Do I Need an LLC for My Financial Planning Firm?

Starting a limited liability company (LLC) for your financial planning firm can provide several benefits.

Most importantly, an LLC structure offers limited liability to its owners, which can protect their personal assets from lawsuits and creditors.

For a financial planning firm, lawsuits can arise from things like professional malpractice and negligence claims (e.g., recommending a risky investment strategy that ends up causing a client significant financial harm, etc.).

LLCs are also affordable, highly flexible (from a tax point-of-view), and can make your financial planning firm seem more credible.

Find the Right Business Structure For You

Figure out which business structure works best for you — in just a few easy questions.

Answer a few short questions about your business and we’ll recommend the right structure for you — plus show you how to get started.

Should I Start an LLC for a Financial Planning Firm?

LLCs are a simple and inexpensive way to protect your personal assets and save money on taxes.

You should start an LLC when there’s any risk involved in your business and/or when your business could benefit from tax options and increased credibility.

LLC Benefits for a Financial Planning Firm

By starting an LLC for your financial planning firm, you can:

- Protect your savings, car, and house with limited liability protection

- Have more tax benefits and options

- Increase your business’s credibility

Limited Liability Protection

LLCs provide limited liability protection. This means your personal assets (e.g., car, house, bank account) are protected in the event your business is sued or if it defaults on a debt.

Financial planning firms will benefit from liability protection because of the risk of professional liability claims, financial data breaches, workplace accidents, and more.

Example 1: You manage a team of financial advisors at your firm. One day, an advisor recommends an investment strategy that turns out to be risky and costly for your clients. As a result, they decide to sue the company for the losses they incurred. Limited liability protection will prevent you from losing any of your personal assets due to this lawsuit.

Example 2: You own a financial planning firm that provides services to small businesses. One of your clients experiences an unexpected data breach, resulting in significant financial losses and reputational damage. They decide to sue the company for failing to adequately protect their sensitive information. Limited liability protection will shield your personal assets from the resulting lawsuit.

Example 3: You decide to invest in a new technology platform for your financial planning firm, but the project fails and incurs significant losses. As a result, you are declared bankrupt and may need to liquidate some of your business assets. Limited liability protection will ensure that any debts or liabilities incurred by your business do not impact your personal finances.

Example 4: A client sues your firm, claiming that one of your financial advisers steered them toward much riskier investments than they said they were comfortable with.

An LLC will also protect your personal assets in the event of commercial bankruptcy or loan default.

To maintain your LLC’s limited liability protection, you must maintain your LLC’s corporate veil.

LLC Tax Benefits and Options for a Financial Planning Firm

LLCs, by default, are taxed as a pass-through entity, just like a sole proprietorship or partnership. This means that the business’s net income passes through to the owner’s individual tax return.

The business’s net income is then subject to income taxes (based on the owner’s tax bracket) and self-employment taxes.

Sole proprietorships and partnerships are taxed in a similar way to LLCs, but they do not offer limited liability protection or other tax options.

S Corp Option for LLCs

An S corporation (S corp) is an IRS tax status that an LLC can elect. S corp status allows business owners to be treated as employees of the business (for tax purposes).

S corp tax status can reduce self-employment taxes and will allow business owners to contribute pre-tax dollars to 401k or health insurance premiums.

The S corp status requires that the business pay the employee-owner(s) a reasonable salary for the work they perform.

In addition, the business might need to spend more on accounting, bookkeeping, and payroll services. To offset these costs, you’d need to be saving about $2,000 a year on taxes.

We estimate that if a financial planning firm owner can pay themselves a reasonable salary and at least $10,000 in distributions each year, they could benefit from S corp status.

You can start an S corp when you form your LLC. Our How to Start an S Corp guide will lead you through the process.

Credibility and Consumer Trust

Financial planning firms rely on consumer trust. Credibility plays a key role in creating and maintaining any business.

Businesses gain consumer trust simply by forming an LLC.

A growing business can also benefit from the credibility of an LLC when applying for small business loans, grants, and credit.

Launch Your LLC With ZenBusiness

Form your LLC with ZenBusiness and get $100 off their most premium package with our coupon code: REALLY100. This includes a free EIN, registered agent service, and dedicated compliance handling.

How to Form an LLC

Forming an LLC is easy. There are two options for forming your LLC:

- You can hire a dependable LLC formation service to set up your LLC for a small fee

- Or, you can choose your state from the list below to start an LLC yourself

Select Your State

- Alabama LLC

- Alaska LLC

- Arizona LLC

- Arkansas LLC

- California LLC

- Colorado LLC

- Connecticut LLC

- Delaware LLC

- Florida LLC

- Georgia LLC

- Hawaii LLC

- Idaho LLC

- Illinois LLC

- Indiana LLC

- Iowa LLC

- Kansas LLC

- Kentucky LLC

- Louisiana LLC

- Maine LLC

- Maryland LLC

- Massachusetts LLC

- Michigan LLC

- Minnesota LLC

- Mississippi LLC

- Missouri LLC

- Montana LLC

- Nebraska LLC

- Nevada LLC

- New Hampshire LLC

- New Jersey LLC

- New Mexico LLC

- New York LLC

- North Carolina LLC

- North Dakota LLC

- Ohio LLC

- Oklahoma LLC

- Oregon LLC

- Pennsylvania LLC

- Rhode Island LLC

- South Carolina LLC

- South Dakota LLC

- Tennessee LLC

- Texas LLC

- Utah LLC

- Vermont LLC

- Virginia LLC

- Washington LLC

- Washington D.C. LLC

- West Virginia LLC

- Wisconsin LLC

- Wyoming LLC

For most new business owners, the best state to form an LLC in is the state where you live and where you plan to conduct your business.

