Veterinary Practice Business Insurance

Getting business insurance for your veterinary practice is essential.

Owners of veterinary practices need to protect themselves against things like medical negligence claims, property damage, and employee-related disputes.

For example, a hired vet could perform a technique on a client’s pet and recklessly injure it, or an unruly pet could cause damage to an exam room.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Veterinary Practice

General liability insurance is — generally speaking — one of the most important insurance policies for veterinary practices.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Having said that, your veterinary practice may benefit from purchasing additional coverage; this is because a simple general liability policy is not always enough to fully protect it from all potential risks.

Additional coverage options for a veterinary practice include:

- Professional liability insurance (negligent acts and/or omissions)

- Workers’ compensation insurance (employee-related disputes)

- Commercial property insurance (damaged or stolen equipment)

You will also need to decide what type of business insurer you will use; as of 2026, there are two primary options available:

- Traditional brick-and-mortar insurers (e.g., The Hartford, CNA, Hiscox, etc.).

- Online insurers (e.g., Tivly, Ergo Next Insurance, etc.).

In most cases, we recommend going with an online insurer as a small business owner.

This is because online insurers have significantly lower operating costs, and can thus offer personalized coverage at a much lower rate in comparison to traditional brick-and-mortar alternatives.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

Cost of General Liability Insurance

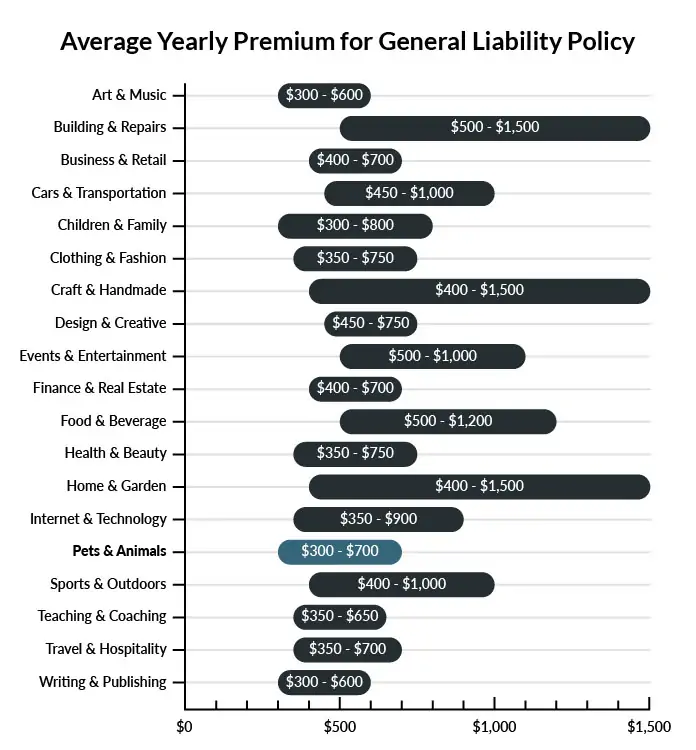

On average, veterinary practices in America spend between $300 – $700 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a veterinary practice to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our low-cost business insurance review.

Common Situations That General Liability Insurance May Cover for a Veterinary Practice

Example 1: During a rainstorm, a customer tracks mud into your veterinary facility. Your staff doesn’t notice it until another customer walks in and falls on the slippery surface. General liability insurance would cover the costs of the resulting injury.

Example 2: One of your customers believes your practice provided poor care to their pet even though you followed all guidelines and veterinary standards. The customer is spreading their version of the story and even attempts to go to the media. General liability insurance would cover the costs to fight their claims in court and in the public eye.

Example 3: When carrying in a new piece of equipment, one of your staff members damages a customer’s car in the parking lot. General liability insurance would pay for the costs of the damage.

Other Types of Coverage Veterinary Practices Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Commercial property insurance covers everything on your property, including surgical tools, flower beds, and the structural integrity of the building. If you own your office and facilities, this insurance covers it against damage from everything inclement weather, theft, and fires.

Professional Liability Insurance

Professional liability insurance is available to vets in case they make a mistake while on the job. If a customer tells you that their pet has an allergy and you treat them with a medication or other product that causes a reaction, they may sue for any resulting medical costs or other damages. This insurance also covers you for any harm done by an omission of information.

Workers’ Compensation Insurance

All vet owners need workers compensation insurance for their employees, whether they work full-time or part-time. Because animals can be unpredictable in a vet’s office, this insurance is particularly crucial for employees to get the coverage they need. It also covers chronic injuries, such as long-term shoulder pain after years of lifting heavy dogs.

Business Interruption Insurance

If your business has to close for a covered reason, this insurance will provide vets with a steady income until the practice can be reopened. For example, if the practice has a fire, you’ll still receive cash flow while the building undergoes renovations.

Commercial Auto Insurance

This insurance covers vets in case they need to transport pets from one location to the next. It’s also highly recommended if you need to move equipment in a vehicle, since standard policies will typically not cover damages to work-related items.

Commercial Umbrella Liability Insurance

This insurance extends the coverage of your general liability policy in the case of serious lawsuits that exceed the general liability limits. Most vets will get umbrella insurance due to the emotional nature of treating people’s beloved animals. If a customer chooses to draw out a lawsuit, it can cost far more than what a general liability policy will cover.

Data Breach Insurance

Hackers and virtual criminals of all kinds will target small businesses for any number of reasons. Because you keep so much personal and financial data about your customers on file, this insurance will cover the financial repercussions of a successful hack.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your veterinary practice:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Veterinary Practice Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes. This is because liability could theoretically arise as soon as you begin interacting with clients and their pets or hiring vets and other staff.

You will also want to purchase commercial property insurance in order to protect your medical equipment, office furniture, and other commercial property.

Not necessarily. Certain exceptions may be written directly into your veterinary practice insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.