Tree Service Insurance

Getting tree service insurance for your business is essential.

Tree services need to be protected against claims involving injuries and property damage disputes.

For example, an employee may get seriously injured while attempting to remove a tree during a job or could accidentally damage a client’s property.

We’ll help you find the most personalized and affordable business insurance for your tree service company.

Recommended: Next Insurance is dedicated to matching small businesses with the right policy at the best price.

Best Insurance for a Tree Service

General liability insurance is — generally speaking — one of the most important insurance policies for tree services.

Some of the risks general liability insurance covers are:

- Bodily injury

- Property damage

- Medical payments

- Legal defense and judgment

- Personal and advertising injury

Having said that, you should note that not all tree service businesses will be “fully” protected with a simple general liability policy.

Your tree service business will most likely benefit from these other types of policies:

- Umbrella insurance coverage will pick up where your other insurance policy limits leave off. Due to the high-risk nature of the tree service industry, umbrella insurance is highly recommended.

- Errors and omissions will protect your business’s assets from negligent acts or omissions committed by you or an employee.

- Commercial property will cover your business’s equipment in the event that it gets damaged or stolen.

- Commercial auto coverage may be legally required if you lease or purchase a company vehicle in order to transport your equipment and/or employees.

Let’s Find the Coverage You Need

The best insurers design exactly the coverage you need at the most affordable price.

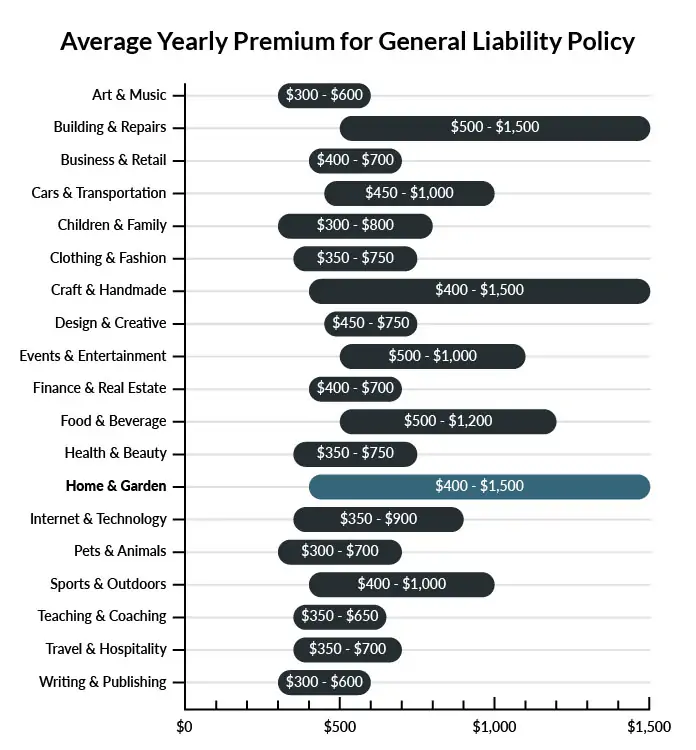

Tree Service Insurance Cost

The average tree service in America spends between $400-$1,500 per year for $1 million in general liability coverage.

Check out the chart below for a snapshot of average general liability insurance expenditure across a variety of industries.

Several factors will determine the price of your policy. These include your:

- Location

- Deductible

- Number of employees

- Per-occurrence limit

- General aggregate limit

You may acquire general liability insurance at a discounted rate by purchasing it as part of a business owner’s policy (BOP) rather than a standalone one.

A BOP is a more comprehensive solution that includes multiple forms of coverage, such as business interruption and property insurance.

Find the Best Rate

Discover the best coverage at the lowest rate in our low-cost business insurance review.

Common Situations That General Liability Insurance May Cover for a Tree Service

Example 1: A tree accidentally falls into the property owner’s window while your team is trying to remove it. Their glass is not only broken but the window frame is also damaged from the branches. General liability insurance would most likely cover the cost of fixing the window and any surrounding damage.

Example 2: You take down a tree for a customer and remove the stump. After filling the hole, the customer claims that you damaged the roots of their other tree, causing them to die. General liability insurance would most likely take care of the ensuing costs.

Other Types of Coverage Tree Services Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some of the most common types of coverage:

Commercial Auto Insurance

Tree services rely on their vehicles to haul equipment and get from one property to the next. A personal auto insurance policy will not cover potential damages to the vehicle — even if the driver is technically off-duty at the time of the crash.

Commercial auto insurance covers both the vehicle and any other property damage in the event of an accident.

Commercial Property Insurance

If your tree service owns its own office or warehouse space, then you’ll need commercial property insurance to cover both the physical structure and the property inside of it.

If your business keeps expensive equipment inside the property or sells specialized tools to its customers, then commercial property insurance will most likely pay to repair the building and replace the tools in the event of certain covered events like a fire or severe storm.

Professional Liability Insurance

Professional liability insurance is there for business owners in case their work causes any type of damage to the physical structure or surrounding grounds. This coverage extends to errors or omissions made by your employees. So if someone accidentally cuts down the wrong tree, you will most likely be covered.

Commercial Umbrella Insurance

Whether it’s a lawsuit from a competing tree service company or a medical claim brought on by pesticide use, commercial umbrella insurance can cover a wide array of potential costs should they exceed the limits of your primary general liability insurance policy.

Product Liability Insurance

If your business sells products to its customers, such as pruners or hedge clippers, then you’ll need product liability insurance. Even if your business didn’t actually make the products, you could be held liable for any damage they caused simply because you sold them.

Additional Steps To Protect Your Business

Although it’s easy (and essential) to invest in business insurance, it shouldn’t be your only defense.

Here are several things you can do to better protect your tree service:

- Use legally robust contracts and other business documents. (We offer free templates for some of the most common legal forms.)

- Set up an LLC or corporation to protect your personal assets. (Visit our step-by-step guides to learn how to form an LLC or corporation in your state.)

- Stay up to date with business licensing.

- Maintain your corporate veil.

Tree Service Insurance FAQ

Yes, absolutely. You will need to first get a quote from an online business insurance provider like Next Insurance. Next allows you to then purchase a policy immediately and your coverage will be active within 48 hours.

A typical business owner’s policy includes general liability, business interruption, and commercial property insurance. However, BOPs are often customizable, so your agent may recommend adding professional liability, commercial auto, or other types of coverage to your package depending on your company’s needs.

“Business insurance” is a generic term used to describe many different types of coverage a business may need. General liability insurance, on the other hand, is a specific type of coverage that business owners need to protect their assets.

Yes. Getting business insurance can be done for a relatively low cost, and it can end up saving you tens of thousands of dollars down the line.

Since you cannot accurately predict when you will need to rely on business coverage, we recommend purchasing it before you begin interacting with your clients.

Not necessarily. Certain exceptions may be written directly into your tree service insurance policy, and some perils may be entirely uninsurable.

Yes, an LLC is meant to create a legal barrier between your business and your personal assets and credit. If you haven’t formed an LLC yet, use our Form an LLC guide to get started.

An LLC doesn’t protect your business assets from lawsuits and liability – that’s where business insurance comes in. Business insurance helps protect your business from liability and risk.