Do LLCs Need Insurance?

All businesses need insurance to protect their business assets — even LLCs. This is because the limited liability protection from an LLC protects your personal assets, not your business assets.

Financial planning firms need insurance to protect against the potential for losses caused by errors and omissions that could occur when providing financial advice. Business insurance can provide crucial coverage for a financial planning firm by protecting it from claims related to negligence or malpractice and other forms of legal liability stemming from their professional services.

Common Situations Business Insurance May Cover for a Financial Planning Firm

Example 1: A new client is visiting your office to discuss financial planning options. One of your employees rounds the corner while talking to someone else and runs directly into the client, knocking her back into a desk. She breaks her wrist, requiring medical care. She files a lawsuit against your company. Your general liability insurance will pay for your legal defense costs.

Example 2: One of your long-term clients leaves for the restroom, slips on a puddle, and breaks his tailbone. He is upset about the accident but decides not to file a lawsuit. However, he does ask your business to cover his medical bills. Your general liability insurance policy will likely cover his medical treatment.

Example 3: You get an email from the attorney of one of your competitors informing you that the competitor is suing your business for libel. You are not certain how your business may have libeled the competitor, but you understand that you need to get an attorney as soon as possible to ensure that your business is protected. The general liability insurance policy you carry covers your legal fees in this situation, paying for your attorney and for any payout or settlement that may be required.

Other Types of Coverage Financial Planning Firms Need

While general liability is the most important type of insurance to have, there are several other forms of coverage you should be aware of. Below are some other types of insurance all financial planning firms should obtain:

Workers’ Compensation Insurance

The state you do business in most likely requires that you carry workers’ compensation insurance if you have employees. The policy will benefit your business in several ways, including paying for medical treatment for work-related injuries your employees sustain. It will also help to cover the lost wages of injured employees while they recover.

Professional Liability Insurance

Professional liability insurance is designed specifically for your business. It helps protect you from liability caused by errors or failure to perform. There is always the possibility that one of your clients will file a lawsuit against you, claiming you failed in your financial planning duties. With professional liability insurance, your policy will pay for your legal fees if you are sued and for any settlement that may be required.

Commercial Property Insurance

The computers, office furniture, and other equipment you have in your office were costly to purchase—and they would be costly to replace if they were damaged or destroyed. Commercial property insurance is designed to help pay for damage to property owned by your business that is caused by an event like a fire or severe storm, so you can get replacements without paying out of pocket.

Data Breach Insurance

Also called cyber attack insurance, data breach insurance provides protection for your business if you are the victim of a cyber attack. For example, if your clients’ financial data is compromised by a hacker and one or more clients file a lawsuit against your business, your data breach insurance would pay for your legal fees. Your data breach insurance would also pay for any payouts or settlements that might be required to protect your business and end the lawsuit.

Should I Start an LLC FAQ

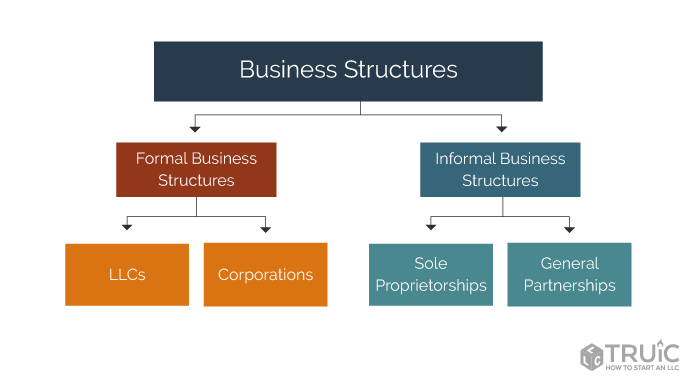

Choosing the right business structure depends on your business’s unique circumstances and needs. However, unless your business is very low risk (like a hobby), an LLC is likely the better option.

Visit our LLC vs. Sole Proprietorship guide to learn more.

At a minimum, you’ll need general liability insurance, workers’ compensation insurance, and professional liability insurance.

Read our Business Insurance article for more info.

Starting a financial planning firm requires registering as an investment advisor with the state and incurring startup costs of between $10,000 and $20,000. These include office rent, legal documents (such as Form ADV client brochure and fee disclosure), fees for vendors, and a good contract with a custodian.

Visit our How to Start a Financial Planning Firm guide to learn more about the costs of starting and maintaining this business.

You will likely need to rent and maintain an office for your financial planning firm. In addition, you will need to purchase various kinds of business insurance as well as hire staff.

Learn more about running a financial planning firm.

Financial advisory firms make money by charging clients for financial advice and planning. In addition, many of them charge fees for managing investments.

Learn more about starting a financial planning firm.

A financial planning firm, otherwise known as a financial advising business, helps people plan and meet their financial goals. Financial planners analyze clients’ budgets, insurance, investments, and other assets.

A financial planning firm’s profit margin can average about 22%.

Learn more about starting a financial planning firm.