Used Tire Store Insurance

Getting business insurance for your used tire store is essential.

This is because owners of used tire stores need to protect themselves against a variety of foreseeable risks, such as those that relate to property damage, product liability claims, and work-related injuries.

For example, you accidentally sell a used tire that’s insufficient and causes a car crash, or an employee injures themselves while helping a customer and requires time off.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Used Tire Store

General liability insurance is — generally speaking — one of the most important insurance policies for used tire stores.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Having said that, it is important to understand that not all used tire stores will be adequately covered with just a general liability policy.

This means that — depending on your unique risks — you might benefit from purchasing the following policies:

- Errors and omissions (protects against negligent acts or omissions)

- Workers’ compensation (protects against employment law disputes)

- Business income (covers part of your lost income if you need to shut down)

You will also need to decide what type of business insurer you will work with. There are two options available for small business owners:

- Traditional brick-and-mortar insurers (e.g., Nationwide, The Hartford, etc.).

- Online insurers (e.g., Ergo Next Insurance, Tivly, etc.).

All in all, we recommend going for an online insurer as a small business due to the fact that coverage can be obtained at a much lower rate.

This is because online insurers benefit from having lower operating costs (e.g., no insurance agent, etc.).

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

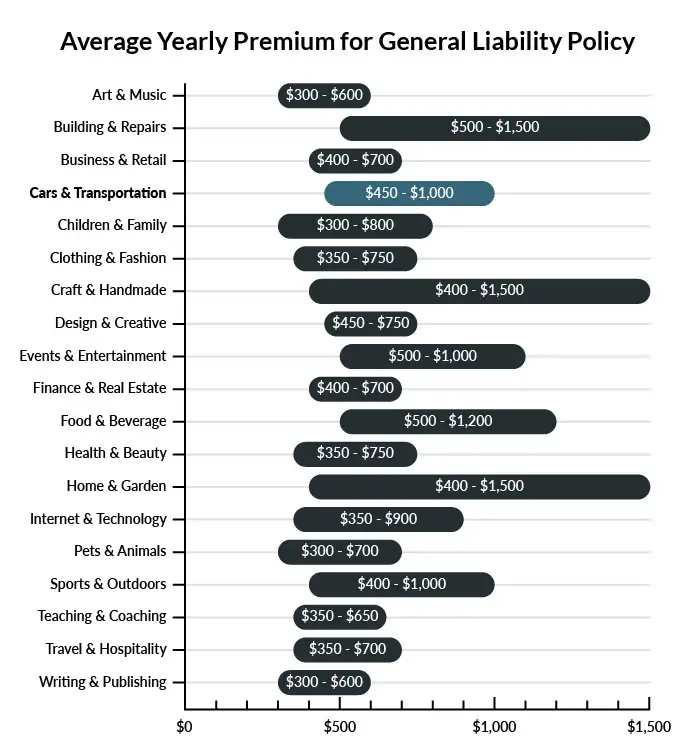

The average used tire store in America spends between $450 – $1,000 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a used tire store to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our low-cost business insurance review.

Common Situations That General Liability Insurance May Cover for a Used Tire Store

Example 1: While retrieving a tire from a tall stack, one of your employees drops it down the ladder. It rolls out of the garage and into traffic, causing a car wreck in which two people are injured. If found liable in court, your company would probably be covered for some of the ordered payments and/or settlements related to car repair and medical fees.

Example 2: An employee drives a customer vehicle into your business’s garage. Unfamiliar with the car, he accidentally rams it into the side of a steel insert, badly denting and scuffing the front fender of the customer’s car. General liability insurance would probably be able to cover your business in the event it is found liable for this damage.

Example 3: A customer prefers to stand nearby and watch as your employees replace the tires on his old car. The parking brake is worn down and the vehicle rolls backward onto the customer’s foot, breaking several of his toes. If your business is found liable, general liability insurance would probably provide coverage for court-ordered payments or a settlement.

Other Types of Coverage Used Tire Stores Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Product Liability Insurance

As a used tire business, you will be selling products that customers depend on to get around at high speeds. If a tire pops or a vehicle slips on an icy road, you could be found liable for any resulting damages to involved people and vehicles. Product liability insurance is designed to cover damages resulting from any products your company sells.

Commercial Property Insurance

This policy protects companies from serious losses in the event that their owned real estate, equipment, tools, or products are damaged or destroyed by factors like fire and extreme weather. Particularly since tires are flammable, this is a must-have policy for a used tire business that houses large quantities of their chief product. Commercial property insurance is also invaluable for providing coverage for related equipment and tools for tire changing and similar automotive fixes.

Business Interruption Insurance

If your business does suffer losses due to fires or various similarly destructive forces, this policy is a major plus in the effort to restore interrupted services. Business interruption insurance can help cover estimated losses in revenue during a temporary shutdown. If your used tire store is forced to go dormant for a little while, this policy can also cover rebuilding, relocation, and training costs for new workers learning to operate professional machinery. Protect your company during unexpected interruptions with business interruption insurance.

Commercial Auto Insurance

Tire shops may offer mobile automotive repairs or use commercial vehicles to pick up parts from a local vendor. If this is the case, a tire shop would be well advised to obtain commercial auto insurance. Any vehicle must be insured so long as it drives on public roads. With this policy, your commercial vehicles and any incurred medical expenses can be covered in the event of auto accidents.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your used tire store:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Used Tire Store Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes you do, even though this isn’t a legal requirement. This is because you will want to avoid a situation in which liability arises and you are not covered, as this can end up costing you thousands of dollars down the line.

All in all, we recommend purchasing at least a general liability insurance policy before you begin operating.

Not necessarily. Certain exceptions may be written directly into your used tire store insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.