Home Theater Installation Business Insurance

Getting insurance for your home theater installation service is essential.

Insurance is an essential requirement for home theater installation services to shield themselves from a range of potential risks. By providing coverage for physical injuries, property damage, and financial loss, insurance can offer reliable protection.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Home Theater Installation Business

General liability insurance is — generally speaking — one of the most important insurance policies for home theater installation businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

However, your home theater installation service may face other hazards that are not covered by a general liability policy. Here are three types of insurance to guard against those adverse occurrences:

- Commercial property coverage: This type of insurance provides coverage for the physical property and equipment owned by the business. For example, if the business’s equipment, such as tools and machinery, is damaged or stolen, property insurance can help cover the cost of replacing or repairing them.

- Professional Liability Insurance: Insurance of this kind, also known as errors and omissions (E&O) insurance, provides coverage for claims made by clients against the business for professional errors or negligence. For instance, if the home theater installation business fails to properly install a system and causes damage to a client’s property, the client may file a claim against the business for damages.

- Workers’ Compensation Insurance: This type of insurance, required by law in most states, provides coverage for employees who are injured or become ill while on the job. It would cover an employee who falls from a ladder or suffers an electrical shock.

After deciding on the type of insurance you must have, you will generally have to choose between the following two types of insurers:

- Traditional brick-and-mortar insurers: These insurers, like Allstate and Progressive, typically offer policies designed to cover extended periods of time. Premiums are generally higher.

- Online insurers: Insurtechs, such as Lemonade and Ergo Next, may offer insurance that can be purchased and activated instantly for a specific period. Overhead is low and in turn, so are the premiums.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

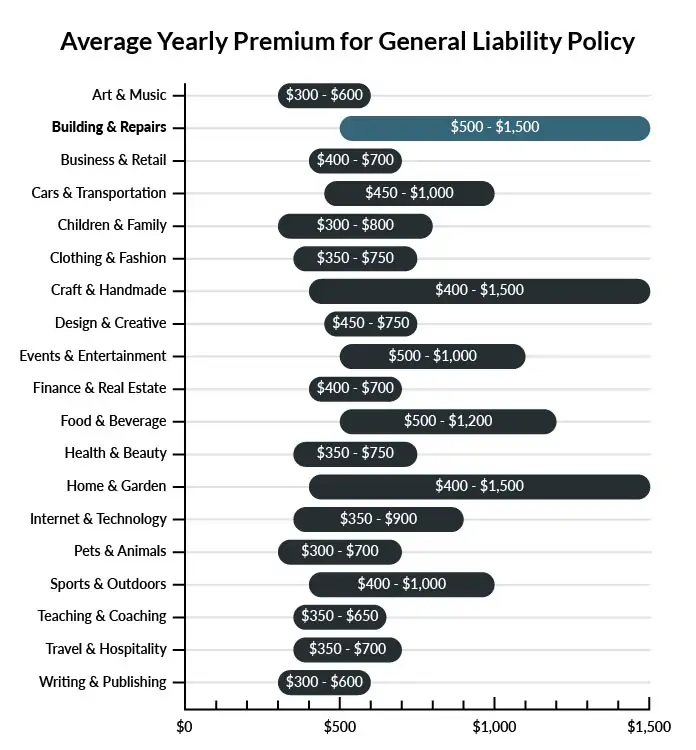

Cost of General Liability Insurance

On average, home theater installation businesses in America spend between $500 – $1,500 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a home theater installation business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Home Theater Installation Business

Example 1: You are installing a home theater and accidentally cause damage to a wall and the wood flooring. General liability insurance will cover the cost to repair or replace the client’s damaged property.

Example 2: A month after installing a new television, the home burns down in a fire. The origin traces back to your work. Your general liability policy should cover the cost to replace the home, the claimant’s personal property, and any other damages awarded to the third party as a result of your work. Should someone bring a lawsuit against you, your insurance carrier will pay your legal fees.

Example 3: One of your promotional social media posts implies that your competition does not provide quality service. The company has named your business in a defamation lawsuit, claiming their business has suffered as a result. A general liability policy will pay your legal team and damages awarded by the court.

Other Types of Coverage Home Theater Installation Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Commercial property insurance indemnifies the insured when a covered loss occurs. It pays for the repair or replacement of the physical property, as well as the business property kept onsite.

Businesses can purchase commercial property insurance as part of a business owner’s policy (BOP). Owners should discuss coverages and exclusions with their insurance agent to identify any coverage gaps. Most commercial property policies exclude business property taken off premises without the properly added endorsements. In some instances, a separate Inland Marine policy may be necessary.

Commercial Auto Insurance

The home theater industry requires employees to travel from one job site to another. Since personal auto policies exclude business vehicles, owners must purchase a commercial auto policy for business vehicles. In the event of an accident, the policy would cover the cost to repair your vehicle, as well as any auto liability claims that may arise from an accident.

Businesses can purchase commercial auto insurance with a business owners’ policy (BOP) or as a standalone policy, depending upon the carrier.

Workers’ Compensation Insurance

State law requires that businesses carry workers’ compensation insurance on all employees. When an employee’s work causes illness or injury, the policy can pay for medical treatment and lost wages while he/she is recovering.

Workers’ compensation is typically purchased as a standalone policy.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your home theater installation business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Home Theater Installation Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes, it is good practice to have business insurance before starting a home theater installation business. Business insurance can help protect your venture from financial loss due to unexpected events such as property damage, lawsuits, and other unforeseen circumstances that may arise during the course of its business operations.

Not necessarily. Certain exceptions may be written directly into your home theater installation business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.