Smoothie Business Insurance

Getting insurance for your smoothie business is essential.

This is because smoothie businesses need to be protected against risks that could foreseeably occur and cause them serious financial harm, such as accidental injuries, product liability disputes, and employment law claims.

For example, if an employee was to get injured while working on the job or if a customer suffers an allergic reaction from an improperly-marked smoothie.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Smoothie Business

General liability insurance is — generally speaking — one of the most important insurance policies for smoothie businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Even so, some business owners will choose to purchase additional coverage in order to protect themselves from a higher number of risks.

For example, they may decide to purchase:

- Product liability — Protects in the event that a consumed smoothie causes a customer harm (e.g., food poisoning, etc.).

- Workers’ compensation — Protects against employee disputes and claims, such as personal injuries.

- Commercial property — Protects your commercial equipment in the event that it gets accidentally damaged or stolen.

You will also need to spend some time in order to find the right coverage provider for your business. Currently, there are two types of insurers available for small business owners:

- Online insurers: Popular examples include Ergo Next Insurance and Tivly.

- Brick-and-mortar insurers: Popular examples include Nationwide and The Hartford.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

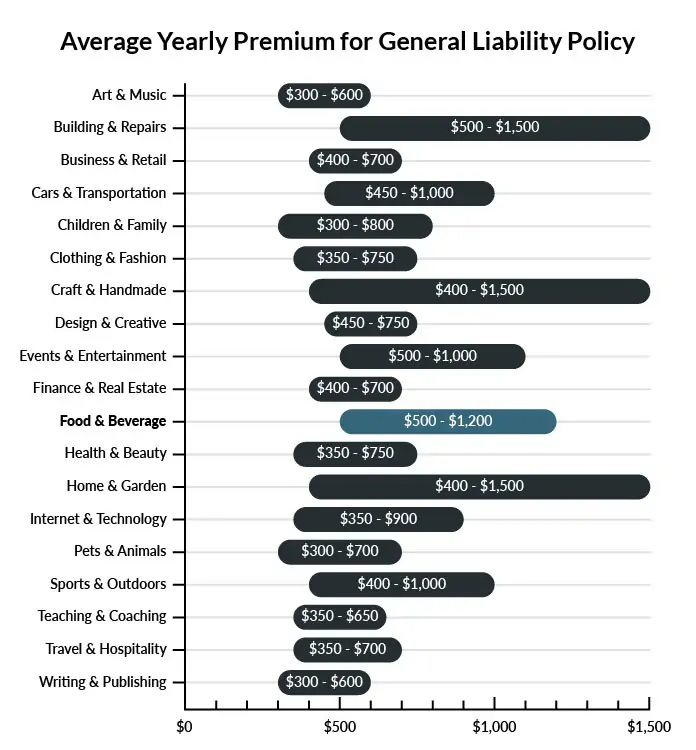

The average smoothie store in America spends between $500 – $1,200 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a smoothie business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our low-cost business insurance review.

Common Situations That General Liability Insurance May Cover for a Smoothie Business

Example 1: An employee spills a smoothie on the floor in front of the counter and quickly mops up the mess. He forgets to leave a notice that the floor is slippery due to mopping, and an elderly customer slips on the wet floor. The customer’s ankle is broken, and your company is found liable. General liability insurance could likely help in covering payments ordered by the court or any settlement reached regarding medical expenses.

Example 2: An employee is in a hurry, hauling a large box of newly arrived store equipment through the customer waiting area instead of the back door. He loses his grip, dropping the heavy box on a customer’s foot. The customer suffers a bone fracture and requires a cast and a wheelchair for several months. If found liable in court, your business would probably be covered by general liability insurance for the cost of a settlement or ongoing medical payments.

Example 3: An employee at one of your locations decides to begin making and selling an imitation smoothie sold by a competing smoothie store. She advertises this product on a chalkboard sign outside, and word gets around to the competing business. They sue your company for copyright infringement. Your business would likely obtain coverage from general liability insurance in the event of a settlement or a payment ordered by the court.

Other Types of Coverage Smoothie Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Product Liability Insurance

This is a key policy for all businesses that sell food products. Between choking hazards, allergies, or other food-related damages, a company can find itself in hot water without a policy to cover serious product lawsuits. It is necessary to keep your smoothie business safe with a product liability policy in case a customer suffers unexpected health consequences that are linked to your beverages. This insurance covers a variety of damages caused by the products you sell, and it can be custom-tailored to your business for maximum effectiveness.

Commercial Property Insurance

A given smoothie store location will contain not only ingredients and supplies but also expensive machinery used in custom-crafting its advertised smoothie beverages. Commercial property insurance is essential for business owners looking to protect their inventory, equipment, and owned real estate investments from threats like fire and weather. Avoid costly replacement losses from unpredictable disasters with a commercial property policy.

Workers’ Compensation Insurance

Your business may begin as a smoothie stand, but if you make sound business choices, with a bit of luck, you can begin expanding. Expansions often include a need for employees who will be working under you. If you hire part-time or full-time workers to help run your business, you will be legally required to purchase workers’ compensation policies. This insurance keeps your employees covered in the event of on-site accidents and provides disability and death benefits for any damages that they may suffer while in the workplace.

Business Interruption Insurance

A successful business is an active business. But what happens when unexpected events cause your business to shut down temporarily? It can be disastrous for a business to go dormant, not only because of the loss of revenue during a shutdown but also the potential discouragement or confusion of customers who decide not to return. Business interruption insurance can provide coverage when your company’s storefronts or other facilities need to undergo repairs, relocations, or even wait out nearby major construction that prohibits access to your location. Some causes of a temporary shutdown include fire, tornadoes, and similar destructive forces.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your smoothie business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Smoothie Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

We recommend getting business insurance before you start your smoothie business due to the fact that it’s the most safe way of ensuring that you will not have to face a legal claim or other large dispute while not being insured.

This is because liability could theoretically arise as soon as you begin interacting with clients.

Not necessarily. Certain exceptions may be written directly into your smoothie business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.