Film Production Business Insurance

Getting insurance for your film production business is essential.

Film production businesses face numerous risks in their daily operations, which necessitate safeguarding against potential hazards. To address these risks, insurance is a crucial requirement.

By providing coverage for property damage, bodily injury liability, and financial loss, insurance can offer a protective shield to film production companies.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Film Production Business

General liability insurance is — generally speaking — one of the most important insurance policies for film production businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Here are three common risks that many businesses are exposed to and the policies that cover them are:

- General Liability Insurance: This type of insurance provides coverage for third-party bodily injury, as well as property damage. For example, if a passerby trips on a cable and gets injured or if a camera falls and damages someone’s property, this insurance can cover the costs of legal defense and any damages awarded.

- Errors and Omissions Insurance: A policy of this kind provides coverage for legal claims related to defamation, copyright infringement, invasion of privacy, and other claims related to intellectual property. It protects the production company against lawsuits related to the content of the film, including allegations that the film infringes on the rights of others.

- Equipment Insurance: This type of insurance provides coverage for loss or damage to production equipment, such as cameras, lighting, and sound equipment. It can cover a range of incidents, including theft, damage during transport, and accidental damage on set.

Acquiring business insurance will generally mean you must choose between the following two types of insurers:

- Traditional brick and mortar insurers: Insurers in this bracket may still be using the tried and tested methods of yesteryear. In general, this means they don’t deliver their products and services as fast as many customers today would like. They generally have higher premiums compared to online insurers.

- Online insurers: In contrast, insurtechs like Acrisure and Ergo Next can often provide quotes and coverage much more quickly than traditional insurers. This is because they use technology to automate many of the processes that were done manually in the past. This, combined with reduced overhead in general, allows online insurers to offer lower premiums.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

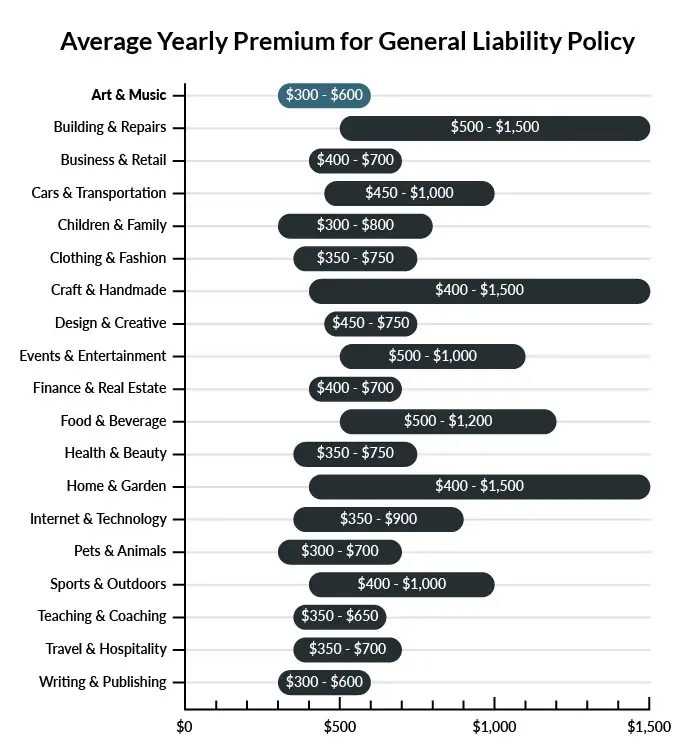

The average film production company in America spends between $300-$600 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a film production business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Film Production Business

Example 1: Some heavy equipment crashes on the set and lands on a passerby who wandered away from his studio tour. His leg is crushed, and he is rushed to a hospital. If liable for the incident, your company would probably have coverage through general liability insurance for the resulting damages or for a settlement reached.

Example 2: During a dangerous scene featuring a contained fire outbreak, the flames get out of control and end up destroying a small local bookstore. In this case, your business would likely receive coverage for the bookstore’s sustained damages through a general liability policy.

Example 3: Your caterers provide food for the wrap-up party after filming completes. Some actors and studio workers bring their friends and family, but many of them get sick after eating the food. The caterers made a major mistake and provided spoiled food to the party. If held liable for this incident in court, general liability insurance would probably cover some amount of the resulting damages as well as any settlements reached.

Other Types of Coverage Film Production Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

To a film production company, equipment is everything. Your cameras, set pieces, computers, costumes, cosmetic supplies, and more are vital material assets. If these assets are compromised by a force of nature like fire or violent weather, it can spell disaster for an uninsured film production company. Don’t get caught off guard by sudden catastrophes. Commercial property insurance helps to cover losses sustained to owned commercial real estate, equipment, and other supplies that support your business. This policy is non-negotiable for truly serious businesses.

Commercial Auto Insurance

A film production company will require some number of motor vehicles for transportation of equipment and personnel to new locations for shooting. For that matter, your automobiles might make it into a scene when vehicles are called for! Any motor vehicle that drives on public roads is legally required to be insured. Commercial auto insurance will help cover accidents that occur on the road, whether you’re actively filming a car chase or just picking up lunch for the artists and crew.

Workers’ Compensation Insurance

Your film production company will thrive on the talent and competence of its employees. Any part-time or full-time employees (not including independent contractors) must be offered workers’ compensation as a matter of law. Any on-the-job accidents that take place are potentially eligible for coverage under a good compensation policy, and it will help your workers to rest easy in the event of injuries sustained in the line of work. Disability and death benefits are also offered through this policy, providing coverage for not only employees but their families as well.

Commercial Umbrella Insurance

You never know what might happen on a given day at work, but this is especially true for workers in a film production company. Commercial umbrella insurance is an add-on policy that supplements maximized insurance, adding a new range of coverage for businesses looking to cover all their bases. Working with such a diverse array of people and equipment, your film production company can’t be too careful about which potential threats it leaves uncovered. Commercial umbrella insurance can be a major safety net for businesses.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your film production business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Film Production Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

It is advisable to purchase business insurance before commencing business operations. Failing to obtain coverage from the outset can potentially expose your business to various unforeseen risks and legal non-compliance.

Additionally, certain types of insurance like workers’ compensation and commercial auto insurance are mandatory by law. Furthermore, your enterprise may need business insurance to safeguard against specific risks like property damage and customer personal injury.

Not necessarily. Certain exceptions may be written directly into your film production business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.