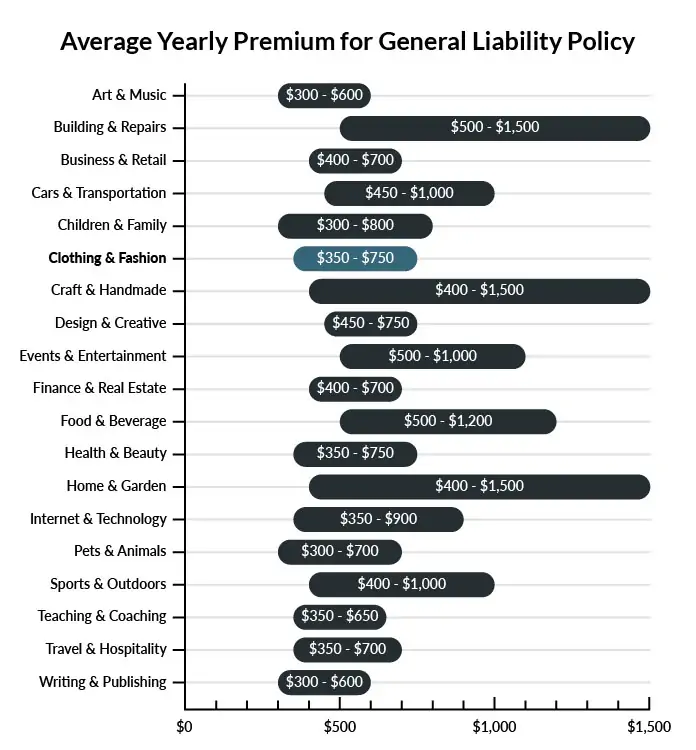

The average dry cleaning business in America spends between $350-$750 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a laundry and dry cleaning business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Laundry and Dry Cleaning Business

Example 1: Some children are playing inside your building, and one of them climbs into a washing machine, which ends up activating with the child inside. In the event your business is found liable for injuries to the child, general liability insurance would likely help to cover whatever you owed or any settlement reached regarding the accident.

Example 2: A malfunctioning washing machine leaks water onto the floor, leaving an untended pool in the middle of the front walkway. A customer slips on the water and sustains a serious injury. If liable, your company would probably be covered through general liability insurance for damages owed or settlements reached.

Example 3: A customer’s expensive collection of professional outfits is badly damaged by a malfunctioning dryer, costing her thousands in replacement expenses as well as compromising her appearance in an upcoming business event that afternoon. If liable for damages, general liability insurance could probably assist in covering anything you owed per a court’s ruling or a settlement between your business and the plaintiff.

Other Types of Coverage Laundry and Dry Cleaning Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Unquestionably, dry cleaning businesses require coverage for their expensive and hard-to-replace/repair commercial property. Dry cleaning businesses are stocked with machinery for the efficient cleaning and drying of clothing, and disasters like fire or violent weather could compromise a business’s assets, leaving it with massive replacement or repair costs. Protect your equipment and any owned real estate with a commercial property policy. When covered disasters strike, a policy like this can be the difference between bankruptcy and a challenging hurdle.

Professional Liability Insurance

Professional liability policies are suited for businesses that perform careful, professional services with potentially significant consequences. When all goes well, customers are grateful and satisfied. But if your services are provided without the proper care, or an employee suffers a lapse in professional judgment, some serious issues can arise. If your process renders a customer’s garments unusable through poor professional decision making, this policy will help to cover expensive damages and prevent your business from going into the financial red zone.

Business Interruption Insurance

What can a business do against catastrophes like fires and tornadoes? Forces of nature come and go as they please, wrecking the products and leveling businesses in a fraction of the time it took to build them. Fortunately, there is business interruption insurance to assist companies in recouping estimated profit losses during times of hardship.

When disaster puts a halt to your business operations, this policy may even cover the costs involved in temporarily relocating or training new employees to use complex machinery. Together with a commercial property policy, this insurance can keep a business afloat during hard times.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your laundry and dry cleaning business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Laundry and Dry Cleaning Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes, it is vital for each and every laundry and dry cleaning business to obtain the necessary business insurance to be safe from the risks they are faced with every day.

It is especially important when you consider that certain insurance policies may be a legal requirement, and neglecting them may lead to your business being at odds with the law.

Not necessarily. Certain exceptions may be written directly into your laundry and dry cleaning business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.