Hot Sauce Company Insurance

Getting insurance for your hot sauce company is essential.

Hot sauce companies need to be protected against claims of things like product liability, false advertising, and food safety violations.

For example, your company’s products are found to have caused food poisoning to customers, or a customer claims that you falsely advertised the spiciness of some of your products.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Hot Sauce Company

General liability insurance is — generally speaking — one of the most important insurance policies for hot sauce companies.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

You may find that general liability fails to provide enough protection for your hot sauce company. In this case, some of the following policies may be useful:

- Product liability insurance: Due to the potent ingredients often used in hot sauce, product liability is important to protect your company from claims of burns or allergic reactions suffered by customers.

- Business interruption insurance: Your company, like any other business, is susceptible to events that could interrupt its operation. This policy protects your company from the loss of income in the event it is temporarily shut down.

- Commercial auto insurance: As your company will likely need commercial vehicles in order to transport its products, this policy will be essential to protect you from the financial losses resulting from property damage or bodily injury caused by these vehicles.

It can often be difficult to decide which insurance provider to select. One of the first steps involves choosing which of the two primary groups best suits your business.

- Traditional brick-and-mortar insurers — Providers with a physical store and an insurance agent. Firms such as Nationwide and The Hartford are included in this category.

- Online insurers — Providers that are based purely online and utilize AI instead of insurance agents. Firms such as Ergo Next and Tivly are included in this category.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

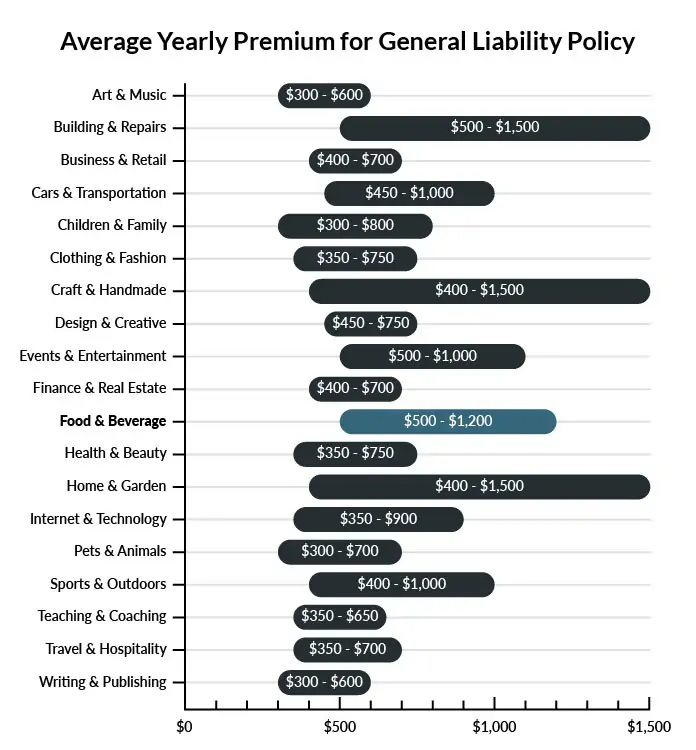

The average hot sauce company in America spends between $500-$1,200 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a hot sauce company to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Hot Sauce Company

Example 1: To produce your hot sauce, you may have to operate out of a large warehouse space that includes lots of different machinery and tools. In these types of buildings, the risk of common accidents and injuries is increased. Luckily, with the help of general liability coverage, you can protect any visitors to your workspace in the event that they become injured after a slip and fall or their personal property is damaged.

Example 2: As your business grows, there’s a good chance that you may start to sell your hot sauce at a retail location. If your parking lot isn’t maintained properly and a customer is involved in an accident due to dangerous conditions, you could be sued for damages. With the help of general liability coverage, you can rest easy knowing that you are protected against common accidents, inside and outside of your building.

Example 3: Loading and unloading your product is always a risky process—just one false move and a whole batch of hot sauce could come crashing to the ground. But if you drop a pallet of hot sauce as you load it into a client’s vehicle, you could be held responsible for damages to their personal property. While general liability insurance can’t get back those wasted hot sauce production hours, it can help to pay for repairs.

Other Types of Coverage Hot Sauce Companies Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Product Liability Insurance

Hot sauce is rising in popularity among foodies and daredevils across the country. And while most customers understand there is a risk involved in using your product, there is still a chance that you could be sued for certain damages that may be caused by the products you sell. Product liability coverage can work to protect your business if a customer decides to pursue a lawsuit related to damages caused by your hot sauce or other products.

Business Interruption Insurance

If there is a problem in your factory due to a fire, inclement weather, or even burglary and you have to shut down production, this coverage can help to cover some of the losses your business may incur. This is a great coverage option for businesses both large and small to help prevent closing your doors for good after an interruption to your regular production schedule.

Home-Based Business Insurance

If you are running your hot sauce business out of your own home, there’s a good chance that your homeowners’ insurance policy won’t cover accidents that are related to any of your business activities. Luckily, by investing in this special home-based business insurance option, you can protect your home and your business in the event of a work-related accident.

Commercial Auto Insurance

Whether you have your very own fleet of delivery vehicles for your hot sauce or you plan on using personal employee vehicles to make deliveries, commercial auto insurance can help to cover damages if you or your team are found to be liable for damages in an auto accident. This coverage is especially important if you use personal vehicles for work-related duties because your personal auto insurance policy will not cover these types of accidents.

Commercial Umbrella Insurance

The hot sauce industry is on fire right now in the US, and businesses are at risk for increased liability judgments as they gain popularity. A commercial umbrella policy provides an extra layer of protection for your business in the event that your primary policy is exhausted.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your hot sauce company:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Hot Sauce Company Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Due to its nature, a hot sauce company is inherently exposed to a variety of risks from the outset. The best way of tackling this risk is proactively acquiring business insurance.

In fact, it is highly likely that certain policies will be a legal requirement for your hot sauce company to be able to operate.

Not necessarily. Certain exceptions may be written directly into your hot sauce company insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.