Real Estate Photography Business Insurance

Getting insurance for your real estate photography business is essential.

Real estate photographers need to be protected against things like personal injury claims, commercial property disputes with providers, and property damage claims.

For instance, if someone gets injured on your property while doing a photoshoot, or if one of your employees accidentally damages a client’s property while on assignment, you could face substantial claims for compensation.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Real Estate Photography Business

General liability insurance is — generally speaking — one of the most important insurance policies for real estate photographers.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

There are other types of insurance policies real estate photographers may want to consider:

- Errors and omissions (E&O) insurance: This coverage can protect you from claims of negligence or mistakes made in your work.

- Equipment breakdown insurance: As a real estate photographer, the equipment you use such as cameras and lighting gear can be costly and essential to your work. This insurance can keep your business in operation in the event of a loss.

- Commercial auto insurance: This policy provides coverage for vehicles used for business purposes, including those used by real estate photographers to transport equipment and travel between job sites. Without this type of coverage, any accidents or damages that occur while using a vehicle for business purposes may not be covered under personal auto insurance policies.

When acquiring business coverage, you’ll choose between these types of insurers:

Traditional brick and mortar insurers: Brick and mortar insurers have a physical presence with offices in various locations. They offer face-to-face interactions with agents who can answer questions and address concerns about policies. Their premiums are usually higher in price.

Online insurers: Operate solely through digital platforms without physical locations. Customers can purchase policies quickly from anywhere, at any time. Their application processes are streamlined with little to no paperwork required. Moreover, online platforms allow customers to compare rates from multiple providers easily. Premiums are lower due to lower operational costs and greater competition.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

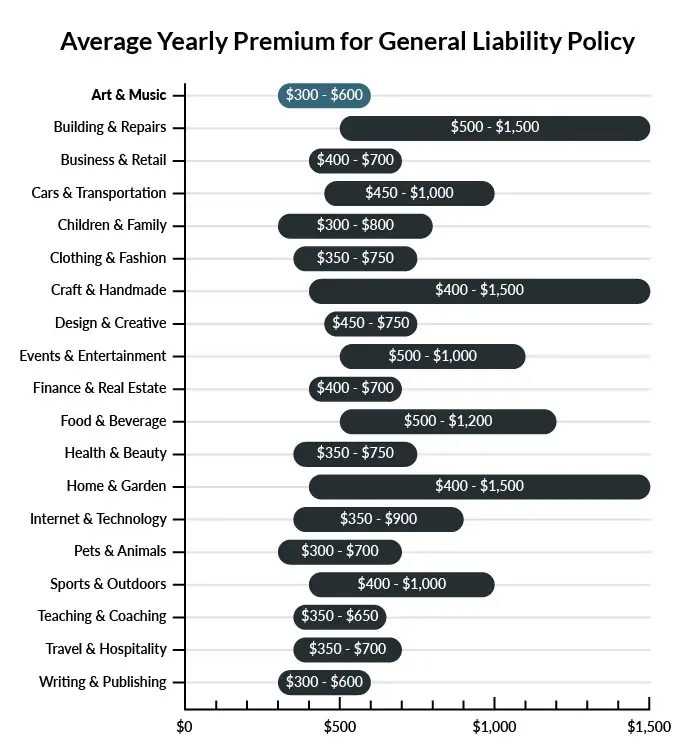

On average, real estate photographers in America spend between $300 – $600 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a real estate photography business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our low-cost business insurance review.

Common Situations That General Liability Insurance May Cover for a Real Estate Photography Business

Example 1: During a customer photo shoot, your client trips on a power cord. This causes a light tower to fall and injure the client. General liability insurance would cover you against bodily injury claims and potential payouts.

Example 2: You are hired as a personal photographer for a high-profile property. After the photoshoot, pictures from inside the house, taken on a smartphone, appear on social media. The owner accuses you and your team of taking and posting the pictures, then files a lawsuit against your business. A general liability policy may be able to cover the legal fees and any money awarded to the property owner.

Example 3: While taking pictures of a client’s property, you accidentally crack an antique mirror. The mirror is one-of-a-kind and quite expensive. Your general liability policy may be able to cover the cost of the damaged antique.

Other Types of Coverage Real Estate Photography Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Professional Liability Insurance

Professional liability insurance, commonly known as Errors & Omissions (E&O) is a coverage every real estate photographer should consider. As a photographer, events often occur that are out of your control. If a memory card fails, causing you to lose pictures from an event, you could face a court challenge. Whether from human error or faulty equipment, a professional liability policy protects you from such claims.

Commercial Auto Insurance

Real estate photographers use their own vehicles to drive from one client home to the next. Since most personal auto policies will not cover business pursuits, your state will require you to carry a certain level of commercial auto insurance.

In addition to requiring insurance, your state may also mandate the minimum coverage all drivers must carry. To shield you properly against potential losses, consider your personal and professional financial situation when selecting your commercial auto insurance limits. Consider selecting a limit higher than required by your state.

You can typically purchase commercial auto insurance as part of a business owners’ policy (BOP).

Home-Based Business Insurance

Since this type of business involves regular work in the field, many real estate photography business owners opt to operate out of their homes. If you then store your equipment in your residence when it’s not in use, you’re leaving a potential insurance coverage gap. If your home suffers a loss, or an accident occurs as a result of business activities, you may find you are uninsured or underinsured for these losses. Home-based business insurance fills in those gaps, protecting against losses excluded by a standard homeowners policy.

You can typically purchase home-based business insurance as a part of a business owners policy (BOP). For an additional premium, some homeowner’s insurance policies offer this coverage as a rider (an extension of coverage).

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your real estate photography business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Real Estate Photography Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes, those engaging in real estate photography should obtain general liability business insurance coverage. This policy safeguards against potential claims arising from bodily injury or property damage caused by the photographers themselves or their equipment during photo shoots. Purchasing ahead of time means being able to capitalize on opportunities when they come your way, even before officially opening for business.

Not necessarily. Certain exceptions may be written directly into your real estate photography business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.