Hotel Business Insurance

Getting business insurance for your hotel is essential.

By obtaining insurance, hotels can safeguard themselves against financial losses, property damage, and harm to individuals.

For example, a guest may claim she has lost valuable personal property as a result of your negligence and demands compensation. Thankfully, there is insurance that would indemnify you for the costs incurred.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Hotel Business

General liability insurance is — generally speaking — one of the most important insurance policies for hotels.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

While general liability insurance provides coverage for a variety of risks, it may not be sufficient to cover all the risks that your business may face. For instance, some risks may require coverage from specialized policies, such as those that offer:

- Commercial property coverage: This kind of coverage is designed to protect the hotel’s physical property, such as the building, equipment, and inventory, against damages or loss due to fire, theft, or other covered perils.

- Workers’ Compensation Insurance: Hotels are generally labor-intensive businesses that employ a large number of people, including housekeeping staff, maintenance workers, and restaurant workers. Workers’ compensation insurance provides benefits to employees who are injured or become ill as a result of their job.

- Business income coverage: This is a policy that will provide coverage for loss of income and additional expenses incurred by the hotel in the event of a disaster or other covered event that forces the hotel to temporarily close or suspend operations.

When searching for an insurance company, it’s important to keep in mind that there are two main types to choose from, traditional brick-and-mortar insurers such as Nationwide or Allstate, and online insurers such as Ergo Next or Tivly.

The advantages and disadvantages of each will depend on your specific circumstances. However, if you’re a small business owner looking for affordable and high-quality insurance, it’s generally recommended to opt for an online-based insurer.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

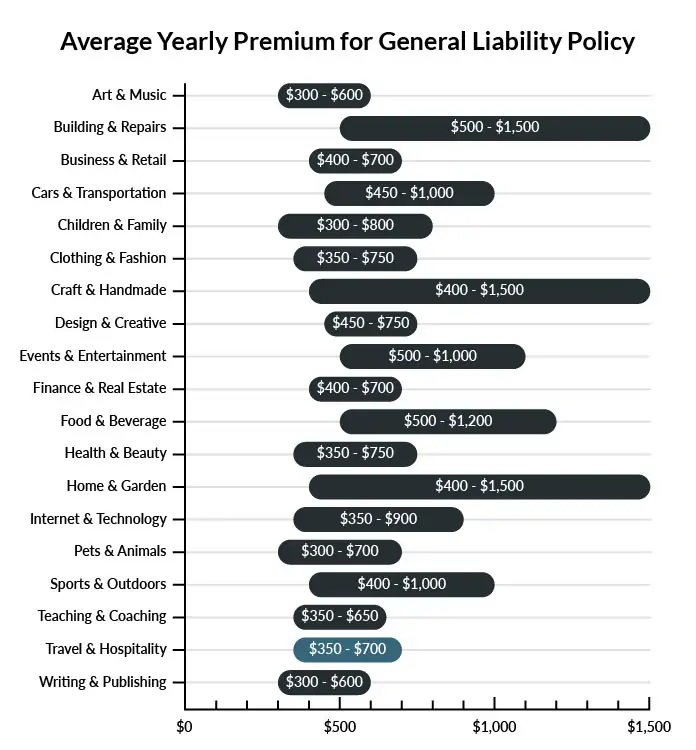

The average hotel in America spends between $350-$700 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a hotel business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Hotel Business

Example 1: A luggage carrier’s wheel locks up while a child is riding the carrier, causing the child to fall off the carrier. They sustain a head injury during the fall. General liability insurance would likely cover necessary medical care.

Example 2: A young child finds their way to the pool and gets in the water. They haven’t learned to swim, and the result is a tragic drowning accident. General liability insurance would likely cover any lawsuit filed against the hotel seeking compensation for the incident.

Example 3: While carrying luggage into the hotel, a guest slips on some ice in the parking lot and falls. General liability insurance would probably cover any settlements related to injuries that they sustained in the fall.

Other Types of Coverage Hotel Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Commercial property insurance covers business-owned real estate from perils such as fire and wind. Most policies also cover equipment and supplies that are kept at the insured property. Hotel buildings are often worth substantial amounts. Make sure your hotel’s policy provides enough coverage to rebuild the hotel building if it’s destroyed by a covered peril.

Commercial property insurance is often included in a business owner’s policy (BOP).

Workers’ Compensation Insurance

Hotels usually need workers’ compensation insurance because they employ staff. This coverage protects against work-related illnesses and injuries, and most states require businesses that hire employees to carry the coverage.

Cyber Attack Insurance

Cyber attack insurance helps protect against both malicious online attacks and non-criminal data breaches. These sorts of incidents are commonly excluded by general liability policies. When selecting cyber attack insurance, check to see whether the policy includes coverage for ransomware attacks. More than one hotel has had their data seized by ransomware, and sometimes the attacks have rendered electronic room locks inoperable.

Cyber attack insurance can be procured on its own or within a package policy.

Commercial Auto Insurance

If your hotel has a shuttle van, the van needs to be insured with commercial auto insurance. States generally require businesses to get minimum levels of coverage for their vehicles, and many businesses purchase more than the minimum coverage requirements.

Commercial auto insurance can be procured on its own or within a package policy.

Business Interruption Insurance

Operating a hotel comes with regular expenses that must be paid even when there’s a disaster. If your hotel is shut down following a covered disaster, business interruption insurance might help cover recurring expenses while the hotel isn’t generating revenue.

Business interruption insurance is often included in a BOP.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your hotel business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Hotel Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

In broad terms, that is correct. Certain categories of insurance are mandated by state regulations. Furthermore, a business may face various types of risks, such as property damage, financial losses, and personal injuries, even prior to commencing operations. These factors mean it’s important to get business insurance right from the start.

Not necessarily. Certain exceptions may be written directly into your hotel business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.