Walking Tour Business Insurance

Getting insurance for your walking tour business is essential.

Walking tour businesses need to protect themselves against foreseeable claims that could cause them financial harm, such as bodily injury claims or misrepresentation.

For example, a patron could accidentally slip and fall down during a tour and injure themselves, or a tour group may claim that you did not provide the advertised and agreed-upon tour.

We’ll help you find the most personalized and affordable coverage for your unique business.

Recommended: Ergo Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Walking Tour Business

General liability insurance is — generally speaking — one of the most important insurance policies for walking tour businesses.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Having said that, your walking tour business might also benefit from purchasing additional types of policies. This is because a general liability policy will not protect you from all applicable risks:

- Errors and omissions insurance will protect your business’s assets from negligent acts and omissions committed by an employed tour guide (or yourself).

- Business income insurance will cover part of your lost income if you happen to need to close down temporarily.

- Workers’ compensation insurance covers your business’s assets from employee-related claims (e.g., disability benefits, injuries, etc.).

You will also need to decide how you will go about acquiring your coverage. As of 2026, there are two options available for small business owners:

- Traditional brick and mortar insurers (e.g., Nationwide, CNA, etc.).

- Online insurers (e.g., Ergo Next Insurance, Tivly, etc.).

We recommend going for an online insurer as a small business owner due to the fact that personalized coverage can be obtained at a much cheaper rate.

This is because online insurers benefit from lower operating costs (e.g., no insurance agent, etc.).

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

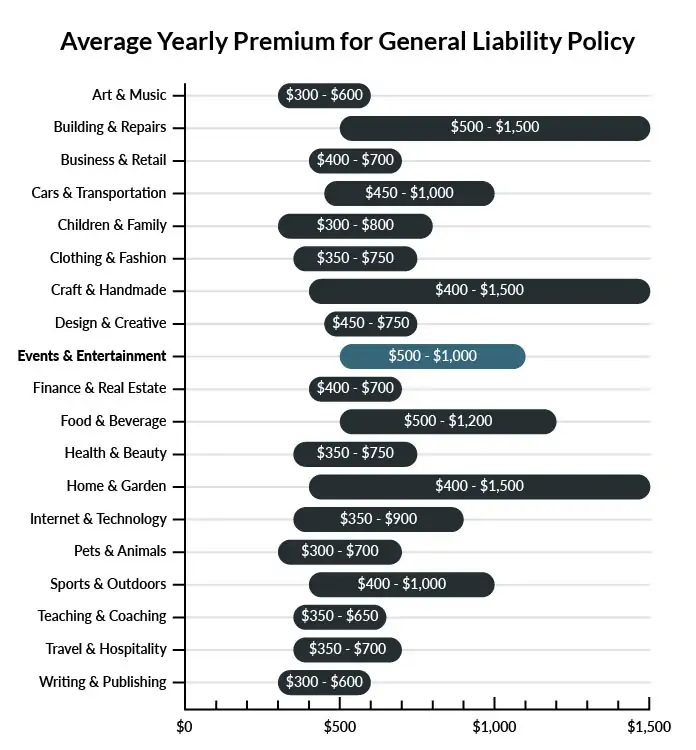

Cost of General Liability Insurance

On average, walking tour businesses in America spend between $500 – $1,100 per year for $1 million in general liability coverage.

Compare the average cost of general liability insurance for a walking tour business to other professional industries using the graph below.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may be able to acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than as a standalone policy.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our low-cost business insurance review.

Common Situations That General Liability Insurance May Cover for a Walking Tour Business

Example 1: During a tour, a pickpocket takes the wallet of one of the guests. They blame you for taking them to an unsafe area of town and failing to give a proper warning. They decide to sue for both monetary loss and emotional damages. General liability insurance would cover the costs to either fight or settle their claim.

Example 2: When you’re giving your presentation, you use your arms to illustrate your words. During one of your tours, you knock a person’s expensive sunglasses off their face and accidentally injure their eye. General liability insurance would cover the costs associated with replacing the sunglasses and treating their injuries.

Example 3: The name of your walking tour business is similar to that of another tourist-related company in the same area. The other company believes you are intentionally stealing business and decides to file a lawsuit for lost income. General liability insurance would protect your walking tour company by covering costs associated with fighting or settling the claim.

Other Types of Coverage Walking Tour Businesses Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Property Insurance

Some walking tour businesses will have a small office or structure where guests can check-in before they get started on the tour. If you own this space, you’ll need commercial property insurance to protect it in case of damage due to inclement weather, fire, or criminal activity.

Workers’ Compensation Insurance

Workers’ compensation insurance should be made available for all staff, whether they work once a week or every day of the month. Cities and towns can be dangerous places, and there are far more ways to be injured outdoors than in an air-conditioned office. This insurance will cover expenses associated with both acute and chronic injuries sustained on the job.

Data Breach Insurance

If your customers book primarily online, data breach insurance is available to cover the costs associated with a hack. If a cybercriminal steals your customers’ financial and biographic information, data breach insurance can help protect your livelihood and safeguard your reputation.

Commercial Umbrella Liability Insurance

Commercial liability insurance is available only if a general liability policy reaches its maximum payout for a claim against your company. For example, if a customer alleges that they sustained injuries due to your business, it may take several months to successfully fight the claim. General liability insurance may only cover a month of legal fees, but an umbrella policy gives the owner the means to continue without having to dip into their own personal funds.

Home-Based Insurance

If you operate your walking tour business from home, this insurance will keep your equipment and structure safe. A typical home insurance policy will not cover commercial supplies or tools.

Commercial Auto Insurance

This insurance is available if you transport guests to and from a specific base. Because you’re using the vehicle for commercial purposes, your personal auto insurance policy may deny certain claims associated with injuries or property damage. Commercial auto insurance will cover damage to your vehicle, it’s passengers, and contents in the event of an accident. It will also cover damage or injury to others involved in the accident if you or your employees are found liable.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your walking tour business:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Walking Tour Business Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Ergo Next Insurance. Ergo Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes you do. This is because you will want to protect yourself against foreseeable financial losses, and the “safest” way to go about doing this is to obtain your business insurance before you begin interacting with clients or hiring employees.

You will also want to protect your business’s assets from damage or theft (e.g., furniture, equipment, etc.).

Not necessarily. Certain exceptions may be written directly into your walking tour business insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability– that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.