Laundry Delivery Service Insurance

Getting insurance for your laundry delivery business is essential.

Laundry delivery businesses need to be protected against things like claims of property damage, personal injury, and breach of contract.

For example, your laundry delivery business could be accused of damaging clothing garments, or a delivery driver could get into an accident.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Laundry Delivery Service

General liability insurance is — generally speaking — one of the most important insurance policies for laundry delivery businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

If you want to increase your coverage beyond what general liability insurance provides, consider the following policies:

- Product liability insurance: Protects your laundry delivery business from any claims that you damaged a customer’s property with one of your products like a cleaning solution.

- Commercial property insurance: Provides your laundry delivery business with financial protection to pay for the repair or replacement of your company’s commercial property if they’re damaged, lost, or stolen. This can include, for example, laundry machines.

- Workers’ compensation insurance: Protects workers financially if they’re injured or become ill on the job.

When shopping for insurance, take into account the two basic types of providers:

- Traditional brick-and-mortar insurers — These firms typically hire insurance agents and sell policies from physical offices. This business model often results in higher prices for customers due to the higher cost of operation.

- Online insurers — These providers operate entirely online, which lets them charge less because of their lower overhead.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

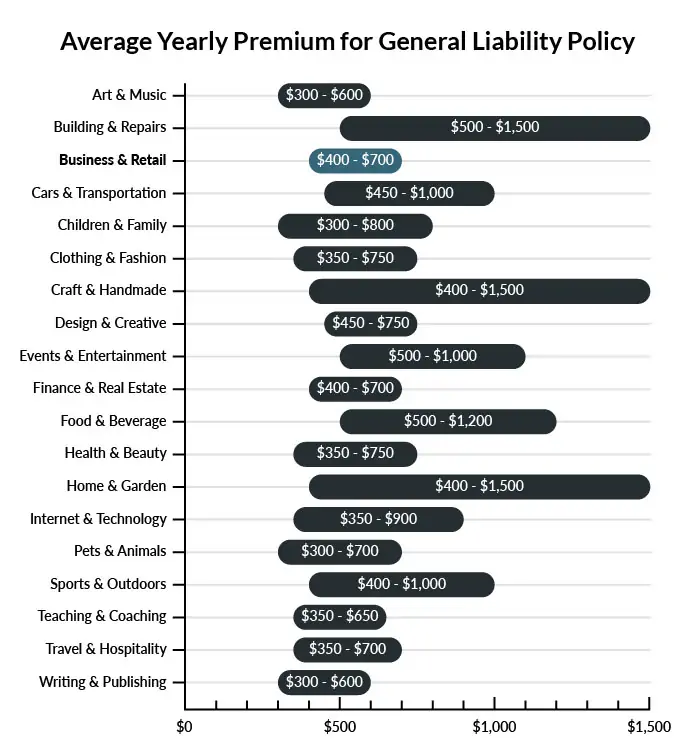

On average, laundry delivery services in America spend between $400 – $700 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a laundry delivery service to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Laundry Delivery Service

Example 1: Your employee fails to secure the client’s property after a pickup. When he arrives back at the office, he realizes most of the laundry fell out of the vehicle during transport. General liability insurance should pay the cost to replace the client’s property.

Example 2: While showing a potential new employee the operation, he gets burned by a piece of equipment. A general liability policy would pay his medical bills. If he sues for additional damages, the policy should cover your legal fees and associated costs.

Example 3: While unloading deliveries, your employee backs into a building, causing damage that exceeds the limits of your commercial auto policy. Your general liability policy may cover the cost to repair the building, once you exhaust the underlying limits.

Other Types of Coverage Laundry Delivery Services Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Auto Insurance

An auto accident can occur while employees are performing business-related activities. Commercial auto insurance can pay to repair damaged vehicles, liability claims, and lost equipment. While minimum coverage limits are state-mandated, business owners should protect themselves by considering higher limits.

You can purchase commercial auto insurance as a standalone policy or as part of a business owner’s policy (BOP), depending upon the carrier.

Commercial Property Insurance

Building owners and renters should consider purchasing a commercial property insurance policy built around their specific needs. This policy will cover costs to repair or replace business-owned assets, including the physical property and/or its contents.

You can purchase commercial property insurance as part of a business owner’s policy (BOP).

Workers Compensation Insurance

State law requires businesses with employees to carry workers compensation insurance. Its purpose is to provide medical coverage for on-the-job injuries. In the event of a more serious incident, the company will get legal representation and court-awarded damages paid up to the limits of the policy.

Insurers write workers compensation insurance as a standalone policy.

Inland Marine Coverage

A standard policy may exclude coverage for a customer’s property while in their possession or in-transit. Inland marine coverage will cover property that isn’t on your business’s physical site. For an additional premium, the insured should be able to purchase inland marine coverage as an endorsement.

Laundry delivery business owners should have a conversation with their insurance agent to determine if this is a necessary coverage.

Commercial Umbrella Liability Insurance

This profession requires handling of non-owned property and the use of chemicals. Owners concerned with the liability risks should purchase a commercial umbrella policy. This insurance acts as an additional layer of protection, taking over where the underlying general liability policy leaves off.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your laundry delivery service:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Laundry Delivery Service Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Because laundry delivery services face a variety of risks, you should protect yours from the beginning with adequate business insurance.

In fact, it is highly likely that at least a few insurance policies (e.g., commercial auto and workers’ compensation insurance) will be obligated for your business by law.

Not necessarily. Certain exceptions may be written directly into your laundry delivery service insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.