Modeling Agency Business Insurance

Getting business insurance for your modeling agency is essential.

This is because modeling agencies need to be protected against things like professional negligence claims, indemnification-related disputes, and data breaches.

You can also use business insurance in order to safeguard your agency’s equipment from potential theft and/or damage.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Modeling Agency

General liability insurance is — generally speaking — one of the most important insurance policies for modeling agencies.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Even so, your modeling agency will likely benefit from purchasing additional coverage; this is because a general liability policy will not in itself be enough to safeguard your business from all foreseeable risks.

Additional insurance policies you will likely benefit from considering include:

- Professional liability insurance — Covers your agency against liability that arises due to a negligent act or omission.

- Workers’ compensation insurance — Covers your agency against employment law-related disputes (e.g., wrongful termination claims, etc.).

- Data breach insurance — Covers your agency against liability that arises as a result of a data breach (e.g., leaked sensitive information, etc.).

- Commercial property insurance — Covers the cost of repairing or replacing your agency’s furniture and other commercial equipment in the event of damage or theft.

You will also need to find the right business insurer for your agency.

Even though there are several great options to choose from, we found that they all fall within one of the following two categories:

- Online insurers (recommended) — This category includes insurers that use AI — instead of an insurance agent — to offer personalized coverage. Online insurers tend to be significantly more affordable.

- Brick-and-mortar insurers — This category includes “conventional” US-based insurers that have been operating for several decades (if not over a century) and have a long history of strong financial strength.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

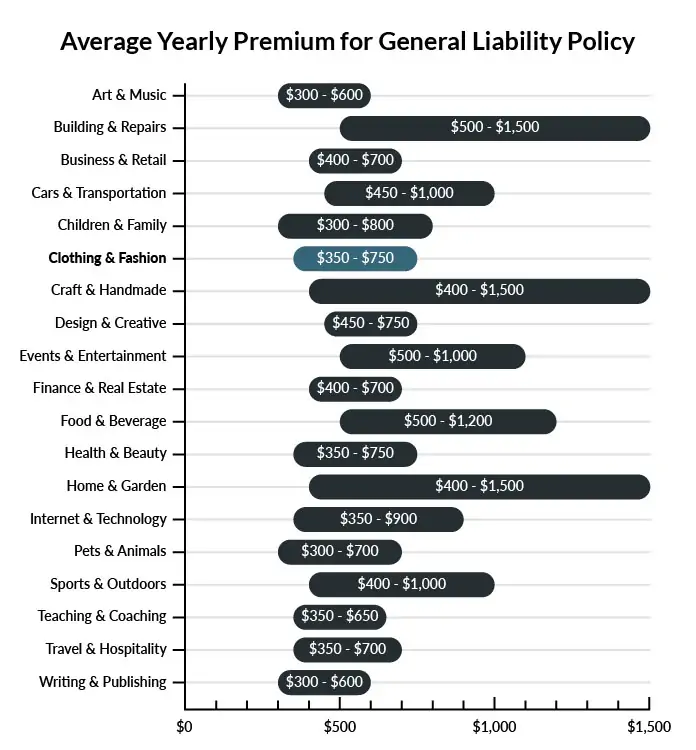

On average, modeling agencies in America spend between $350 – $750 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a modeling agency to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our affordable business insurance review.

Common Situations That General Liability Insurance May Cover for a Modeling Agency

Example 1: During a photoshoot, a freelance photographer trips on a set and injures himself. Because his injuries leave him unable to work for several months, he sues for damages to cover his medical bills as well as pain and suffering. General liability insurance would pay for your legal fees and the damages awarded by a court.

Example 2: At an event held by your modeling agency, one of your models knocks over a vase valued at $7,000. The venue sues, asking for a replacement vase. Your general liability policy would cover the replacement cost of the vase.

Example 3: Your designer accidentally uses a photo under copyright protection as part of your website rebuild, and the photo’s owner sues for copyright infringement. General liability insurance would cover your legal fees and the resulting payout.

Other Types of Coverage Modeling Agencies Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Content and Equipment Insurance

If you don’t own the warehouse in which your agency operates, but you store property there, content and equipment insurance extends coverage to those items in the event of a fire, burglary, or natural disaster.

If your agency conducts both on-site and off-site photo shoots, be sure to discuss policy limitations with your insurance provider because you may need portable equipment insurance when working off-premises.

You can typically purchase content and equipment insurance as part of a business owners’ policy (BOP).

Professional Liability Insurance

Your job requires you to be creative and take risks, but these ideas may not always work out as expected. If a client decides your work caused them harm, they could hold you liable. Professional liability insurance provides protection if you face a lawsuit from your professional advice or services.

Workers’ Compensation Insurance

As a modeling agency, you employ a team of professionals whose health and well-being is critical to the business’ success. To ensure coverage for on-the-job injuries and illnesses, state law requires you to purchase workers’ compensation coverage for both your part-time and full-time employees.

While your state may allow exemptions for business owners, consider including yourself in your workers’ compensation policy if you engage in the daily operation of the business.

You can typically purchase workers’ compensation insurance as a standalone policy.

Business Interruption Insurance

If a fire or other major event forces you to temporarily close, business interruption insurance would help pay for a move to a temporary location as well as help cover your bills and financial losses until you can reopen.

You can typically purchase business interruption insurance as part of a business owner policy (BOP).

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your modeling agency:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Modeling Agency Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Generally speaking, yes. Getting the right modeling agency business insurance before you begin operating can end up saving you thousands of dollars in the long term.

This is because liability could technically arise as soon as you begin interacting with clients, hiring employees, or purchasing equipment.

Not necessarily. Certain exceptions may be written directly into your modeling agency insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.