Frozen Yogurt Business Insurance

Getting insurance for your frozen yogurt business is essential.

Frozen yogurt businesses need to be protected against things like claims of misrepresentation, product liability, and personal injury.

For example, a customer claims that you falsely advertised the health benefits of your yogurt or you fail to label one of your offerings with an allergen list.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Frozen Yogurt Business

General liability insurance is — generally speaking — one of the most important insurance policies for frozen yogurt businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

However, since there are numerous risks faced by frozen yogurt businesses that are not covered by general liability, many choose to invest in some of the following extra policies:

- Product liability insurance for the yogurt (and other products) you sell

- Workers’ compensation insurance to cover your employees if they are sick or hurt on the job

- Data breach insurance for any cyberattacks you may face

- Commercial auto insurance if your business uses any vehicles (e.g., for delivery, etc.)

The first step involved in selecting which insurance provider to choose is to identify which of the following categories best suits your needs

- Traditional brick-and-mortar insurers

- Online insurers

We tend to see small businesses preferring online insurers such as Tivly and Ergo Next over traditional ones as they offer a great budget option without sacrificing quality.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

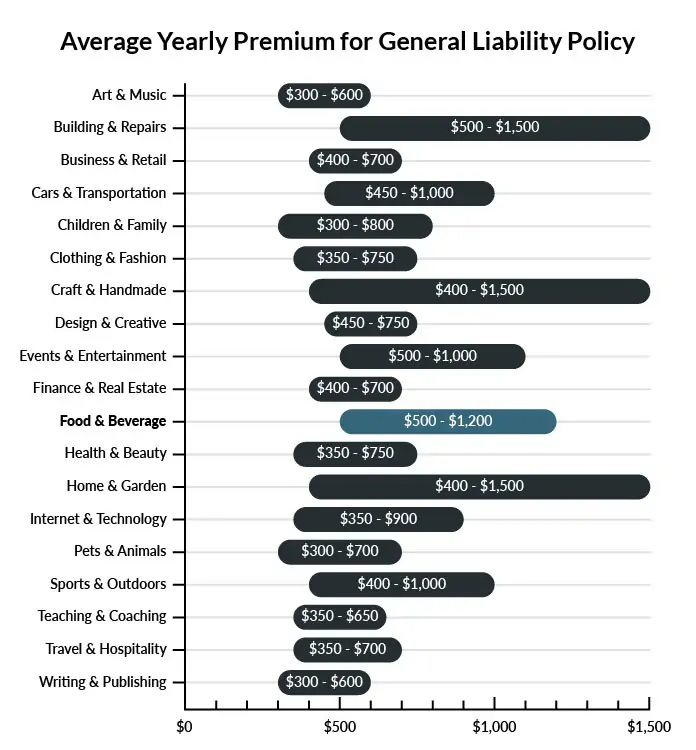

Cost of General Liability Insurance

On average, frozen yogurt shops in America spend between $500 – $1,200 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a frozen yogurt business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Frozen Yogurt Business

Example 1: As a customer is leaving your shop, she holds the door open for another customer who then stops to check his phone in the doorway. The door swings shut as he’s stopped, knocking him to the ground and causing him to break his wrist. He is angry and threatens to sue your shop for damages. General liability insurance would help cover his medical bills and potential legal fees you have..

Example 2: As your regular Monday delivery comes in, the overhead door on your loading dock malfunctions and severely damages the delivery van. The driver is unable to complete his orders for the day and the inventory inside is ruined. Your general liability policy will likely cover the repairs to the delivery van and replace the damaged inventory.

Example 3: After cleaning up a yogurt spill in the lobby, a customer slips on the wet floor before you can set out a caution sign. They are badly injured and demand that you pay for their medical expenses. With general liability insurance, you can file a claim and likely have all of their medical costs covered.

Other Types of Coverage Frozen Yogurt Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Product Liability Insurance

There is always a chance that a customer will claim that your product has caused them harm in some way. If this happens and they decide to pursue legal action, product liability insurance will pay for your legal fees and the cost of any settlement awarded in a lawsuit.

Workers’ Compensation Insurance

Workers’ compensation insurance will cover the cost of an employee’s medical bills if they are injured on the job as well as help cover lost wages if they are unable to work due to the injury. This coverage is legally required in most states for any company that has employees.

Data Breach Insurance

Many retail and food servicees now offer loyalty programs to their customers. To do this, it’s often necessary to store sensitive personal and financial information on your business computers. But keeping this information on file can make your computer system vulnerable to cyber-attacks. With data breach coverage, you can protect your business from possible lawsuits following a cyber attack.

Commercial Auto Insurance

If you deliver your frozen yogurt to any retail locations in your area, you should carry commercial auto insurance. In fact, you need this coverage even if you use your personal car for work duties. Your personal auto insurance won’t cover any accidents related to your job, so be sure to protect yourself and your employees with commercial auto insurance protection.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your frozen yogurt business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Frozen Yogurt Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes. It is important to proactively protect your frozen yogurt business with business insurance as it will face risks from day one, and insurance cannot be bought after the fact.

Additionally, it is essential that you double-check whether your business is subject to any legal obligation to carry specific insurance policies (e.g., workers’ compensation or commercial auto insurance).

Not necessarily. Certain exceptions may be written directly into your frozen yogurt business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.