Farmers Market Business Insurance

Getting insurance for your farmers market is essential.

Farmers markets must be protected against things like claims of product liability, premises liability, and licensing violations.

For example, your farmers market doesn’t acquire the permits and licenses needed to be able to set up, or a vendor claims that you violated their contract by not providing them adequate space.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Farmers Market

General liability insurance is — generally speaking — one of the most important insurance policies for farmers markets.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

There are an array of extra insurance policies for your farmers market to consider in addition to general liability, such as:

- Commercial auto insurance for any vehicles for your market

- Workers’ compensation insurance if your market hires any staff

- Commercial umbrella insurance

- Product liability insurance if anything sold by your market is found to be faulty or otherwise not fit for sale

It is essential that you are able to recognize the two distinct types of insurance providers when attempting to identify the best fit for you. These two types are:

- Traditional brick-and-mortar insurers

- Online insurers

While each of these has its own pros and cons, online insurers like Ergo Next and Tivly are often regarded as better for small businesses as they grant them an affordable option for high-quality, personalized insurance.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

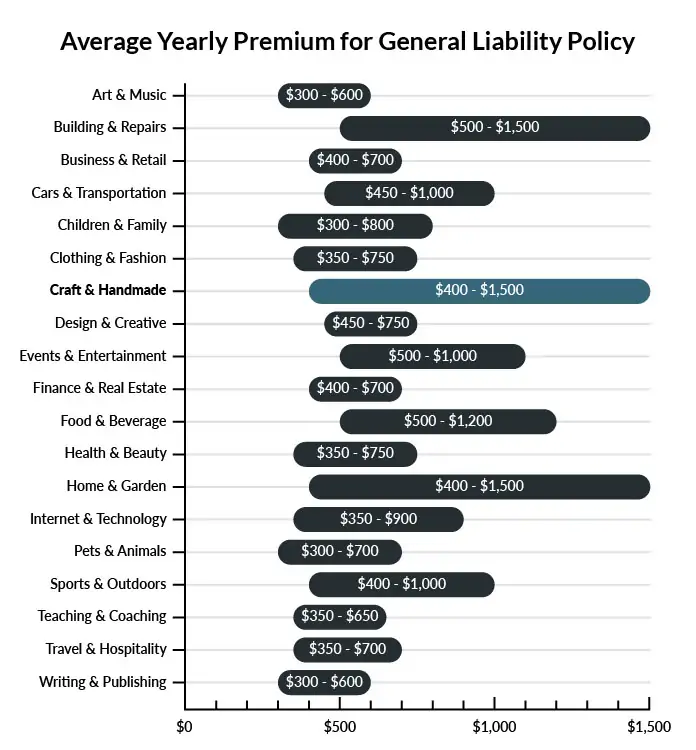

Cost of General Liability Insurance

On average, farmers markets in America spend between $400 – $1500 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a farmers market to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our cheapest business insurance review.

Common Situations That General Liability Insurance May Cover for a Farmers Market

Example 1: You leave your supplies on the ground as you take down your tent at the end of the day. As you run with a load of items to your car, a visitor trips over a tent pole and seriously hurts herself. She demands that you pay for her medical expenses or she will sue. A general liability insurance policy would likely cover her medical bills,

Example 2: An employee is hauling large boxes of apples from their car to set up for the day. As he makes his final trip, he loses control of the pushcart, and it crashes into a crowd of visitors. The accident leaves several visitors with serious injuries. If they file a claim against your business, your general liability policy will likely cover your legal fees and any subsequent award settlements.

Example 3: After running a new advertising campaign on your local access station, you receive a call from a competitor accusing you of libel, and they threaten to sue you for damages. General liability insurance will help to pay your legal fees and cover any payouts if you settle out of court.

Other Types of Coverage Farmers Markets Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Auto Insurance

Transferring goods back and forth each week is a big part of your job. And to do so, you will probably rely on a number of different vehicles to get the job done. Any vehicles that are used for business purposes should be covered under a commercial auto insurance policy to financially protect your business and your employees in the event of an accident.

Workers’ Compensation Insurance

Workers’ compensation insurance is designed to help cover medical bills and disability benefits if an employee is injured or falls ill in a work-related accident. Most states require any business with part-time or full-time employees to carry this coverage.

Commercial Umbrella Insurance

There is always a chance that an accident or lawsuit can exhaust your primary insurance limits. If this happens, you could end up having to pay for the remaining damages out-of-pocket. To avoid this issue, commercial umbrella insurance works to go above and beyond your primary coverage and helps to keep your farmers market open for business.

Product Liability Insurance

Whenever you create or sell your products, keep in mind that there is a possibility that one of them could harm to a customer. For example, a customer could claim that your product made them sick and sue you for damages. With product liability insurance, you can rest easy knowing that you have an extra layer of financial protection.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your farmers market:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Farmers Market Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes. Finding business insurance for your farmers market is an essential task to be completed before it opens to the public.

Not only because it is likely to be legally obligated to purchase certain policies (e.g., workers’ compensation insurance) but because it protects your market’s financial security.

Not necessarily. Certain exceptions may be written directly into your farmers market insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.