Jewelry Store Insurance

Getting insurance for your jewelry store is essential.

Jewelry stores need to be protected against claims of things like fraud, breach of contract, and violations of consumer protection regulations.

For example, an employee knowingly sells a fake piece of jewelry as authentic, or you damage a customer’s jewelry during one of your cleaning services.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Jewelry Store

General liability insurance is — generally speaking — one of the most important insurance policies for jewelry stores.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

That being said, some of the following extra policies may be useful for supplementing your jewelry store’s protection:

- Product liability insurance: This would keep your store financially covered if a customer decided one of your products injured them.

- Commercial property insurance: Stocking a jewelry store requires a significant financial investment. This policy protects that investment if your inventory is damaged or destroyed.

- Crime insurance: Provides coverage for the cost of damages if your store is the victim of criminal activity.

One tip to make the process of selecting an insurance provider easier is to first decide which type of insurer best fits your business’ needs:

- Traditional brick-and-mortar insurers — Typically more expensive policies as these firms rent out physical stores and hire insurance agents.

- Online insurers — These firms, such as Tivly and Ergo Next, are generally more affordable because their online approach requires less capital to run.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

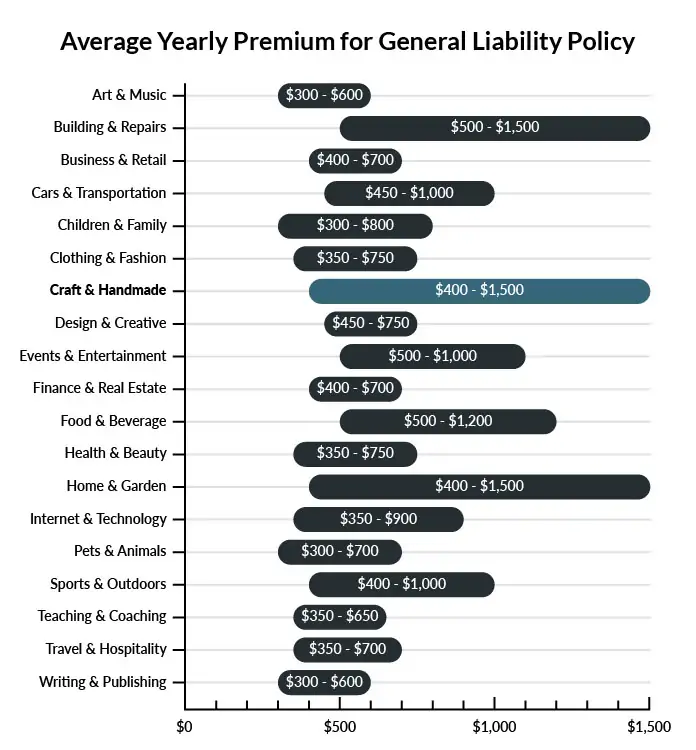

The average jewelry store in America spends between $400-$1,500 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a jewelry business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Jewelry Business

Example 1: A customer is looking at a display case when she leans too hard on the glass. The glass breaks, severely cutting her hand, and she requires immediate medical care. A general liability insurance policy will likely assist in paying for her medical treatment.

Example 2: You have hired a marketing firm to develop a new ad campaign for your jewelry business. One of your competitors files a lawsuit, claiming the ad libeled her business. Your general liability insurance policy will pay for the cost of your legal defense. It will also pay for the cost of a settlement if one is necessary.

Example 3: One of your employees is rushing to answer a ringing phone when he accidentally runs into a customer. The impact knocks the customer into a display case, causing him injury that requires medical care. He decides to sue your business. Your general liability insurance policy will pay your legal costs, including any payouts or settlements that you wind up paying as a result of the lawsuit.

Other Types of Coverage Jewelry Stores Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Product Liability Insurance

There is always the chance that a customer could decide that one of your products caused them injury. If this happens and the customer files a lawsuit, your product liability insurance would pay for hiring an attorney and your various legal costs. It would also cover the cost If you settle the case out of court.

Commercial Property Insurance

Stocking inventory for a jewelry business is a serious financial investment. If something were to happen that destroyed your inventory, like a major fire, it would be extremely costly to replace. Commercial property insurance would help to pay for the replacement of your inventory.

Workers’ Compensation Insurance

In most states, if you have employees, you are required by law to carry workers’ compensation insurance. If one of your employees is injured performing a work-related task and requires medical care, workers’ comp insurance would pay for it. Your policy would also help to cover the employee’s lost wages if they were unable to work due to the injury.

Crime Insurance

Crime insurance is designed to protect your jewelry business if you are the victim of criminal activity—whether the criminal activity is performed by your employee or by someone not associated with your business. Should a crime occur, like an employee stealing some of your inventory, then your crime insurance policy would help to cover the cost of damages to your business.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your jewelry store:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Jewelry Store Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

A jewelry store requires substantial investment in order to get started. In order to protect this investment from the risks such a business will encounter from its first day, business insurance must be obtained in advance.

In fact, there are instances where certain policies are a legal requirement of operation, such as workers’ compensation and commercial auto insurance.

Not necessarily. Certain exceptions may be written directly into your jewelry business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.